BIS Annual Economic Report |

Introduction

The global economy has reached a critical and perilous juncture. Policymakers are facing a unique constellation of challenges. Each of them, taken in isolation, is not new; but their combination on a global scale is. On the one hand, central banks have been tightening to bring inflation back under control: prices are rising far too fast. On the other hand, financial vulnerabilities are widespread: debt levels – private and public – are historically high; asset prices, especially those of real estate, are elevated; and risk-taking in financial markets was rife during the phase in which interest rates stayed historically low for unusually long. Indeed, financial stress has already emerged. Each of the two challenges, by itself, would be difficult to tackle; their combination is daunting.

This year’s Annual Economic Report explores the global economy’s journey and the policy challenges involved. It is, in fact, an exploration of not one but three interwoven journeys: the journey that has taken the global economy to the current juncture; the journey that may lie ahead; and, in the background, the journey that the financial system could make as digitalisation opens up new vistas. Much is at stake. Policymakers will need to work in concert, drawing the right lessons from the past to chart a new path for the future. Along the way, the perennial but elusive search for consistency between fiscal and monetary policy will again take centre stage. Prudential policy will continue to play an essential supporting role. And structural policies will be critical.

What follows considers, in turn, each of the three journeys.

The macroeconomic journey: looking back

How did the global economy fare in the year under review? Even more importantly, what forces shaped its journey?

The year under review

High inflation, surprising resilience in economic activity and the first signs of serious stress in the financial system – this is, in a nutshell, what the year under review had in store.

Inflation continued to hover well above central bank targets across much of the world. Fortunately, there were clear indications that headline inflation was peaking or had started to decline. But core inflation proved more stubborn. The reversal of commodity prices and a marked slowdown in manufacturing prices provided welcome relief even as stickier services prices gathered steam. Several forces were playing out, including easing global supply chain bottlenecks, the post-pandemic rotation of global demand back from manufacturing to services, and the effects of repeated generous fiscal support packages. Labour markets remained very tight, with unemployment rates generally at historical lows.

Global growth did slow, but proved remarkably resilient. The widely feared recession in Europe did not materialise, thanks partly to a mild winter, and China rebounded strongly once Covid restrictions were suddenly lifted. Consumption held up surprisingly well globally, as households continued to draw on savings accumulated during the pandemic and employment remained buoyant. As the year progressed, professional forecasters revised their growth projections upwards, although they still saw slower global growth in the year ahead.

Even as growth held up, signs of serious strains emerged in the financial system. Some milder ones appeared among non-bank financial intermediaries (NBFIs). In October, following the announcement of fiscal measures that undermined policy credibility, the UK government bond market saw a sharp increase in yields and a sudden evaporation of liquidity: leveraged investment vehicles through which pension funds were matching the duration of their liabilities were forced to sell to meet margin calls. Other signs of strain, perhaps more serious and surprising, appeared in the banking sector. A number of regional banks in the United States failed as a result of a combination of losses accumulated on long-maturity, mostly government, securities and lightning runs. And in an environment of fragile confidence, Credit Suisse – a global systemically important bank – went under, as it abruptly lost market access following long-standing concerns about its business model and risk management.

Once again, the strains prompted large-scale official intervention on both sides of the Atlantic to prevent contagion – worryingly, an increasingly familiar picture. Central banks activated or extended liquidity facilities or asset purchases. Where necessary, governments supplied solvency backing, implicitly or explicitly, in the form of guarantees and ultimate support for enlarged deposit insurance schemes. The response restored market calm.

In the meantime, the highly synchronous and forceful monetary policy tightening continued. Central banks across the globe hiked policy rates further. What’s more, those that had engaged in large-scale asset purchases began to unwind them: albeit gradually, quantitative easing turned into quantitative tightening. At the same time, policy rates often remained below inflation rates, ie negative in real terms.

In response to the tightening and the economic outlook, financial conditions reacted unevenly. In general, banks tightened credit standards. But financial markets were less responsive. To be sure, on balance, conditions there did tighten compared with those prevailing at the time of the first hike. But in the second half of the year, they loosened somewhat, as bond yields declined and risky asset prices rose. Central banks contended with a disconnect between their communication, which pointed to a more persistent tightening, and financial market participants’ views, which saw an easier stance ahead.

The longer-term backdrop

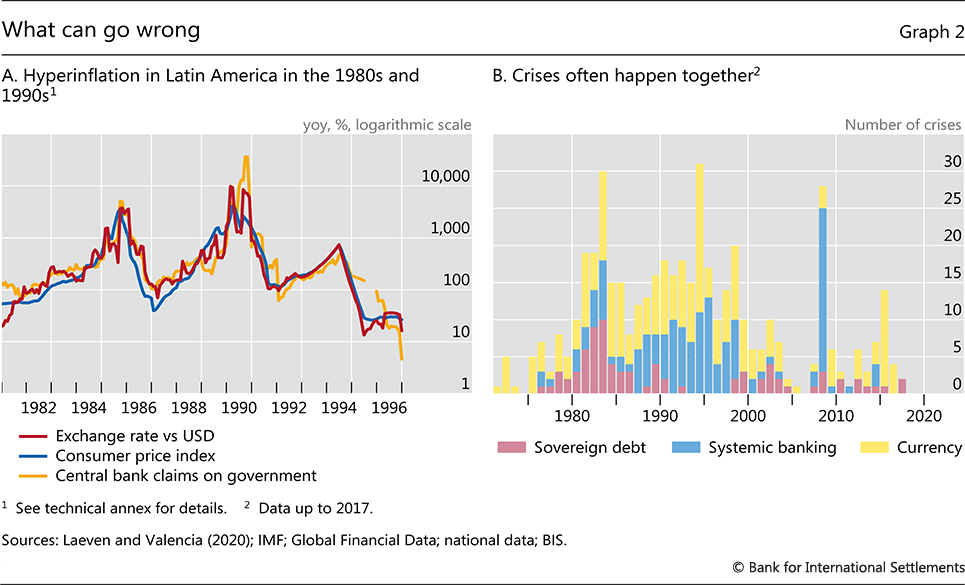

The rather unique combination of high inflation and widespread financial vulnerabilities is not simply a bolt from the blue. To be sure, the pandemic and, to a lesser extent, the war in Ukraine have played an important role in the recent inflation flare-up. But the root causes of the current problems run much deeper. After all, debt and financial fragilities do not appear overnight; they grow slowly over time.

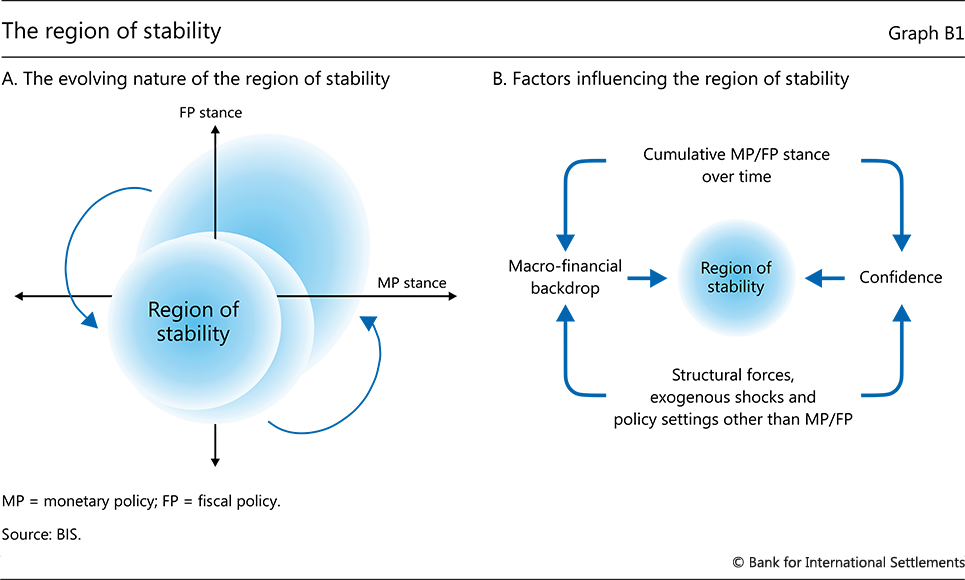

As explored in detail in Chapter II, the combination of high inflation and financial vulnerabilities is probably best seen as reflecting the confluence of two interdependent factors. First, the changing shape of the business cycle. Second, monetary and fiscal policies testing, once again, the boundaries of what might be termed the “region of stability” – the region that maps the constellations of the two policies that foster sustainable macroeconomic and financial stability, keeping the inevitable tensions between the policies manageable. The changing shape of the business cycle determines what kind of symptom signals that the boundaries are being tested – inflation, financial instability or both. The conduct of policy, interacting with structural forces, determines the shape of the business cycle itself.

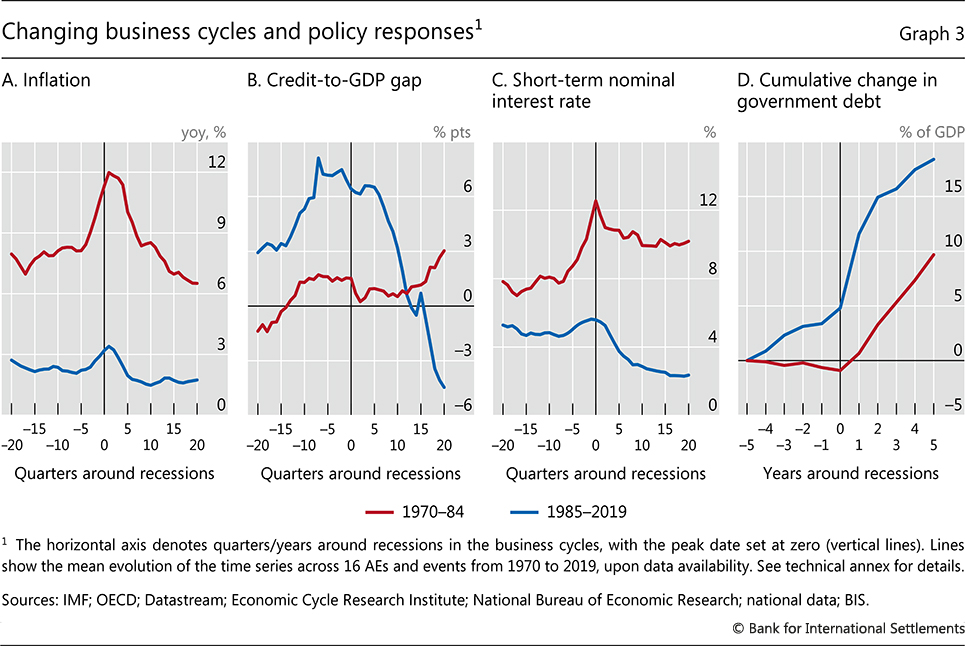

The mid-1980s represented a watershed in the evolution of the business cycle, at least in advanced economies. Until then, recessions tended to follow a tightening of monetary policy designed to bring inflation under control, while financial stress was absent or largely contained. Thereafter, all the way to the sui generis Covid crisis, recessions were ushered in by financial booms that turned into busts, sometimes triggering widespread financial instability, while inflation remained generally low and stable. Emerging market economies, in turn, were buffeted by the global waves unleashed in advanced economies, most notably in the form of capital flows. Accordingly, regional and country differences aside, exchange rate tensions typically played a bigger role there than in advanced economies.

Two fundamental structural changes contributed to the shift from inflation-induced to financial cycle-induced recessions. Broad-ranging financial liberalisation, both domestically and internationally, provided scope for much larger financial expansions and contractions, no longer suppressed by the tight web of regulations that had greatly constrained the financial system. And the globalisation of the real economy helped central banks hardwire low inflation, by eroding the pricing power of labour and firms. In the process, inflation stopped acting as a reliable barometer of the sustainability of economic expansions: the build-up of financial imbalances took over that role.

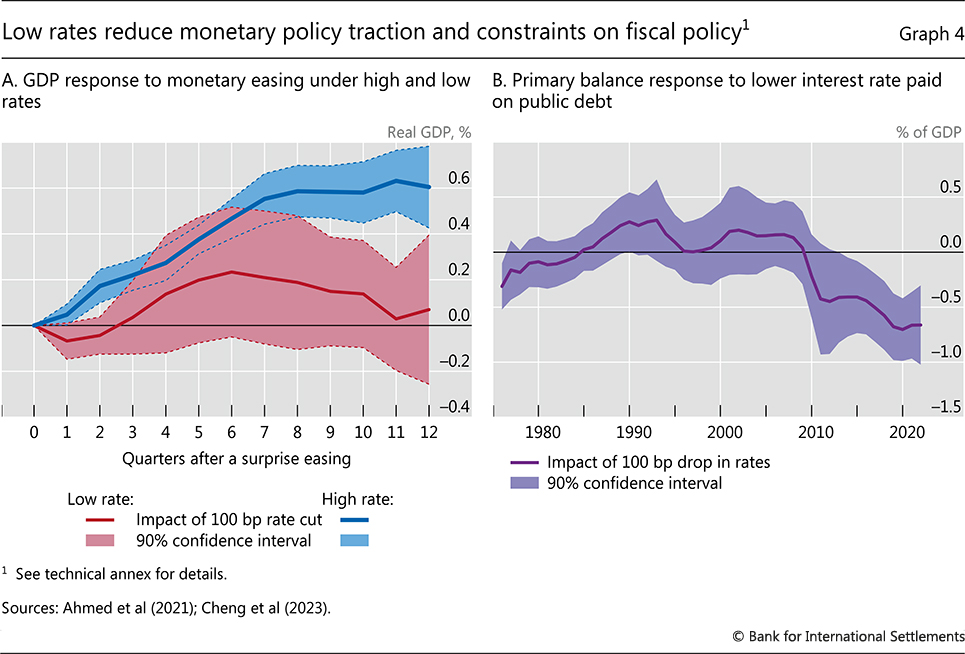

Hence an acute policy dilemma. A painful lesson policymakers had drawn from the high-inflation era was that policies which turned out to be overambitious could generate price instability. In the low-inflation era, however, the constraints on economic expansions had seemingly disappeared. The boundaries of the region of stability had become fuzzier, hardly visible in fact. And the fragility of the financial system, not buttressed by a sufficiently incisive effort to strengthen prudential regulation, clouded the picture further. The economy appeared stable until, suddenly, it no longer was. The post-Great Financial Crisis (GFC) experience blurred the boundaries of the region even further. Inflation hovered stubbornly below inflation targets: having helped central banks’ efforts, globalisation was now hindering them. And fiscal policy was asked to step up to the plate to ensure that central banks would no longer be the “only game in town”, which it did.

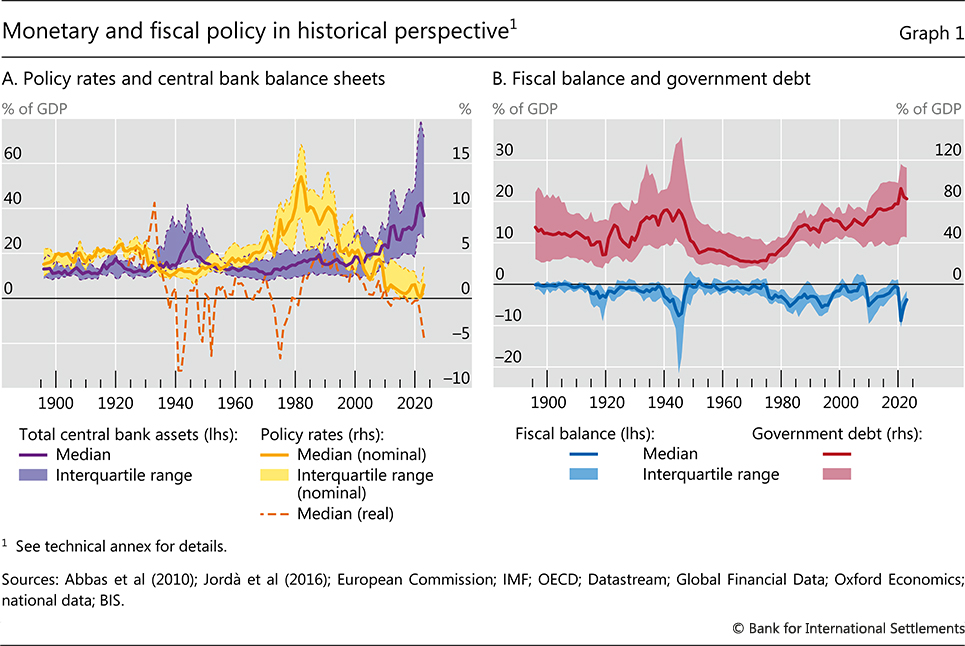

By the time the Covid crisis struck, monetary and fiscal policy were testing the boundaries of the region of stability once again. Interest rates had never been so low and in some cases were now negative even in nominal terms. Central bank balance sheets had never been so large except during wars. Government debt in relation to GDP, joining private sector debt, was flirting with previous historical peaks reached around World War II. And yet, because of the exceptionally low interest rates, the debt burden had never felt so light. Low rates as far as the eye could see encouraged further debt expansion, public and private. The forceful and concerted monetary and fiscal response to the Covid crisis took policies one step further towards the boundary.

The remarkable post-pandemic surge in global demand against the backdrop of the supply disruptions did the rest. Against all expectations, inflation had come back with a vengeance. Monetary policy had to tighten, straining public finances and private sector balance sheets. The financial system came under stress. While understandable as the Covid crisis broke out, with the benefit of hindsight, it is now clear that the fiscal and monetary policy support was too large, too broad-based and too long-lasting.

The macroeconomic journey: looking ahead

Given where we are, what does the journey ahead look like? In the near term, it is indeed possible that the global economy will smoothly overcome the obstacles it is facing. This seems to be what financial market participants and professional forecasters are anticipating. Moreover, peering further into the future, the journey could continue without major incidents. That said, both near- and long-term hazards are lurking along the way. And policies will be the deciding factor.

Near- and longer-term hazards

In the near term, two challenges stand out: restoring price stability and managing any financial risks that may materialise.

Inflation could well turn out to be more stubborn than currently anticipated. True, it has been declining, and most forecasters see it moving within target ranges over the next couple of years. Moreover, inflation expectations, albeit hard to measure reliably, have not rung alarm bells. Even so, the last mile could prove harder to travel. The surprising inflation surge has substantially eroded the purchasing power of wages. It would be unreasonable to expect that wage earners would not try to catch up, not least since labour markets remain very tight. In a number of countries, wage demands have been rising, indexation clauses have been gaining ground and signs of more forceful bargaining, including strikes, have emerged. If wages do catch up, the key question will be whether firms absorb the higher costs or pass them on. With firms having rediscovered pricing power, this second possibility should not be underestimated. Our illustrative simulations indicate that, in this scenario, inflation could remain uncomfortably high. As last year’s Annual Economic Report documented, transitions from low- to high-inflation regimes tend to be self-reinforcing. And once an inflation psychology sets in, it is hard to dislodge.

At a macroeconomic level, historically high private indebtedness and elevated asset valuations cloud the outlook. They can greatly heighten the sensitivity of private expenditures to higher interest rates, although the lengthening of maturities during the period of low inflation has muted, or at least delayed, the pass-through to debt service burdens, and the savings cushions built during the pandemic have softened the blow. Stylised simulations suggest that the impact could be substantial. In a higher-for-longer scenario, with policy rates reaching a peak 200 basis points above the market-implied one and staying there through 2027, debt service burdens would rise substantially, asset prices would drop markedly and output in a representative sample of economies could be some 2% lower at the end of a simulation horizon. Moreover, one should not rule out outsize responses should debt service burdens reach critical thresholds.

Higher interest rates, a turn in the financial cycle and an economic slowdown would eventually raise credit losses. These, in turn, could generate further strains in the financial system. It is quite common for banking stress to emerge following a monetary policy tightening – in as many as a fifth of cases within three years after the first hike. The incidence rises considerably when initial debt levels are high, real estate prices are elevated or the increase in inflation is stronger. The current episode ticks all the boxes. The stress we have seen so far has reflected exclusively interest rate risk, revealing the fragility of strategies predicated on the view that interest rates would remain low far into the future. The credit leg is still to come. The lag between the two legs can be quite long.

Once the credit leg materialises, the resilience of the financial system will be tested again. Simple simulations indicate that, in the market-implied interest rate scenario, in a representative sample of advanced economies credit losses would be in line with historical averages. But they would be of a similar order of magnitude as during the GFC in the higher-for-longer scenario.

The impact of those losses will depend, critically, on the loss-absorbing capacity of the banking system. Since the GFC, thanks in no small measure to the financial reforms, banks have bolstered their capital. That said, pockets of vulnerability remain. Recent events have shown how the failure of even comparatively small institutions can shake confidence in the overall system. Moreover, the price-to-book ratios of many banks, including large ones, have been languishing far below one. This reflects market scepticism about the underlying valuations and long-term profitability of those institutions. Admittedly, this is not new. But, in an environment of more fragile confidence, it could turn out to be a significant vulnerability.

Before stress emerged among banks, all the attention was focused on the NBFI sector. And with reason. The sector has grown in leaps and bounds since the GFC, and now accounts for over half of all financial assets globally. While, on balance, less leveraged than its banking counterpart, the sector is rife with hidden leverage and liquidity mismatches, especially in the asset management industry. It has been a source of large losses for banks, such as in the Archegos case – which, incidentally, hit Credit Suisse especially hard. And it was at the heart of the March 2020 turmoil, which prompted large-scale central bank interventions. The latest tremors in the UK gilt market are a reminder that attention is still justified.

While it is hard to tell where strains might emerge next, several vulnerabilities stand out. In the corporate sector, private credit markets remain very opaque against the backdrop of a long-term deterioration in credit ratings. In the leveraged loan market, securitised products have grown rapidly. Exposures to commercial real estate are bound to see losses, as the sector is buffeted by powerful cyclical and structural headwinds – losses that could also be a source of stress for banks, as they have been throughout history. In addition, structural weaknesses linger in some government bond markets.

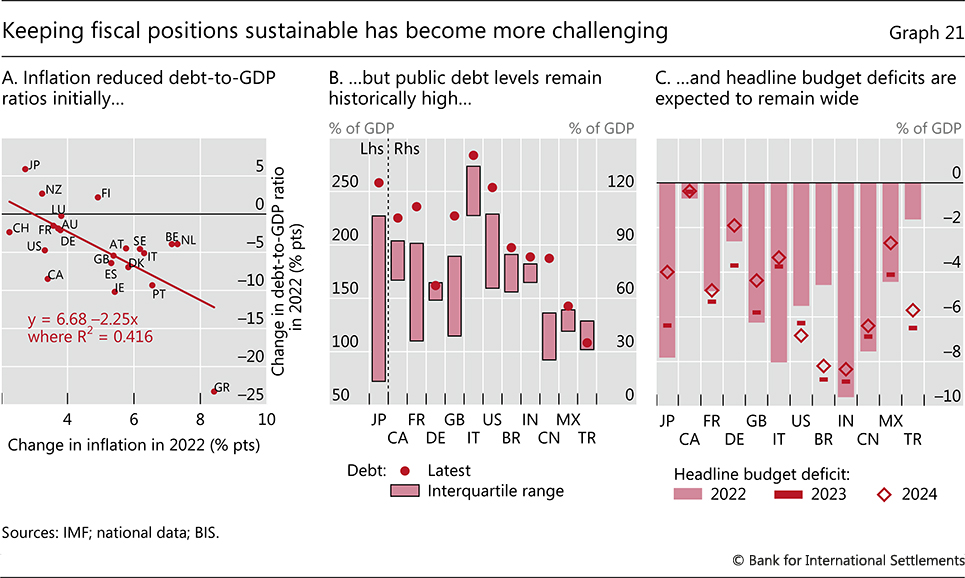

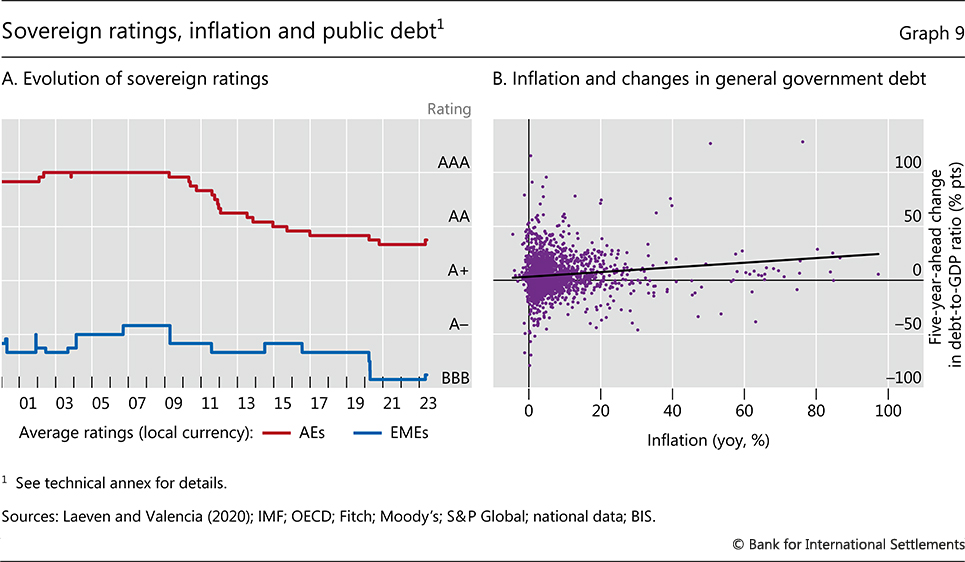

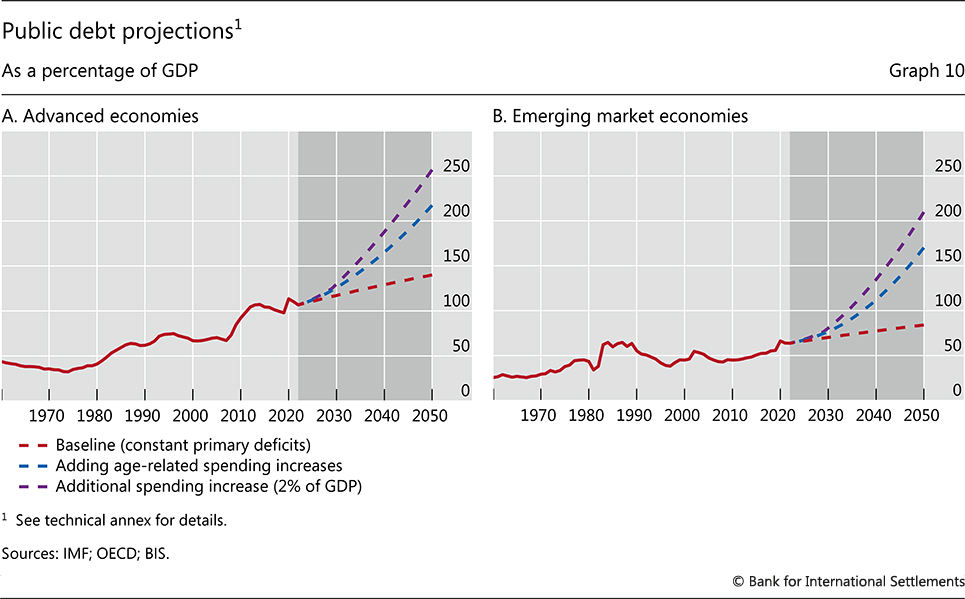

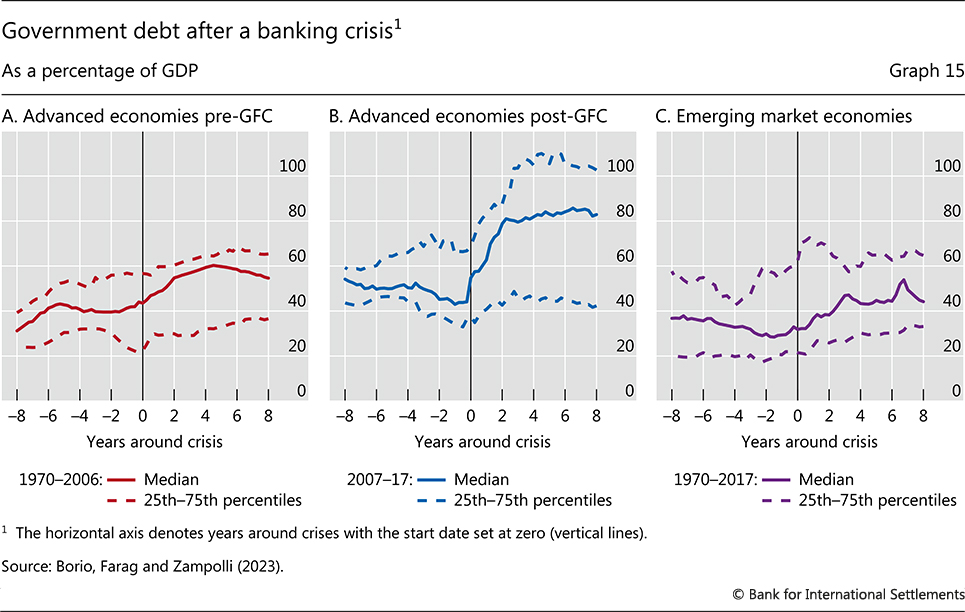

Looking further out, a key source of concern is the sustainability of public debt – an issue analysed in depth in Chapter II. A vulnerable sovereign means a vulnerable financial system. This is because the sovereign can generate financial instability or fail to act as an effective backstop of the financial sector. Central banks can provide liquidity, but only the sovereign can back up solvency. Moreover, the sovereign’s creditworthiness depends on the health of the financial sector. Indeed, banking crises have typically caused surges in public debt, in teens of GDP – directly, because of the government support, and indirectly, because of the damage to economic activity. Long-term projections of public debt trajectories are worrisome, even under favourable interest rate and growth configurations (see below).

Near- and longer-term policy challenges

The sheer size of the challenges ahead calls for a holistic policy response, involving monetary, fiscal, prudential and, last but not least, structural policies. Consider, in turn, the near-term and longer-term challenges, although the dividing line between the two is quite fuzzy.

The near term

The priority for monetary policy is to bring inflation back to target. The insidious damage that a high-inflation regime does to the economic and social fabric is well known. The longer inflation is allowed to persist, the greater the likelihood that it becomes entrenched and the bigger the costs of quenching it.

In bringing inflation back to target, central banks face at least three challenges. First, historical statistical relationships provide limited guidance when a transition to a high-inflation regime threatens. Both judgment and more formal models are tested hard. Second, the transmission mechanism of monetary policy is clouded by the exceptional post-pandemic conditions, which add to the well known lags. Hence the pause many central banks have taken to better assess the impact of the tightening so far. Finally, further financial system stress could well emerge. In that case, if the stress is acute enough, addressing it without compromising the fight against inflation will require the active support of other policies, not least prudential and fiscal, to complement central banks’ deployment of the range of tools at their disposal. This would contain the damage while allowing monetary policy to keep a restrictive stance for as long as necessary.

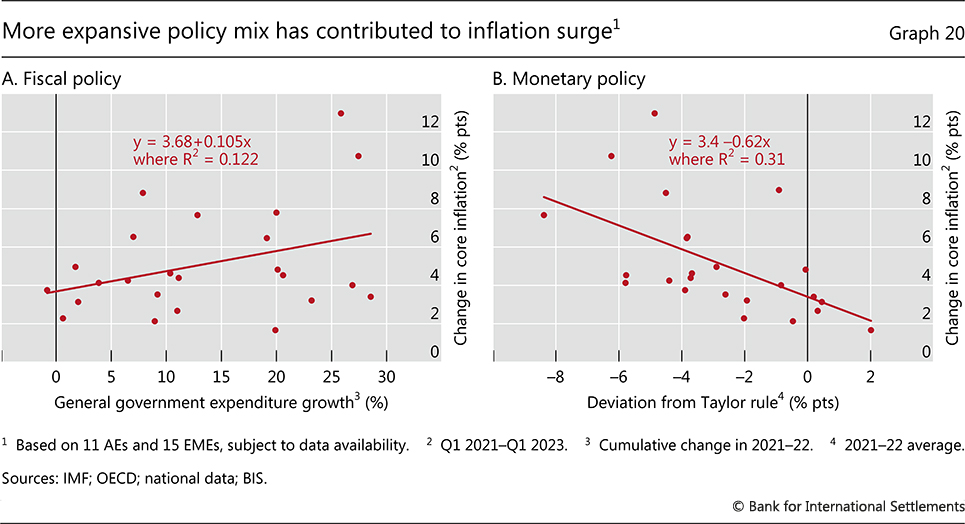

The priority for fiscal policy is to consolidate. To be sure, deficits have narrowed somewhat, especially in cyclically adjusted terms. But some of the improvement reflects the temporary impact of the inflation burst, and cyclical adjustments have proved quite misleading in the past, especially before slowdowns. Moreover, from a long-term perspective, deficits remain too high. Consolidation would provide critical support in the inflation fight. It would also reduce the need for monetary policy to keep interest rates higher for longer, thereby reducing the risk of financial instability.

By bolstering the financial system’s resilience, prudential policy can also support the inflation fight, as it would increase monetary policy headroom. Macroprudential measures need to be kept tight for as long as possible, or even tightened further where appropriate. Similarly, (microprudential) supervision needs to be stiffened to remedy some of the deficiencies that came to light in recent bank failures. While changes in regulatory standards take longer, a reflection on the recent experience should start without delay; and indeed it has. Examples of issues to be examined are the treatment of interest rate risk, the appropriateness of historical cost accounting, not least for assets used for liquidity management purposes (eg government securities) and assumptions about the stickiness of various deposit categories. But beyond banking, we should not lose sight of the urgent need to strengthen the regulation of NBFIs from a systemic perspective.

The longer term

In the longer term, the challenge is to put in place policies and frameworks that foster a stable financial and macroeconomic environment while strengthening the potential for robust and sustainable growth. As argued in detail in Chapter II, a key element of this multi-pronged strategy is to ensure that monetary and fiscal policies operate firmly within the region of stability. This means not being a source of instability and keeping sufficient safety margins or buffers to deal with the inevitable future recessions as well as with unexpected damaging shocks.

For monetary policy, two aspects stand out. As regards operational frameworks, it is essential to combine price stability objectives with the appropriate degree of flexibility. As explored in depth in last year’s Annual Economic Report, low-inflation regimes, in contrast to high-inflation ones, have self-stabilising properties. No doubt this reflects, in part, the fact that, when inflation is mild, it ceases to be a significant factor influencing people’s behaviour. This suggests that, under those conditions, there is room for greater tolerance for moderate, even if persistent, shortfalls of inflation from narrowly defined targets. The approach would also reduce the side effects of keeping interest rates very low for extended periods, such as the build-up of financial vulnerabilities and possible misallocation of resources. As regards institutional frameworks, to buttress the credibility of policy, safeguards for central bank independence, underpinned by appropriate mandates, remain essential. They should become especially valuable in the future, should fiscal positions continue to follow their deteriorating trend.

For fiscal policy, the priority is to ensure fiscal sustainability. Fiscal sustainability is the cornerstone of economic stability and is critical for monetary policy to do its job. Unfortunately, the long-term outlook is grim. Even under favourable assumptions, without sustained and firm consolidation efforts, debt-to-GDP ratios are set to rise relentlessly, threatening safety margins. The looming additional burdens linked to ageing populations, the green transition and geopolitical tensions complicate the picture further. And so does the apparent change in public attitudes following the generous support granted in the wake of the GFC and Covid crises, which has raised expectations regarding government transfers. From an operational perspective, the prominence of financial factors in economic fluctuations merits greater attention when assessing cyclical fiscal positions and fiscal space more generally. From an institutional perspective, there is a need to give more bite to properly designed fiscal rules and fiscal councils, including possibly through constitutional safeguards.

For prudential policy, there is a need for continuous adjustments. The dialectic between financial markets and regulation makes it impossible to stand still. The recent episodes of stress have provided just the latest example. As regards the financial stability risks raised more specifically by fiscal policy, an area that merits particular attention is the favourable treatment of sovereign debt. Adjustments to account effectively for market and credit risk in government securities would also need to give due consideration to the special role that government debt plays in the functioning of the financial system and in central bank operations. Institutionally, just as for monetary policy, it is important to secure the independence of supervisory authorities and to endow them with sufficient resources, both financial and human.

In addition, there is a need to further reflect on crisis management and the financial system’s safety net more generally. Policy actions have, de facto, been extending the safety net with each crisis. And now there are proposals to reduce the scope for runs by extending deposit guarantee schemes further. Once confidence is lost, however, deterring runs and preventing institutions from losing market access would require nothing short of insuring 100% of demandable and short-term claims. This would weaken market discipline far too much and, ultimately, increase solvency risks to unacceptable levels. Moreover, while resolution schemes have been improved and should be improved further, when confidence crumbles, the pressure to extend support becomes insurmountable.

This suggests that expectations should be realistic and that a premium should be put on crisis prevention. It indicates that, refinements aside, there is no substitute for a holistic macroeconomic policy framework that promotes financial and macroeconomic stability, bolstered by a regulatory and supervisory apparatus that boosts the financial system’s loss-absorption capacity. As described in previous Annual Economic Reports, such a comprehensive macro-financial stability framework, in which all policies play their part, is the way to go. Crises cannot be avoided altogether, but their likelihood and destructive force can be contained.

Accordingly, the ambition needed to build such a framework should be combined with realism about what it can deliver and humility in the way it is run. The challenges the global economy is now facing reflect, in no small measure, a certain “growth illusion”, born out of an unrealistic view of what macroeconomic stabilisation policies can achieve. We should avoid falling into the same trap again. Its unintended result has been reliance on a de facto debt-fuelled growth model that has made the economic system more fragile and unable to generate robust and sustainable growth. Overcoming this reliance requires growth-oriented structural reforms (Chapters I and II). Unfortunately, such reforms have been flagging for too long. They should be revived with urgency.

Digitalisation and the financial system: the journey ahead

This takes us to the third and final journey. An important aspect of growth-oriented structural reform is digital innovation in the monetary and financial system. Historically, key innovations in monetary arrangements have enabled new types of economic activity that have led to major advances in the economy. For example, money as ledger entries overseen by trusted intermediaries paved the way for new financial instruments such as bills of exchange that boosted trade by bridging the geographical distance and the timing gap between incurring costs and receiving payment. The gains became even bigger once electronic record-keeping replaced paper ledgers.

Central banks have a duty to lead advances in the monetary system in their role as guardians. The central bank issues the economy’s unit of account and ensures the finality of payments through settlement on its balance sheet. Building on the trust in central bank money, the private sector uses its creativity and ingenuity to serve customers. When viewed through this lens, the fight against inflation is just another aspect of the central bank’s broader duty to defend the value of money. In the same vein, the central bank’s role in innovation serves to defend the value of money by providing it in a form that keeps pace with technology and the needs of society.

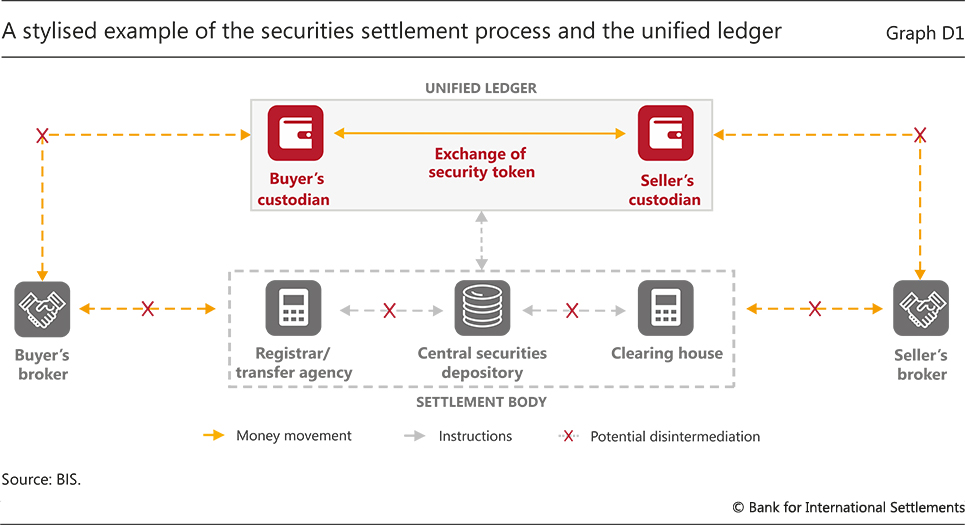

Chapter III charts the course for the future of the monetary and financial system. It argues that the system could be on the cusp of a major technological leap. Following the dematerialisation of money from coins to book entries and the digital representation of those ledger entries, the next key development could be tokenisation – the digital representation of money and assets on a programmable platform. Unlike conventional ledgers, which rely on account managers to update records, tokens can incorporate the rules and logic governing transfers. Money and asset claims become executable objects that the user can transfer directly. Tokenisation could enhance the capabilities of the monetary and financial system, not just by improving current processes but also by enabling entirely new economic arrangements that are impossible in today’s system. In short, tokenisation could improve the old, and enable the new.

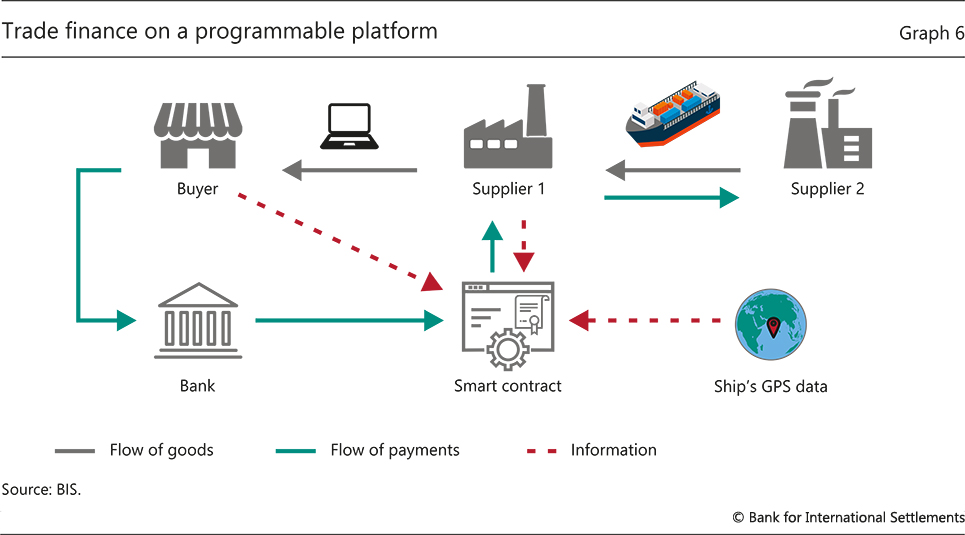

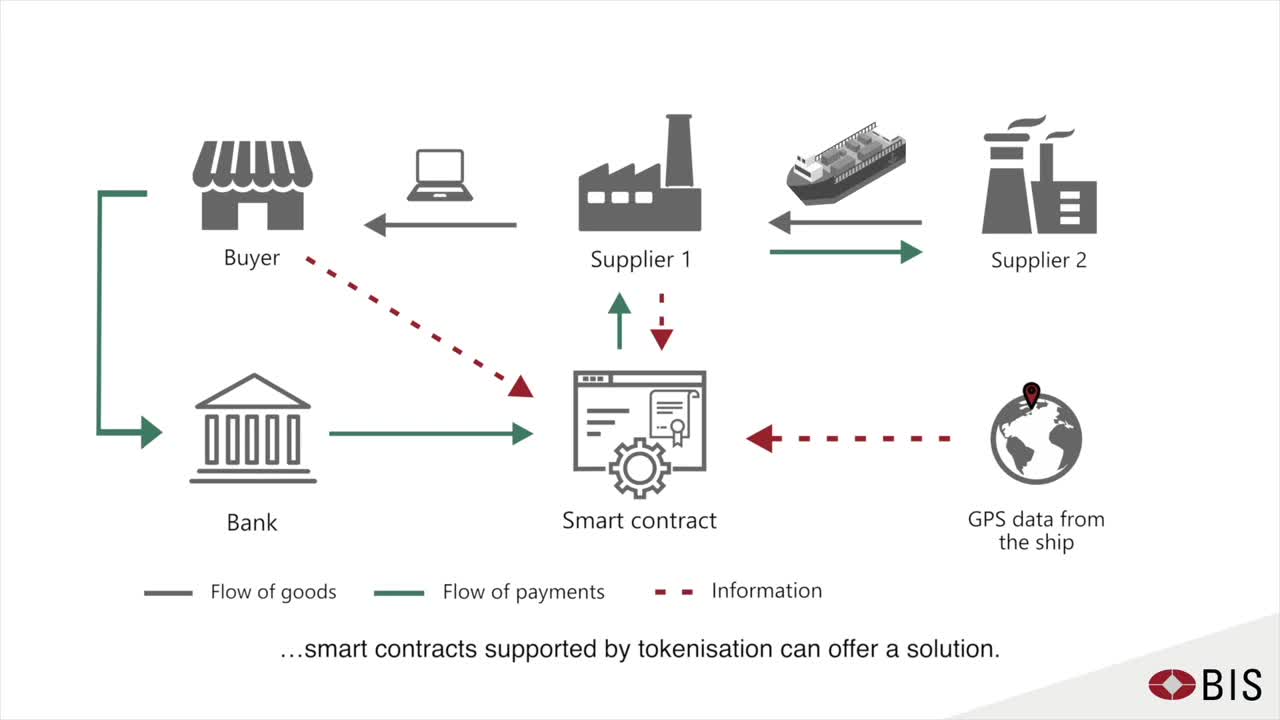

Tokenisation overcomes a key limitation of today’s arrangements. Currently, the digital representation of money and other claims resides in siloed proprietary databases, located at the edges of communication networks. These databases must be connected through third-party messaging systems that exchange messages back and forth. As a result, transactions need to be reconciled separately before eventually being settled with finality. Meanwhile, participants have an incomplete picture of actions and circumstances. This incomplete information, and the associated misaligned incentives, preclude some transactions that have a clear economic rationale. While workarounds, such as collateral or escrow, exist, they do have limitations and create their own inefficiencies. Tokenisation addresses the problems more fundamentally. Resolving FX settlement risk and unlocking supply chain finance are two examples discussed in the chapter. Both are thorny problems in the conventional financial system that are amenable to solution in a tokenised environment.

New demands are also emerging from end users themselves, as advances in digital services in everyday life raise their expectations. Users now demand that the monetary and financial system operate just as seamlessly as the apps on their smartphones. These demands are beginning to outgrow the siloed domains that are holding innovation back.

Chapter III presents a blueprint for a future monetary system. The blueprint envisages a new type of financial market infrastructure (FMI) – a “unified ledger”. The key elements of the blueprint are central bank digital currencies (CBDCs), private tokenised money in the form of tokenised deposits and tokenised versions of other financial or real assets, depending on the particular use case. The success of this endeavour rests on the foundation of trust provided by central bank money and its capacity to knit together key elements of the financial system. To be sure, in crypto, stablecoins that reside on the same platform as other crypto assets also perform a means of payment role. However, for reasons explored at length in last year’s Annual Economic Report, crypto is a flawed system, with only a tenuous connection to the real world. Central bank money is a much firmer foundation. The full potential of tokenisation is best harnessed by having central bank money reside in the same venue as other tokenised claims.

As a new type of FMI, a unified ledger will come with attendant setup costs. While some of the envisaged benefits could also be reaped through more incremental changes to existing systems, history shows that such fixes have their limits, especially as they accumulate on top of legacy systems. Each new layer is constrained by the need to ensure compatibility with the legacy components. These constraints become more binding as more layers are added, holding back innovative developments.

In the near term, a unified ledger could unlock arrangements that have clear economic rationale but which have not been feasible to date due to the limitations of the current system. Over the longer term, the eventual transformation of the financial system will be far more significant. The benefits will be limited only by the imagination and ingenuity of developers, much as the ecosystem of smartphone apps has defied the initial imagination of the platform-builders themselves.

Conclusion

The journey ahead for the global economy and its financial system is hazardous. However, it also offers great opportunities. Steering in the right direction will be far from easy. It calls for a rare mix of judgment, ambition, realism and the political will and capacity to implement the necessary policies. Those policies tend to involve short-term costs as the price to pay for bigger long-term benefits. Fortunately, the journey ahead is not predetermined.

I. Navigating the disinflation journey

BIS Annual Economic Report |

![]() Watch the video (00:02:08)

Watch the video (00:02:08)

with Agustín Carstens, General Manager

Key takeaways

- Inflation peaked in most jurisdictions, but remains well above target. The global economy slowed, although it proved more resilient than many had expected. Clear signs of stress appeared in the financial system.

- There are two key risks to the outlook. First, the next phase of disinflation may become more difficult. Second, macro-financial vulnerabilities loom large amid historically high debt levels at the end of the low-for-long interest rate era.

- Returning inflation to target remains a priority. Fiscal policy should play a key supporting role for monetary policy. In addition, prudential policy should strengthen the financial system further. Weaning growth away from excessive reliance on macro-stabilisation policies is crucial to achieving price and financial stability as a basis for robust, sustainable growth.

The global economy withstood strong headwinds better than expected over the past year. Inflation edged down, as disruptions in global supply chains and in commodity markets waned. Growth slowed, although it proved resilient.

At the same time, signs of strain started to emerge. In particular, financial stress rattled the financial system, engulfing both banks and non-bank financial intermediaries (NBFIs) and prompting a forceful policy response to limit contagion. The strains share a common cause: the system is under stress following the era of low-for-long interest rates. Several strategies adopted to take advantage of that era are now proving ill-suited to the new environment. The strains are also a reminder of the tight monetary-fiscal-financial nexus, as the increase in government bond yields played a key role here.

Even stronger headwinds may lie ahead. Despite the most synchronised and intense monetary policy tightening in recent memory, inflation remains far too high. And there is a material risk of further financial stress.

The next phase of disinflation is likely to be more difficult. Mechanically, base effects are fading away. Substantively, inflation is increasingly driven by the more inertial components, particularly services. The longer inflation lasts, the more likely it is that households and firms will adjust their behaviour and reinforce it.

There are widespread macro-financial vulnerabilities in the system. Private and public debt levels are historically high. Asset prices, notably those of real estate, have started softening on the back of rich valuations. Interest rates may need to stay higher and for longer than financial markets are pricing in. The strains that have emerged so far reflect interest rate risk, but credit losses are still to come. This will further test the resilience of the financial system.

Four major policy challenges stand out. First, monetary policy needs to travel the last mile, bringing inflation back to target. Second, fiscal policy needs to support short-term stabilisation and ensure sustainability. Third, prudential and supervisory policies need to safeguard financial stability, thereby supporting the macroeconomic adjustment. Last but not least, policymakers need to wean growth away from excessive reliance on macro-stabilisation policies and bring monetary and fiscal policies firmly back into a “region of stability” (Chapter II takes a closer look at this challenge).

This chapter first describes the key economic and financial developments over the past year. It then discusses the main macroeconomic and financial risks. Finally, it elaborates on the policy challenges.

The year in retrospect

Inflation moderates, but too early to declare victory

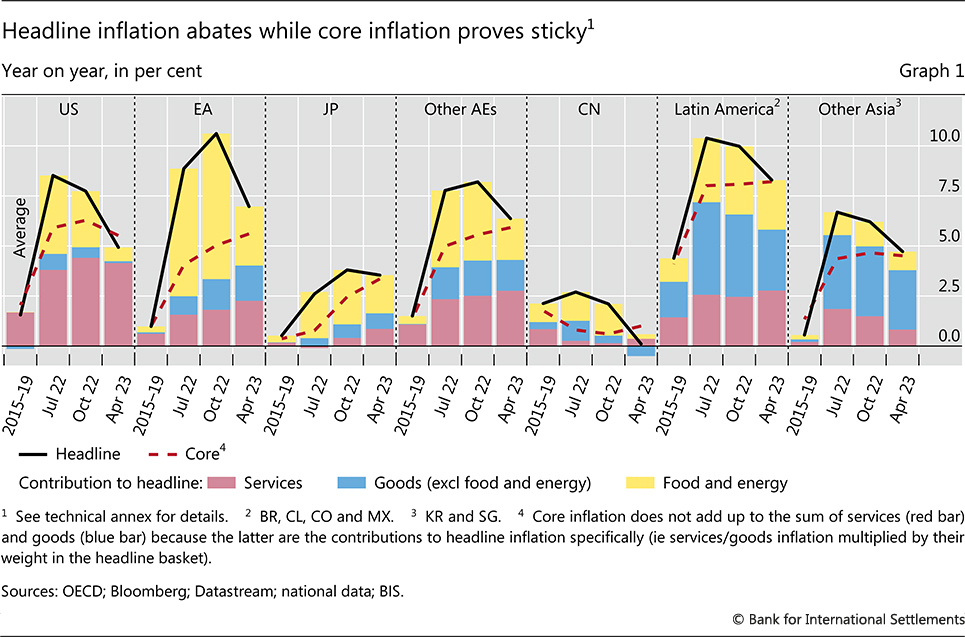

After making a remarkable comeback, inflation continued to be a major policy concern in the year under review (Graph 1). Its persistence was systematically underestimated by public and private sector institutions alike. To be sure, headline inflation came down from the peaks reached in 2022, falling quite notably in most cases. But core inflation proved stickier, either stabilising or continuing to rise. Almost everywhere, inflation remained well above inflation targets. And, importantly, its drivers shifted as the year progressed, with the more inertial components gaining ground.

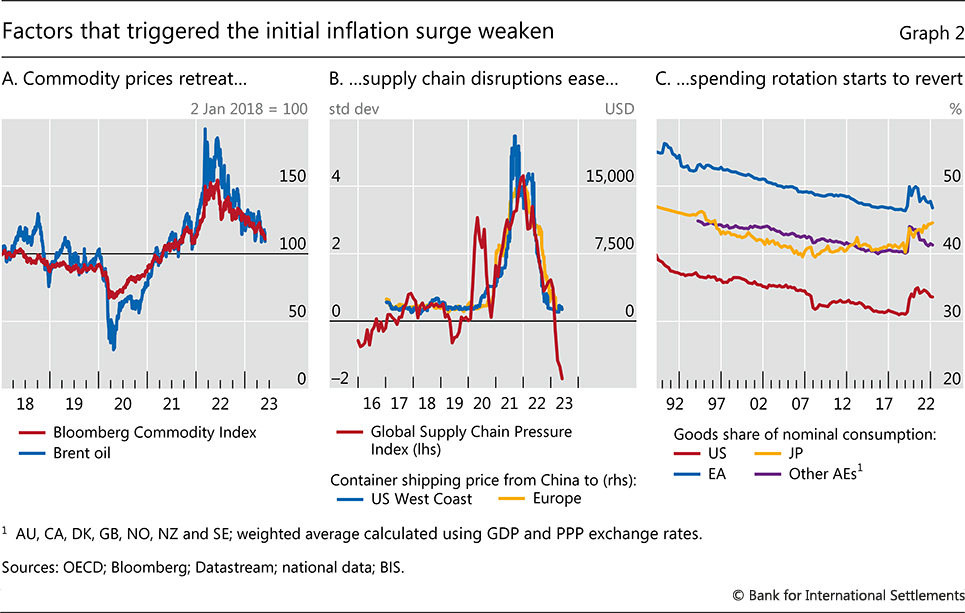

Lower headline inflation reflected, to some extent, both one-off factors and what, in principle, are temporary measures. Strong base effects kicked in, dragging down year-on-year readings. Commodity prices retreated from the highs induced by the war in Ukraine (Graph 2.A). As a result, contributions to inflation from energy and food shrank (yellow bars in Graph 1). In addition, the direct impact of some fiscal measures designed to curb increases in these prices mechanically helped to keep inflation down in the near term.1 The size of the support reached 3% of GDP in some cases. That said, this impact could be reversed should the measures be phased out as planned and, in the case of cap-based measures, if the price of the subsidised commodities were to rise again. And, in the meantime, the support prevented aggregate demand from falling, thereby contributing to tight product and labour markets.

Graph 1

A longer-lasting amelioration came from easing global supply chain pressures, which largely normalised, allowing backlogs to be cleared (Graph 2.B). This affected primarily the prices of goods, which are much more heavily traded than services. These prices tended to rise more slowly and, in some cases, actually fell (blue bars in Graph 1). The pressure on goods prices was also eased by the ongoing reversion of the pandemic-related shift in consumption patterns away from services to goods (Graph 2.C).

That same rotation, however, boosted services price growth, which continued to rise (red bars in Graph 1). In the United States, the services component once again became the main factor behind inflation. Its contribution also slowly rose in other advanced economies (AEs) and in Latin America.

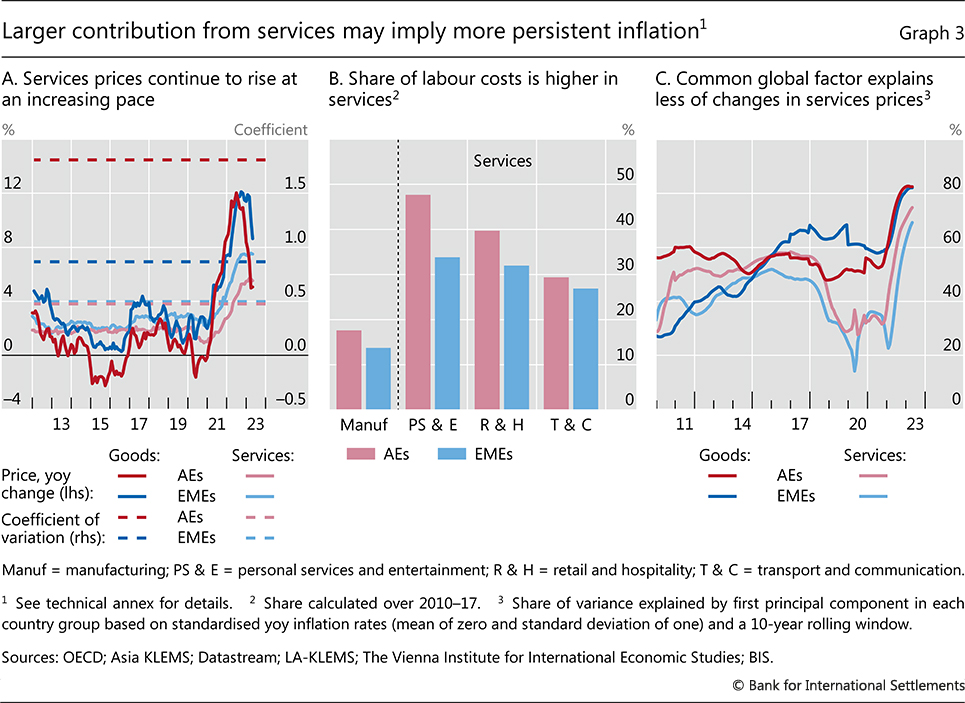

This shift in drivers of inflation towards services is likely to increase its persistence. The rate of change in services prices has historically been much less volatile than that for goods (dotted lines in Graph 3.A). Part of the explanation is that the share of labour in total costs in services is about twice as large as in manufacturing (Graph 3.B). This tightens the link between prices and wages. Not only are wage increases in general more inertial than other cost components, but they also tend to be more domestically driven in services, as the sector is less exposed to international competition. Indeed, the fraction of the variance of price changes explained by a global common factor has generally been lower for services, although it has risen recently owing to the widespread nature of the inflation surge (Graph 3.C).

Synchronised monetary tightening ends low-for-long

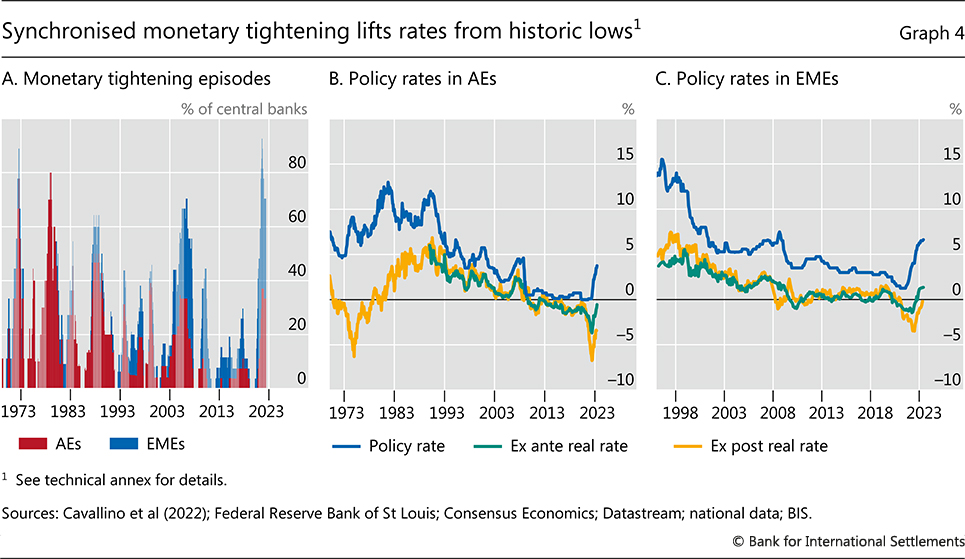

The inflation surge has led to the most synchronised and intense monetary policy tightening in decades.2 Almost 95% of central banks hiked their policy rates between early 2021 and mid-2023 (Graph 4.A). Historically, this share has rarely exceeded 50%, surpassing 80% only during the oil price shocks of the 1970s. Emerging market economy (EME) central banks raised policy rates at twice the historical pace, and AE central banks at a roughly similar one.3 4 Even so, policy rates are still below inflation and, in some AEs below inflation expectations, implying negative real rates (Graph 4.B and 4.C). At the same time, major AE central banks started to gradually shrink their balance sheets, with Japan as the exception. Quantitative easing turned into quantitative tightening.

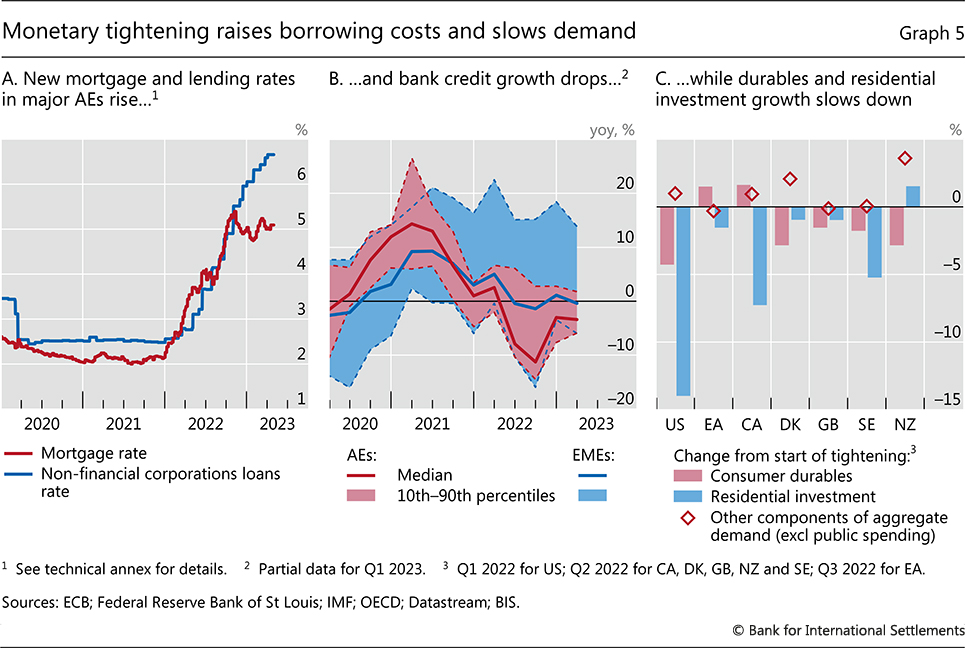

The transmission of monetary tightening to lending rates was mostly swift and began to weigh on aggregate demand. Borrowing costs rose for corporates and households alike (Graph 5.A). Bank lending standards tightened and bank credit contracted, especially in AEs (Graph 5.B). Consequently, spending weakened. The deceleration was led by the most interest rate-sensitive components of expenditure, such as consumer durables, and the housing market cooled in many economies (Graph 5.C).

The economy slows, but manages to avoid recession so far

Overall, global growth slowed from 6.3% in 2021 to 3.4% in 2022, weakening further in the first quarter of 2023 (Graph 6.A). The slowdown was most pronounced in AEs, from 5.7 to 2.8%. EMEs fared better, still growing at 4% in 2022 as a whole compared with 7.3% in the previous year. This was despite China recording a growth rate of only 3%, reflecting setbacks from large Covid-19 outbreaks and the drag from the real estate sector.

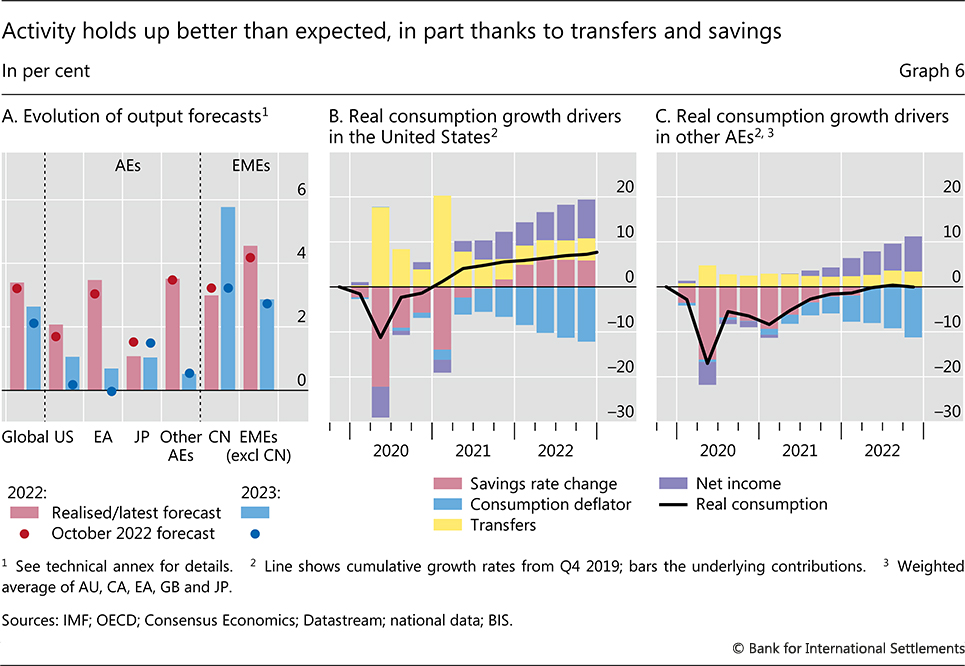

Still, activity held up better than expected in a number of key jurisdictions, and the much feared global recession did not materialise. Relative to the forecasts made early in the review year, growth outcomes in 2022 surprised on the upside in the United States, the euro area and most EMEs, with China an exception to the pattern. As high-frequency indicators remained robust in many jurisdictions, growth forecasts for 2023 were revised upwards as the new year started, although the consensus still saw a considerable slowdown for the year as a whole, to 2.6%.

The relative strength of economic activity and the upgrade of expectations for 2023 reflected three main factors.

Graph 6

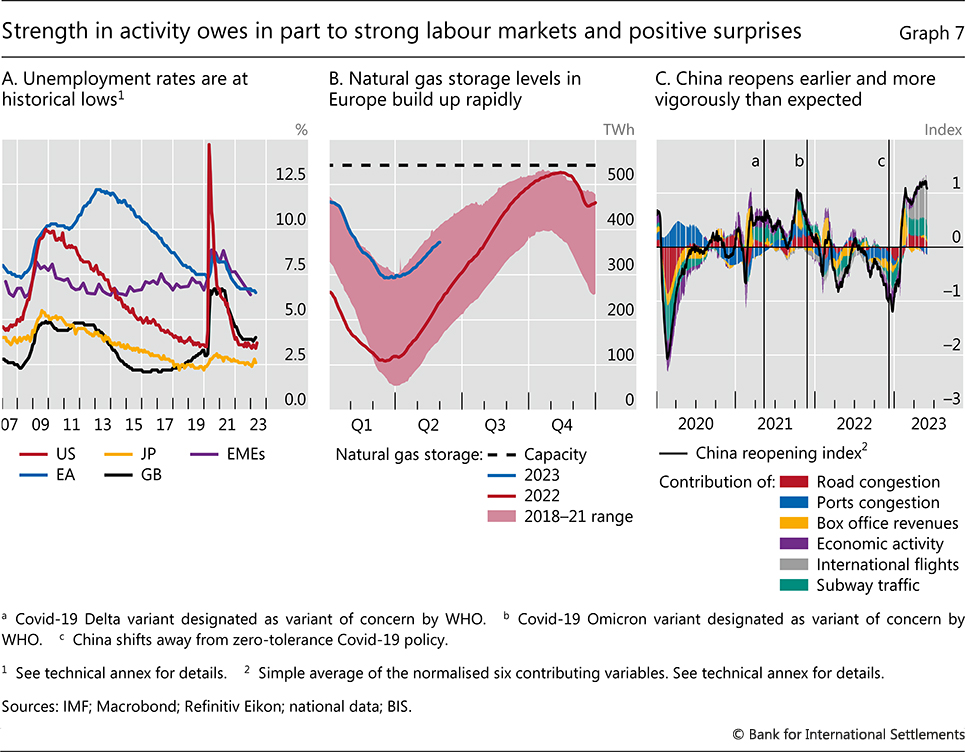

First, consumption remained robust. Excess savings accumulated during the pandemic, not least thanks to higher saving rates and fiscal support (red and yellow bars, respectively, in Graphs 6.B and 6.C). Once Covid-related restrictions were lifted, households drastically cut their saving rates, to pre-Covid levels in most AEs and to even lower ones in the United States. Further, buoyant labour markets bolstered income (purple bars in Graphs 6.B and 6.C). Unemployment rates fell to multidecade lows, especially in AEs (Graph 7.A). Job creation was strong in both AEs and EMEs while job vacancy rates remained high, around record levels in the United States and Europe.

Second, the energy crisis proved far less consequential than expected. A relatively mild winter and the rapid build-up of gas storage helped prevent the deep and widely forecast recession in Europe (Graph 7.B).5 And, in many jurisdictions, fiscal support insulated households and firms from the impact of higher energy prices.

Third, the rapid reopening of the Chinese economy in January, after the country abandoned its zero-Covid strategy in December 2022, boosted domestic activity (Graph 7.C). This also lifted activity abroad, although to a lesser extent than in the past, given the services-driven nature of the rebound (Box A).

Financial system shaken by bank failures

Financial markets and the financial system more generally started to adapt to the abrupt end of low-for-long interest rates but the process was far from smooth. A broad disconnect emerged between financial market pricing and central banks’ announced policy path. And rising signs of stress appeared in the financial system.

Box A

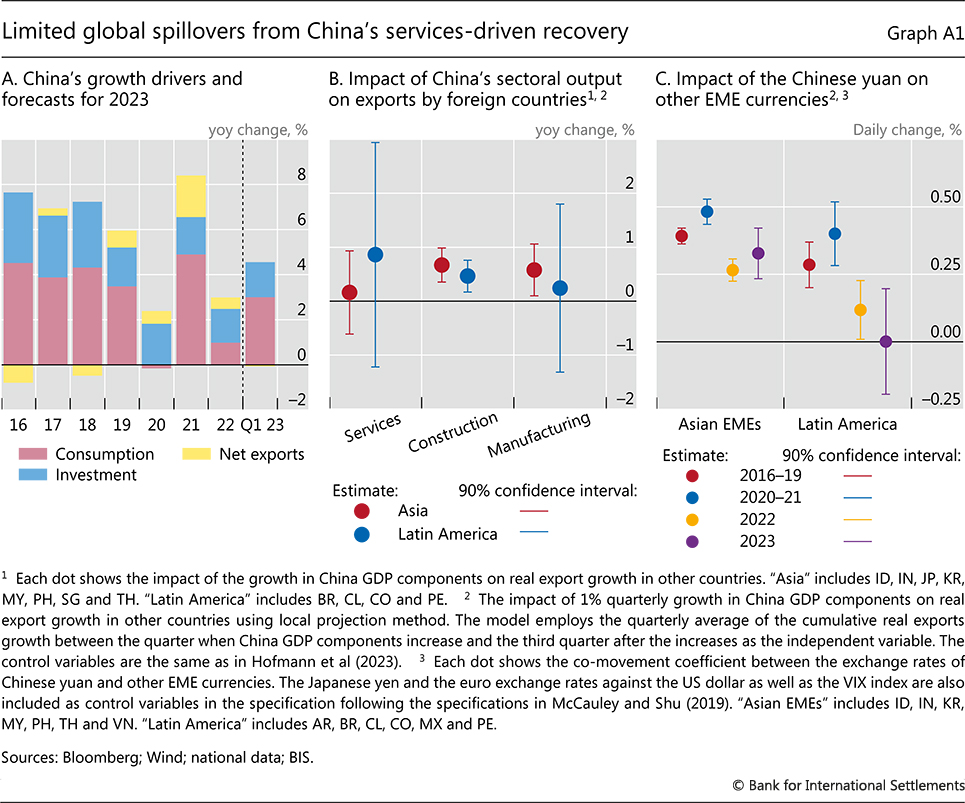

Spillovers from China’s reopening

China abandoned its dynamic zero-Covid policy in late 2022, starting to relax pandemic restrictions in November and reopening its borders in early January 2023. The timing and pace of reopening surprised the market, whose consensus as of early November 2022 was for a gradual reopening from March 2023.

After the reopening, the Chinese economy rebounded strongly, driven mainly by services. The Q1 2023 GDP advanced 4.5% year on year (Graph A1.A), topping the market consensus. Growth forecasts for 2023 were revised up from 4.5% in November 2022 to 5.8% in May 2023. The services sector (eg catering and tourism) benefited most from improved mobility, and the non-manufacturing PMI in March 2023 reached its highest level in more than a decade. The manufacturing sector started to recover from June 2022, after supply chain pressures eased, but faces headwinds in 2023, as external demand flags. Recovery in the construction sector is also likely to be modest, given weak sentiment in the real estate market.

Growth spillovers to the rest of the world from a services-driven recovery should be limited, because services are less tradable and more oriented towards domestic demand. This contrasts with construction and manufacturing, which require imports of raw materials and intermediate goods from other countries. Growth in construction and manufacturing in China had significant positive effects on other emerging market economy (EME) exports between 2004 and 2019 (Graph A1.B). For example, a 1% quarterly growth in construction activity increased exports to China from Asian manufacturing exporters by 0.7%, and those from Latin American metal exporters by 0.5% on average for the first four quarters, while a 1% growth in manufacturing output increased Asian exports to China by 0.6%. In contrast, services had no significant impact.

For example, a 1% quarterly growth in construction activity increased exports to China from Asian manufacturing exporters by 0.7%, and those from Latin American metal exporters by 0.5% on average for the first four quarters, while a 1% growth in manufacturing output increased Asian exports to China by 0.6%. In contrast, services had no significant impact.

The spillover to global inflation could be small as well. One important channel through which China’s growth can affect global inflation is commodity prices. In particular, a pickup in manufacturing and construction activity in China would increase demand for commodities (metals in particular for construction), boosting their prices. Indeed, in 2004–19, a 1% increase in manufacturing production raised broad commodity prices by 2.2% after two quarters, while a 1% increase in construction activity raised metal prices by 0.9%. Again, services had no impact.

Consistent with a smaller spillover from China’s recovery this time around, financial assets in EMEs showed weaker co-movement with those in China in 2023 than in previous years. For example, the currencies of Asian and Latin American EMEs used to show strong co-movements with the Chinese yuan (Graph A1.C, red and blue dots). However, the co-movement weakened in 2022 when China diverged from some other parts of the world in terms of pandemic policy, the growth path and the monetary policy stance (yellow dots). The correlation remained at low levels for Latin America until May 2023, consistent with the expectation of limited spillover (purple dots). The co-movements of equity market returns and those of portfolio capital flows also diminished.

The eight Asian manufacturing exporters are India, Indonesia, Japan, Korea, Malaysia, the Philippines, Singapore and Thailand. The four Latin American metal exporters are Brazil, Chile, Colombia and Peru. Consistent with the dependence of spillovers on growth drivers, China’s spillover to the rest of world has varied over time. In particular, a 1% increase in China’s GDP was associated with 0.4% GDP growth in the rest of world in 2004–08 (when China actively participated in global trade after its entry into WTO in 2001), with 0.6% growth in 2009–14 (when China introduced large-scale investment projects after the 2007–09 Great Financial Crisis), and with 0.1% growth in 2015–19 (when China reduced reliance on investment for growth but focused more on consumption). The correlation between China’s equity market returns and those in Asian and Latin American EMEs was relatively high at 0.34 in 2016–19 and 0.36 in 2020–21 but fell to 0.17 in 2022 and Q1 2023. In contrast, the correlation of bond market returns stayed around zero throughout these periods. Similarly, after controlling for economic fundamentals, a one standard deviation increase in daily portfolio capital flows to China was associated with an increase in portfolio capital flows to six Asian EMEs and one Latin American country by 0.11 and 0.13 standard deviations in 2016–19 and in 2020–21, respectively, but its impact declined to 0.09 standard deviations in 2022 and Q1 2023.

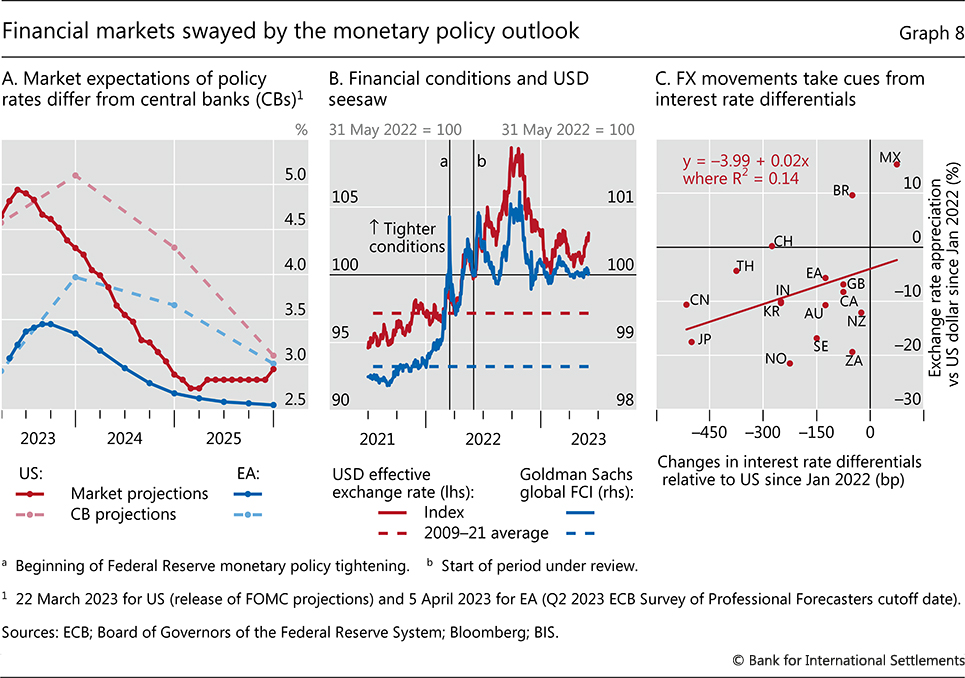

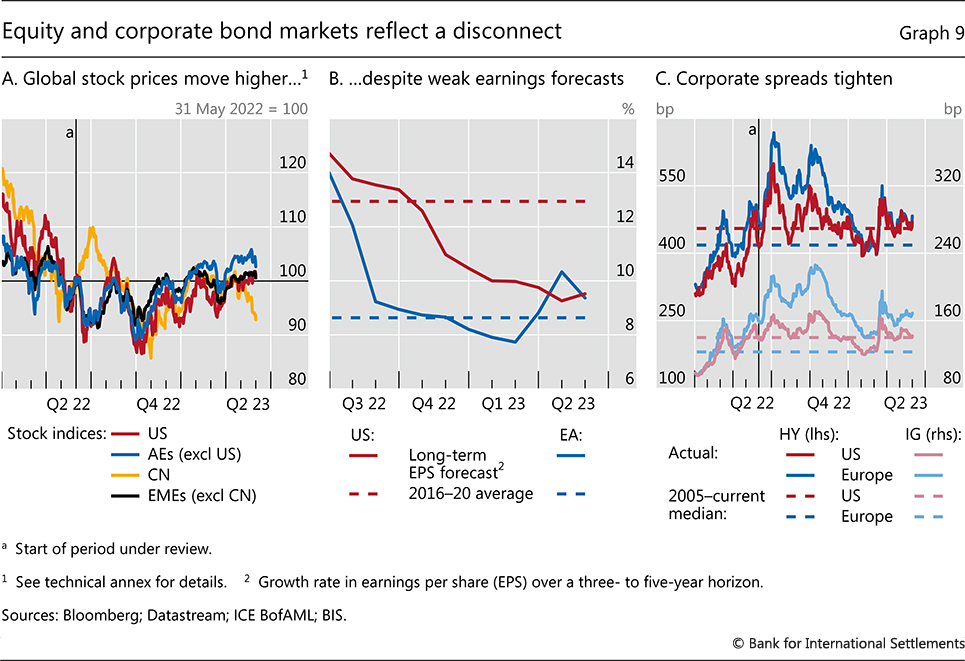

The disconnect between market expectations and central bank plans was evident in the dynamics of financial conditions. As markets were swayed by the shifting odds of inflation staying high and the economy entering a recession, participants continuously re-evaluated how central bank actions would evolve. Expectations of future rates remained lower than central banks’ projections, with investors anticipating rate cuts already in 2023 (Graph 8.A). After considerable tightening in 2022, by some measures, financial conditions tightened marginally during the period under review (Graph 8.B). They remained tighter than historical averages.

Foreign exchange movements largely followed those of financial conditions, taking their cue from the relative strength of the economies and the corresponding monetary policy outlooks. The US dollar generally appreciated through the third quarter of 2022, before weakening moderately against most currencies. By and large, the depreciation against the dollar was larger for the currencies of countries where the policy rate increased less than in the United States. The Japanese yen and the euro touched multidecade lows. Countries where monetary tightening had started earlier and interest rates had reached higher levels, such as Mexico and Brazil, actually saw appreciations (Graph 8.C). In general, EMEs absorbed the sharp tightening of global monetary conditions in an orderly way.

The disconnect between financial market expectations and central bank communications was also evident from the dynamics of risky assets. Equity markets finished the review period marginally higher (Graph 9.A), despite weak earnings forecasts, especially in the United States (Graph 9.B). Measures of implied equity volatility hovered below historical averages for most of 2023. In credit markets, spreads marginally tightened, remaining in line with historical norms in the United States and somewhat above in Europe (Graph 9.C).

Against this backdrop, increasing signs of stress emerged in the financial system in late 2022 and early 2023, in large part due to higher interest rates.

First, leveraged strategies to hedge against drops in interest rates came under pressure. As the UK “mini-budget” announcement in September 2022 sent gilt rates soaring, such strategies generated losses for the so-called liability-driven investment (LDI) funds in which UK pension funds had invested. To meet the ensuing collateral calls, LDI funds needed cash infusions, which pension funds failed to provide promptly enough. As their solvency positions worsened, LDI funds had to deleverage by selling gilts, putting further upward pressure on yields and setting off a full-fledged spiral. The Bank of England intervened forcefully and swiftly through temporary asset purchases to calm the market.

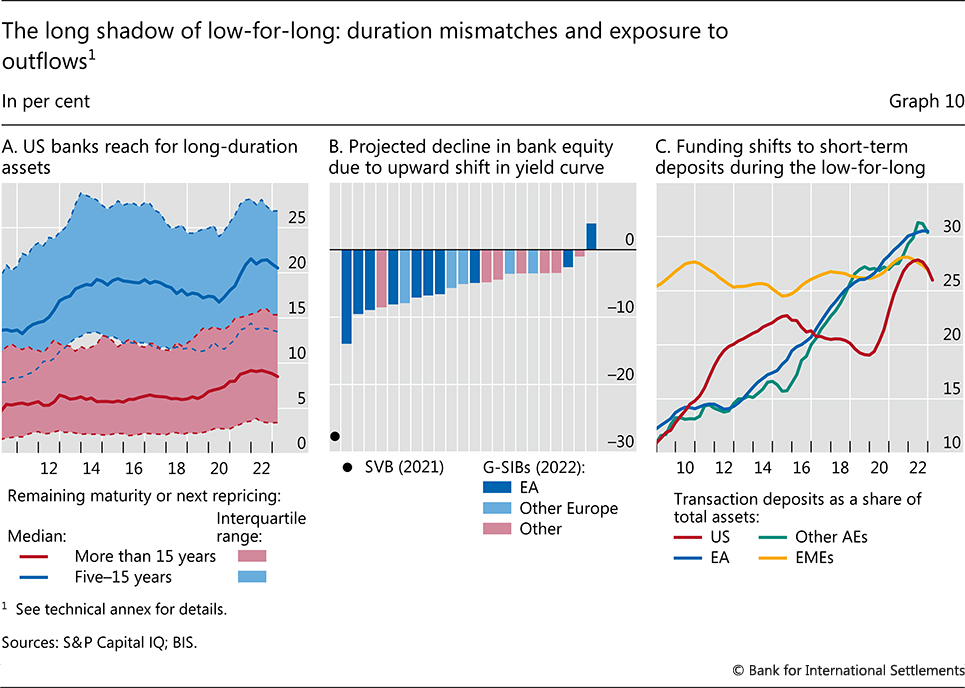

The sharp increase in interest rates also put the spotlight on banks. To the extent that they could reprice their assets, banks benefited from the impact of rising interest rates on net interest margins (Box B). However, during the low-for-long era, many had accumulated fixed rate mortgages and long-term government bonds (Graph 10.A), which declined steeply in market value when interest rates rose. Banks are generally required to assess and manage their exposure to changes in interest rates, including under scenarios of upward shifts in the yield curve (Graph 10.B). In addition to hedging with derivatives, banks often base their interest rate risk management on deposit stickiness. This feature has traditionally allowed banks to keep their funding costs in check by passing only a fraction of policy rate rises to deposit rates. As the share of short-term – and thus potentially flighty – deposits has risen (Graph 10.C),6 an increase in their interest rate sensitivity undermined the risk management strategies of some banks.

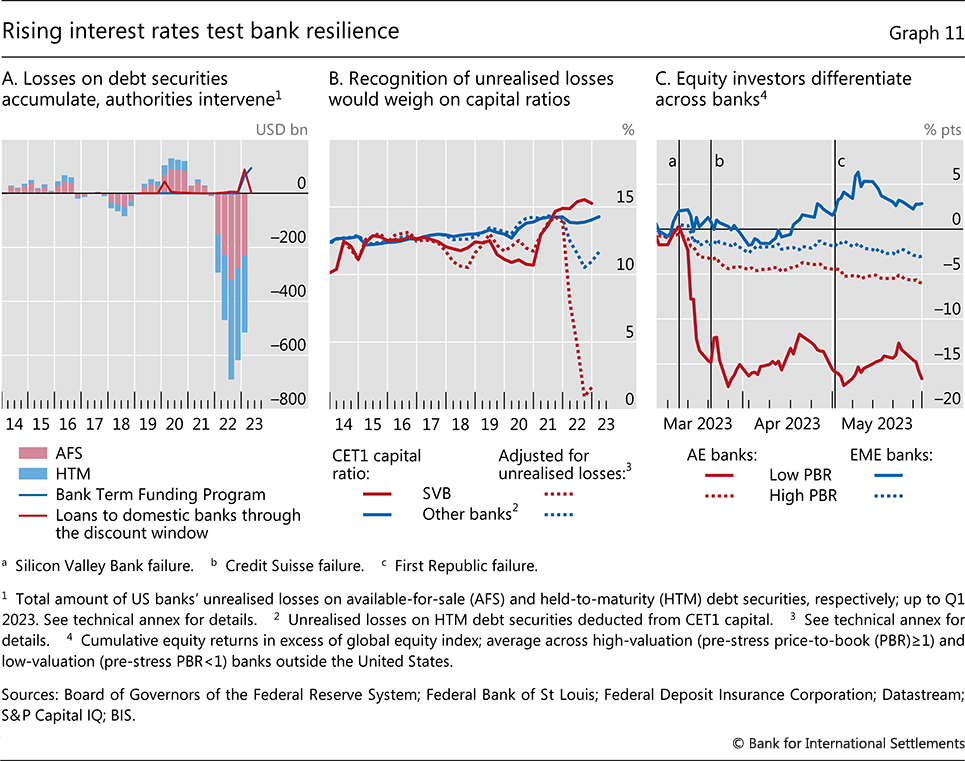

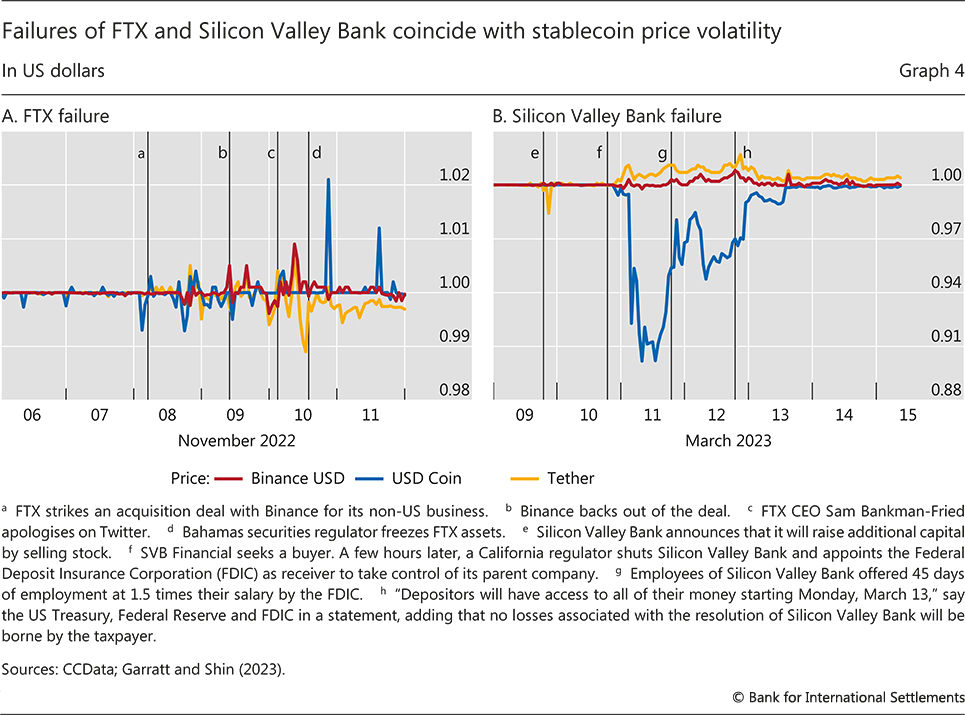

Mismanagement of interest rate risk, among other factors, drove the first major bank failures since the Great Financial Crisis (GFC). Already by late 2022, many US banks had sizeable market value losses on their debt securities holdings (Graph 11.A). More than half of the losses were not reflected on balance sheets, on the accounting assumption that banks would hold the attendant assets to maturity.7 However, as a loss of confidence in some of the smaller and thus more lightly regulated banks triggered a deposit flight, these banks had to liquidate some of their “held-to-maturity” assets and recognise immediate capital losses (Graph 11.B). These intertwined interest rate and run risks materialised forcefully for Silicon Valley Bank (SVB), a regional bank that collapsed in early March (Box C).

Box B

Rising policy rates and the outlook for banks’ net interest margins

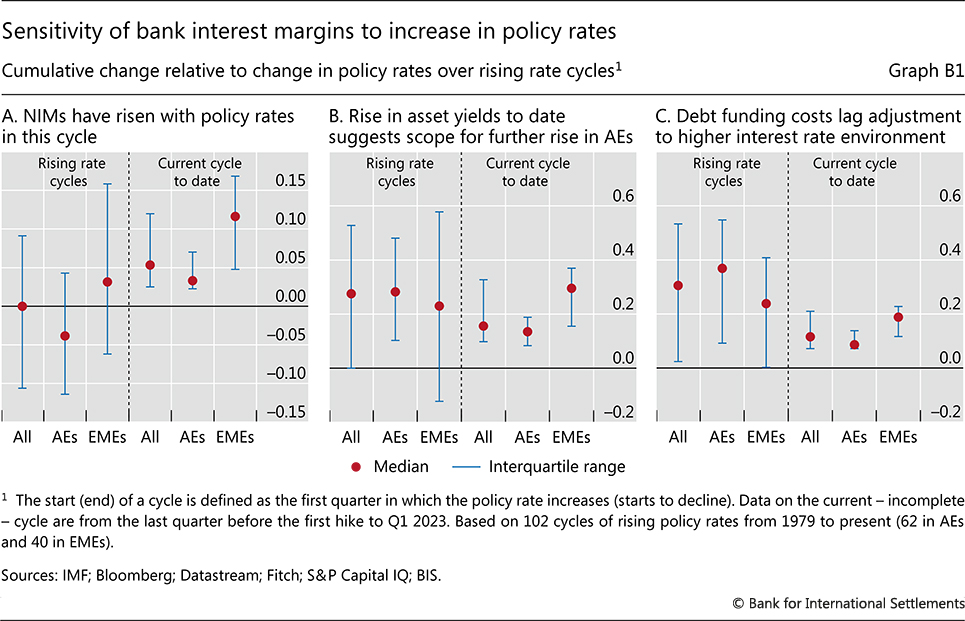

While monetary tightening has exposed banks’ interest rate risk, the end of the low-for-long era is also expected to ease pressures on their income. In assessing banks’ performance, valuation losses on fixed rate assets will need to be set against higher interest income on variable rate assets and new lending. Drawing on evidence from past tightening episodes, this box assesses the effect of the recent rises in policy rates on net interest margins (NIMs), ie the difference between the yield on banks’ interest-earning assets and the cost of funding their debt.

During the current cycle, there was a general increase in NIMs (Graph B1.A). Since the start of the current cycle, NIMs have increased by more than 10 basis points in EMEs and nearly 5 basis points in AEs for every 100 basis point increase in the respective policy rate.

The recent rise in NIMs was driven more by the muted response in banks’ cost of debt than by the return on interest-bearing assets. In EMEs where the current cycle is more advanced, yields on interest-earning assets increased in line with past cycles, whereas the adjustment in debt funding costs is still lagging behind. The pickup in yields in AEs, by comparison, has yet to fully unfold if compared with the endpoint in previous cycles (Graph B1.B). This is consistent with banks’ shift to long-duration assets during the low-for-long era, which reduced the responsiveness of interest income to changes in policy rates. The increase in banks’ cost of debt, by contrast, has remained far behind historical endpoints (Graph B1.C). This probably stemmed from the higher proportion of non-interest-bearing deposits in many AE banking sectors.

The outlook for NIMs depends on how yields and costs will adjust to the policy path. Historically, NIMs often returned to their initial level, or even fell slightly in AEs, over the course of a rising rate cycle (Graph B1.A). At the current juncture, banks are expected to benefit from additional increases in yields when low-yielding fixed rate loans and mortgages expire, and borrowers refinance at higher rates. However, the availability of higher-yielding investments could also put upward pressure on bank funding costs. Relative to past episodes, this effect could unfold more rapidly due to the larger share of overnight deposits that can be withdrawn quickly. The threat of such withdrawals would require banks to pass on the increase in policy rates more swiftly to creditors in order to secure funding.

Return on interest-earning assets is defined as banks’ gross interest income divided by total interest-earning assets. Cost of funding is defined as banks’ interest expenses divided by total funding.

Box C

Recent bank failures

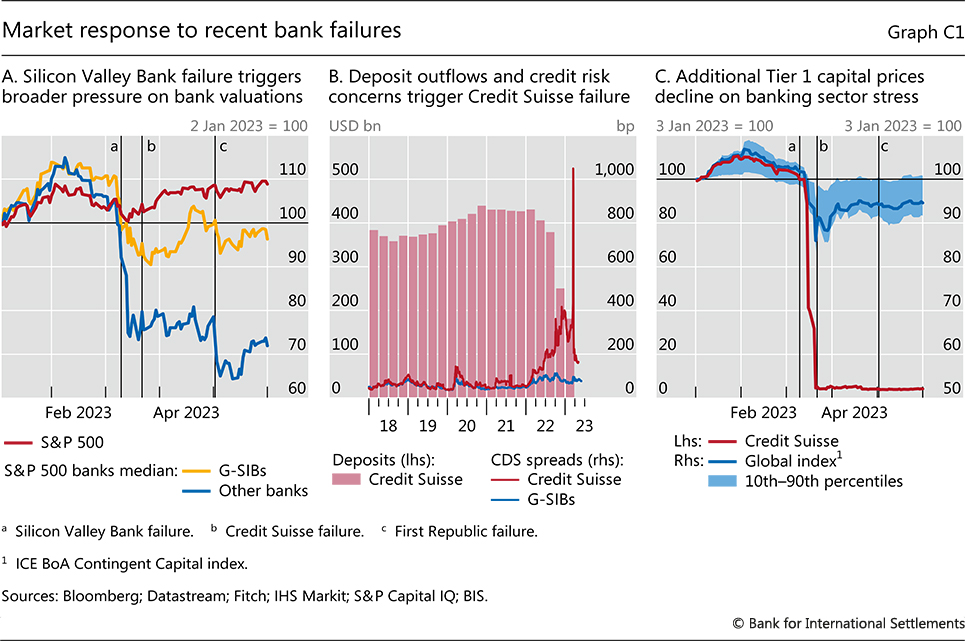

Market tremors in March 2023 highlighted how risk management deficiencies at individual banks can undermine the confidence of depositors and other investors, leading to a funding crisis that can reverberate through the financial system. This box reviews recent bank failures and attendant market responses.

Silicon Valley Bank (SVB), which was the 16th largest US bank as measured by total domestic assets at end-2022, went into receivership on 10 March 2023. SVB had accumulated significant, albeit unrealised, valuation losses on its unhedged securities portfolio due to rising rates over the course of 2022. In early March, confronted with persistent deposit outflows, the bank had to sell securities and recognise a large loss and the attendant impact on its capital position. Unable to raise new equity to rebuild this position, the bank collapsed within just a few days on the back of a concerted, unprecedentedly fast run by its mostly uninsured corporate depositors.

Following the failure, concerns spread immediately about similar vulnerabilities at other banks, leading to significant falls in the valuations of small and mid-sized banks amid large deposit outflows (Graph C1.A). After suffering a run by uninsured depositors, Signature Bank was closed two days after SVB’s failure. First Republic, also struggling with a combination of losses on long-duration assets and large deposit outflows, initially managed to secure alternative funding, including from major US banks. However, the bank ultimately failed given the persistence and scale of deposit outflows and, after entering receivership, was sold to JPMorgan Chase.

Concerns also spilled over to banks outside the United States. In particular, Credit Suisse entered the eye of the storm. This bank’s profitability and reputation had already suffered due to risk management deficiencies and significant performance setbacks in recent years. Market scepticism about the bank worsened through 2022 amid large deposit withdrawals, rising credit spreads and outflows of assets under management. The switch to a risk-off environment in March 2023 was the tipping point, with the bank’s CDS spreads jumping to levels indicating imminent default (Graph C1.B). To alleviate systemic risk concerns, Swiss authorities facilitated and enforced a takeover by UBS.

The Credit Suisse takeover shook the market for Additional Tier 1 (AT1) capital – instruments that can be written down or converted to equity when a bank becomes unviable. As the takeover entailed the writedown of Credit Suisse’s entire AT1 capital, this led to broader uncertainty about when and how these instruments would absorb losses at failing banks. The immediate upshot was significant price declines in the AT1 market, notably for instruments issued by European banks (Graph C1.C). New issuance on this market has been subdued, even if prices have since partially recovered after European authorities provided additional clarity on the hierarchy of AT1 investors relative to equity holders in the event of bank failure.

Graph 10

The realisation of interest rate risk reverberated through the US banking sector in the first half of 2023. Small and mid-sized banks suffered significant deposit outflows, forcing the closure of first Signature Bank and then First Republic Bank. At the same time, US global systemically important banks (G-SIBs) saw significant inflows from depositors searching for safe havens.

Investors’ concerns spread to banking sectors in several other AEs. Banks that had already faced persistent market scepticism, as indicated by a low price-to-book ratio (PBR), were hit particularly hard. Credit Suisse – a G-SIB which had been struggling with large fund outflows and a series of setbacks (see Box C) – failed to rebuild market trust and – after writing down its contingent convertible bonds to absorb losses – was taken over by a competitor. Relative to global equity markets, other AE banks with low PBRs also registered deeply negative stock returns (Graph 11.C). This stood in contrast to the more modest decline for high-PBR banks in AEs and banks in EMEs.

Again, authorities responded forcefully to contain contagion and deployed a number of crisis management tools to curb systemic risks. In the United States, authorities invoked the so-called systemic risk exception – previously used in the GFC – to stem more widespread runs by guaranteeing the uninsured deposits of SVB and Signature Bank. In addition, the Federal Reserve established the Bank Term Funding Program (BTFP), offering loans to banks that pledged qualifying government securities, valued at par and thus above market value. The BTFP complemented lending through the Federal Reserve’s discount window, which soared in the immediate aftermath of SVB’s failure but has come down since then (Graph 11.A). In Switzerland, the public sector backed the emergency takeover of Credit Suisse, with the central bank pledging significant liquidity support and the government extending guarantees to shield the central bank from potential losses. Furthermore, to facilitate the takeover, the government guaranteed to cover part of future losses in relation to the disposal of the failed bank’s legacy assets.

Key risks on a turbulent path

Against this broad macroeconomic and financial backdrop, what is the outlook for the global economy?

Consensus forecasts are rather benign. While forecasters do see lower growth and inflation still above target, the slowdown is rather mild and the fall in inflation substantial. Banking woes are expected to be contained.

Two risks loom large, however – quite apart from those of a more political nature, such as an intensification of geopolitical tensions. First, disinflation could well turn out to be harder than expected – the “last mile” challenge. Second, the end of low-for-long could further test the global financial system, with the crystallisation of macro-financial risks to threaten growth.

This combination of risks is rather unique by post-World War II standards. It is the first time that, across much of the world, a surge in inflation has coexisted with widespread financial vulnerabilities. The longer the inflation persists, the stronger and longer the required policy tightening, and hence the bigger the financial stability risks.

The “last mile” may pose the biggest challenge

Getting back to target is likely to be harder than the first phase of the disinflation journey. There are several reasons why. Beyond fading base effects and the increasing role of inertial components of inflation, households and firms may adjust to persistently higher inflation by trying to recoup previous losses and then seeking to avoid future expected ones through their wage- and price-setting decisions.8 Moreover, as time goes by and higher policy rates propagate through the system, the economy will weaken and further financial stress may arise. This means less pressure on prices but, at the same time, tougher trade-offs involving activity. In some cases, there may be political pressure on central banks to keep interest rates low, requiring them to reiterate the commitment to deliver price stability through both communication and action. Such dynamics may be especially relevant among those EMEs where institutional safeguards are weaker, inflation expectations are less anchored and indexation is more prevalent.

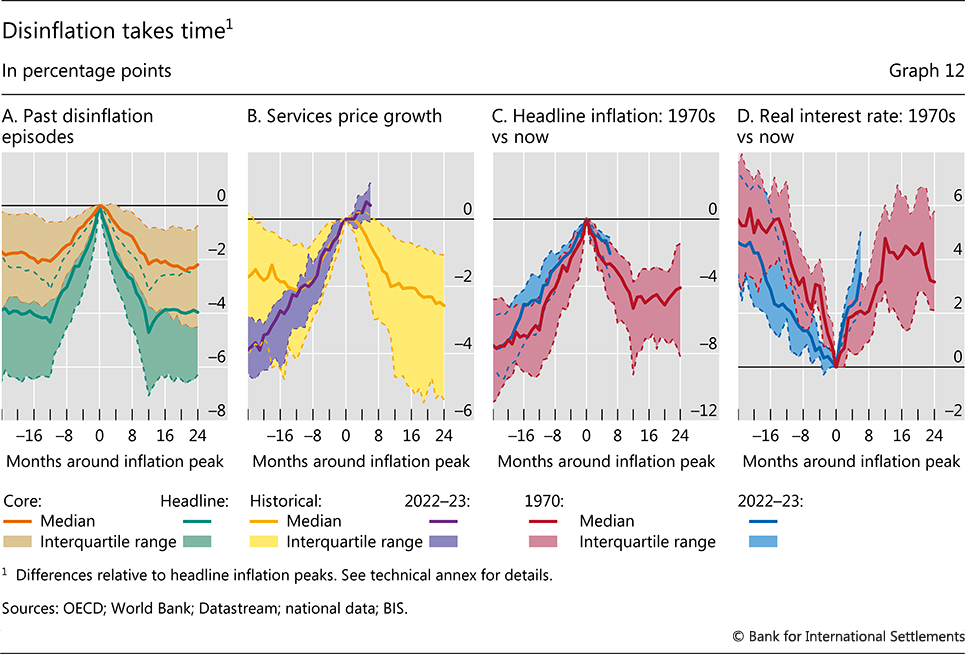

Admittedly, in previous disinflation episodes, headline inflation typically returned to the pre-peak levels (or even lower) in the space of one to two years (Graph 12.A). Core inflation tended to follow a similar path.

However, a number of features set the current episode apart from previous ones and indicate that disinflation may prove difficult. First, services prices have risen much faster and their rate of change has not yet peaked (Chart 12.B). This could mean a potentially longer disinflation journey. Second, rather than the median episode, the current surge more closely resembles the 1970s – when a “first mile” of disinflation was achieved in the space of about one year but inflation thereafter declined only gradually: after two years, it was still generally above its pre-surge level (Graph 12.C). In fact, the pace of disinflation so far has been even slower than in the 1970s – although the tightening has proceeded at a faster pace (Graph 12.D).

Crucially, then, what is the likelihood of a transition to a high-inflation regime, such as the one in the 1970s?

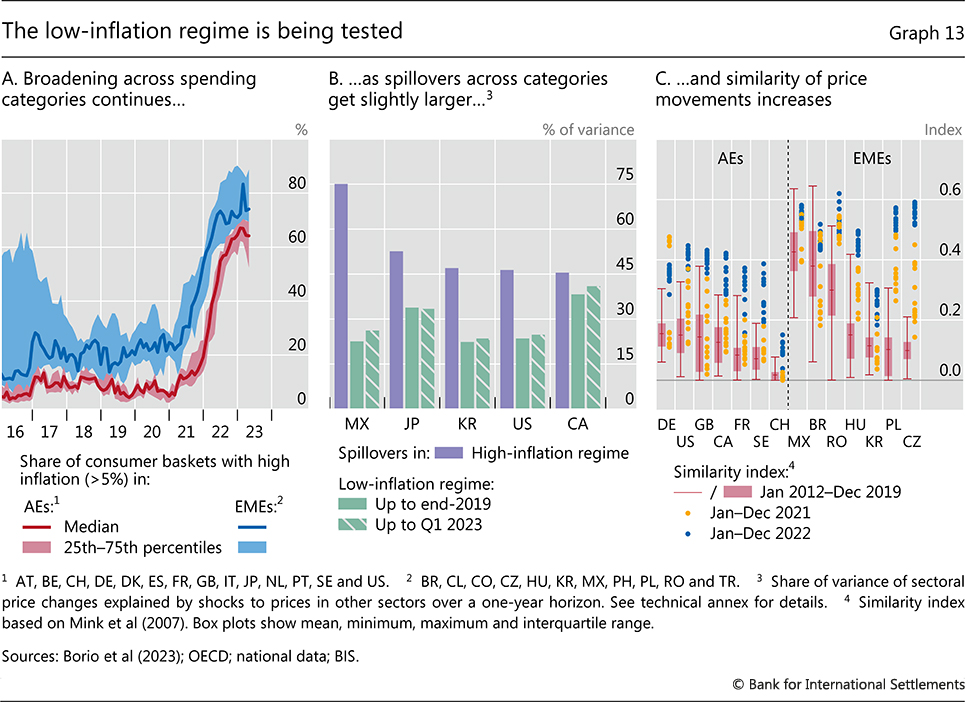

Several indicators point to possible obstacles along the disinflation journey and suggest that the low-inflation regime will continue to be tested. First, after a steep rise, the share of items in the consumer price index whose prices increased at a fast rate has not come down (Graph 13.A). Second, price spillovers across consumption categories are slightly larger than they were in the recent past when inflation was low (Graph 13.B). This means that increases in the price level due to price shocks in one category will propagate to others, raising the likelihood that they will lead to sustained inflation rather than die out. Third, price changes across categories are becoming increasingly similar (Graph 13.C), implying that differences in consumption patterns across consumers and input costs across firms matter relatively less, so that the general price level becomes more relevant for individual decisions. This tends to be a useful indicator of inflation persistence, ie when the similarity index is high, so is the probability that inflation in the next period will be at least as high as in the current one.9 These signals, taken together, suggest that households and firms are responding more strongly to the higher inflation rates.

Looking ahead, two closely related factors could signal a shift in inflation norms and tip the disinflation process off course: self-sustaining wage-price dynamics and a de-anchoring of inflation expectations.

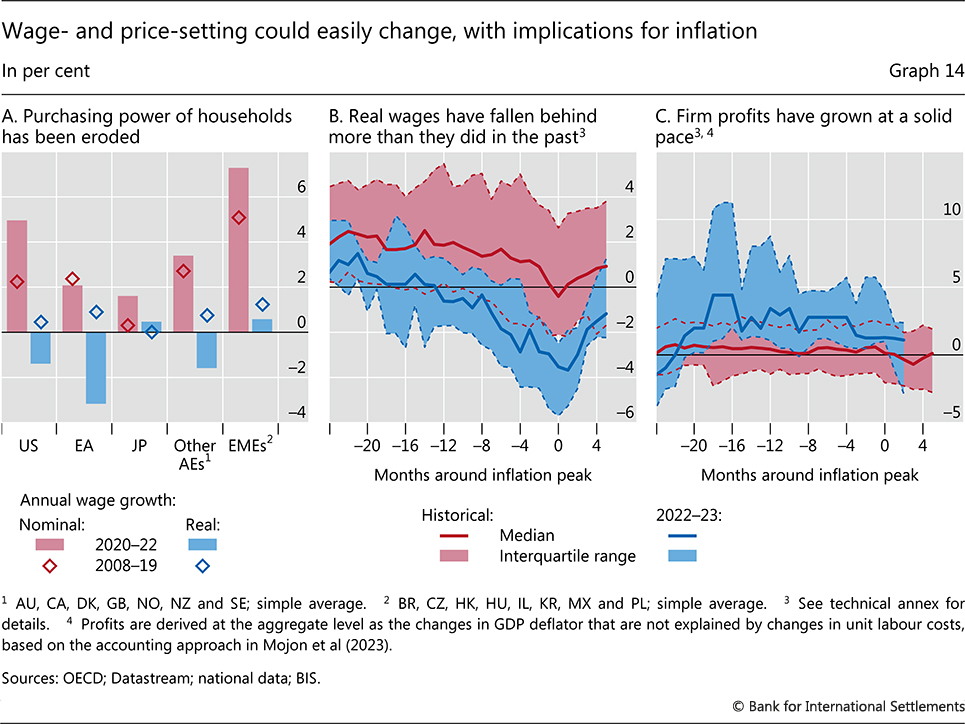

While nominal wage growth has not been exceptionally strong so far, this should not provide too much comfort. Wage adjustments are still influenced by the lingering effects of the norms prevalent in the low-inflation regime, but this could change quickly. The inflation surge has severely eroded the purchasing power of households (Graph 14.A), even more than in past disinflation episodes (Graph 14.B). Some catch-up is on the cards, particularly given the strength of labour markets. While labour’s bargaining power declined significantly over the years of low inflation,10 recent strikes and calls for unionisation suggest that the environment is evolving. In the euro area, for instance, negotiated wage growth has been on the rise and is now at its highest level since the inception of the common currency. And while multi-year wage contracts generally make the adjustment lags for wages considerably longer than for prices, contract length may shorten in response to higher and more persistent inflation.11 What’s more, the pass-through from prices to wages has been somewhat higher when labour markets have been tight.

In parallel, there are signs that price-setting behaviour is changing. Firms are adjusting prices more frequently than when inflation was low and stable.12 In addition, corporate profits, which were already on the rise before the inflation surge, have held up remarkably well so far (Graph 14.C). This is a departure from the historical pattern: in past episodes, profit growth tended to fluctuate within a comparatively narrow range around zero. One concern is that, having been able to raise prices more easily than in the low-inflation regime, firms are now more reluctant to accept profit squeezes and will pass on cost pressures to prices more readily.13

In the end, a shift to a high-inflation regime would require self-sustaining wage-price increases – a “wage-price spiral” – as workers and firms try to recoup their losses. The feedback between wages and prices has been quite low in the last two decades, below 10%. However, moving to a high-inflation regime would strengthen it.14

A stylised exercise based on a decomposition of changes in the GDP deflator during disinflations shows that some catch-up in wages would be compatible with inflation returning to target, but only as long as firms accept a reduction in profits.15 16 Back-of-the-envelope calculations suggest that, for inflation to go back to a target of 2%, profits on average would need to decline by about 2.5% per year in 2023–24, should real wages rise fast enough to make up for the loss in purchasing power and return to the pre-inflation surge level by end-2025. For comparison, the cross-country pre-pandemic median for profit growth has been slightly more than 1.5% between 2014 and 2019.17

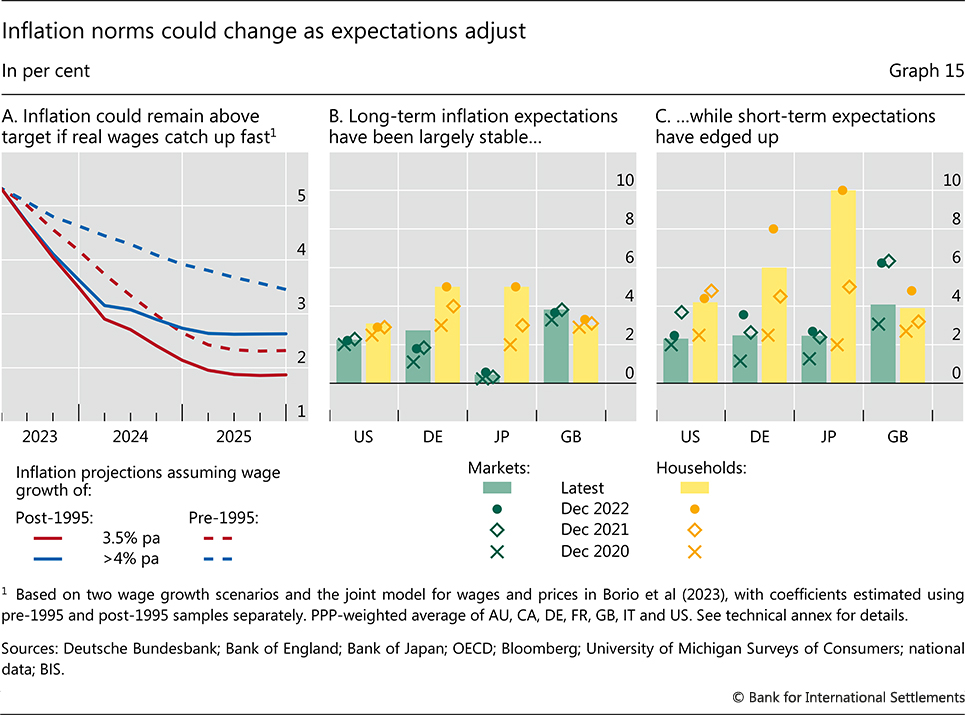

An alternative exercise based on the historical price-wage relationship reinforces the message that the room for adjustment in real wages without jeopardising the inflation target is limited. The exercise is guided by the cointegration between core CPI and hourly compensation and considers the path inflation could take under two different scenarios of purchasing power recovery (Graph 15.A).18 In the first scenario, wages gradually recover, growing at an annual rate of 3.5%, which is consistent with an inflation target of 2% and historical labour productivity growth rate of 1.5% (“gradual catch-up”). Real wages would then largely make up for the losses incurred so far by end-2025. In the second one, the pace of nominal wage growth is faster in 2023 and 2024 at 6%, and settles at 4% by 2025 (“fast catch-up”). In that case, the erosion in real wages is remedied by mid-2024. The gradual catch-up scenario seems conducive to bringing inflation down to or below target (solid red line in Graph 15.A), based on the historical relationship between wages and prices that prevailed in a low-inflation environment – here proxied by post-1995. By contrast, inflation would remain well above target up to the end of 2025 in the fast catch-up scenario (solid blue line in Graph 15.A). Further, if the relationship between wages and prices reverts to the pattern that prevailed before 1995 – capturing a high-inflation environment – the implied inflation trajectory would remain above target also in the gradual catch-up scenario (dashed red line in Graph 15.A). This is because wage-price spillovers were stronger when inflation was higher.

A wage-price spiral would be even more likely should workers and firms seek not just to recoup past losses, but also to be compensated for future ones, ie if expectations became “de-anchored”. While a de-anchoring is not yet evident, inflation expectations have edged up visibly in some cases and are generally above target. True, long-term ones – over a five-year horizon – have remained stable. That said, they are higher than before the inflation surge began. This is especially so for German and Japanese households, who had seen inflation being persistently below target before the pandemic (Graph 15.B). Further, short-term inflation expectations – at the one-year horizon – rose much more than their long-term counterparts (Graph 15.C). The longer inflation remains high, the higher the odds that long-term expectations will follow.

Macro-financial vulnerabilities could complicate the inflation fight

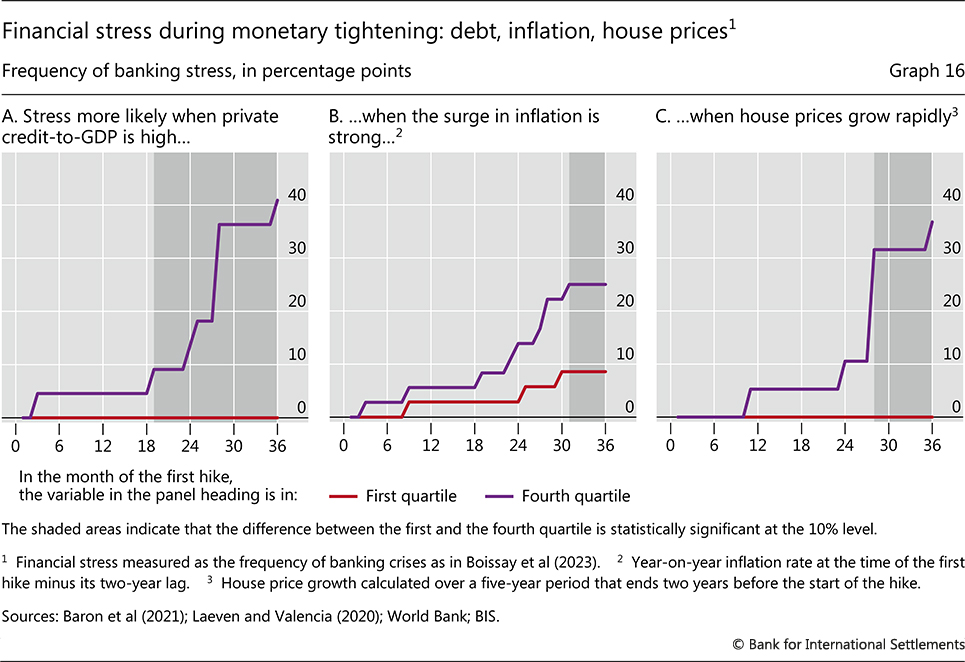

Given the economic background, the risk of further financial stress is material. Historically, about 15% of monetary policy tightening episodes are associated with severe banking stress. The frequency of such stress is higher during tightening episodes that start in an environment of high debt, an abrupt inflation surge or rapid house price growth. If the private debt-to-GDP ratio is in the top quartile of the historical distribution at the time of the first interest rate hike, 40% of the episodes are followed by a banking crisis within three years (Graph 16.A). The odds of a banking crisis are 25% for an inflation surge (Graph 16.B) and about 35% for rapid house price growth (Graph 16.C). Very high debt levels, a remarkable global inflation surge, and the strong pandemic-era increase in house prices19 check all these boxes. Vulnerabilities in the commercial real estate (CRE) sector – historically a common source of stress in the banking sector – raise concerns, too (Box D).

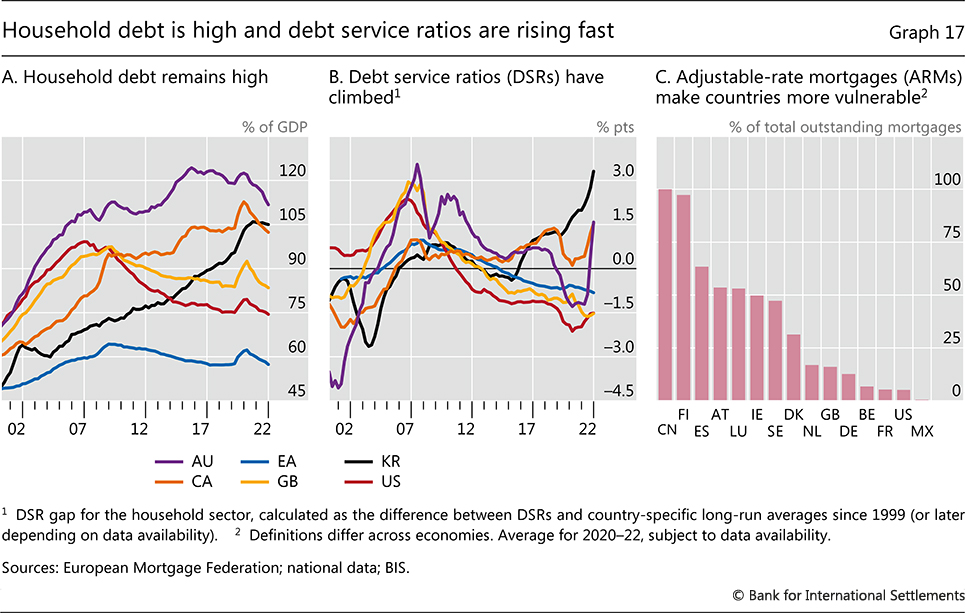

If inflation proves to be more persistent than expected and central banks have to tighten monetary policy by more or for longer, financial stability risks will rise. A key channel is the impact of asset prices and debt burdens on the macroeconomy. Sharply higher mortgage financing costs, coupled with high household debt (Graph 17.A) and falling house prices, translate into lower consumption (see Box D). Evidence shows that, generally speaking, high debt amplifies the impact of monetary tightening20 and that house prices are much more sensitive to a rate hike when debt levels are high.21 Countries with higher household debt have already seen a sharper rise in debt service ratios (DSRs) (Graph 17.B). Economies that rely on adjustable-rate mortgages (ARMs) are especially vulnerable (Graph 17.C).

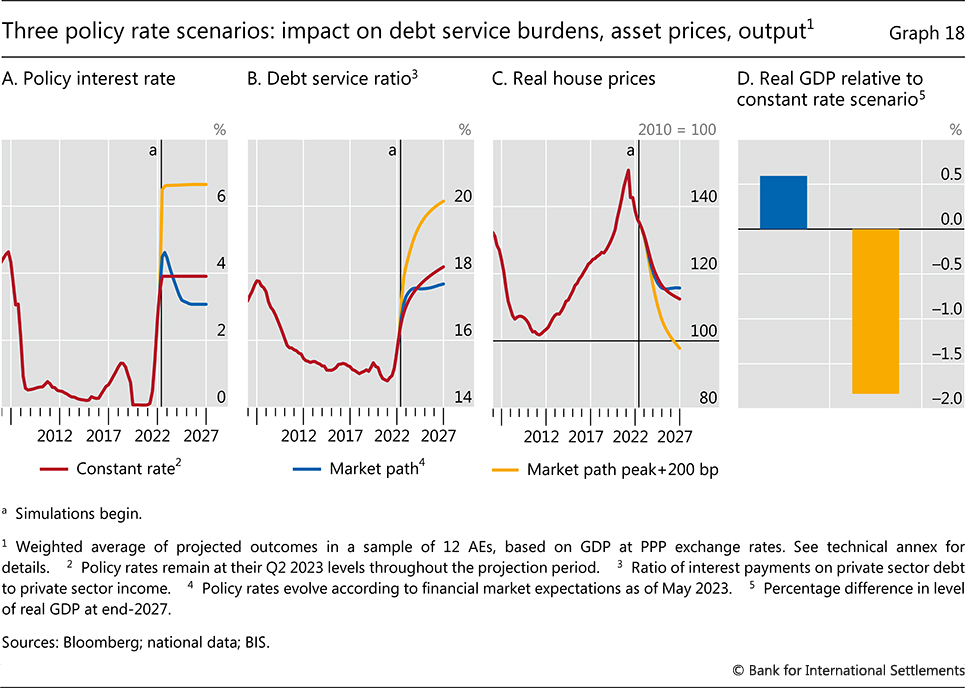

Illustrative simulations, based on historical relationships, shed light on the implications of alternative interest rate paths. For a number of AEs, the simulations trace the behaviour of key variables in three scenarios, assuming that interest rates are constant, follow the “market path” or go “higher-for-longer”, ie remain at the market-implied peak plus 200 basis points until the end of 2027 (Graph 18.A). Average AE private sector DSRs could increase by about 1.5 percentage points and reach their pre-GFC peaks by 2027 if central bank policy rates evolve as financial markets currently expect (Graph 18.B). In the “higher-for-longer” scenario, average DSRs could increase by more than 4 percentage points. The decline in house prices in this adverse scenario could be as large as 30%, relative to the 15% drop in the market-implied path (Graph 18.C). The level of GDP in the adverse scenario could be about 2% lower by end-2027 relative to what would be expected were policy rates to follow the market path (comparing the blue to the yellow bar in Graph 18.D).

Box D

Commercial and residential real estate markets

This box first describes the trends in commercial real estate (CRE) markets, then discusses residential real estate (RRE) developments and concludes with an analysis of risks.

CRE dynamics

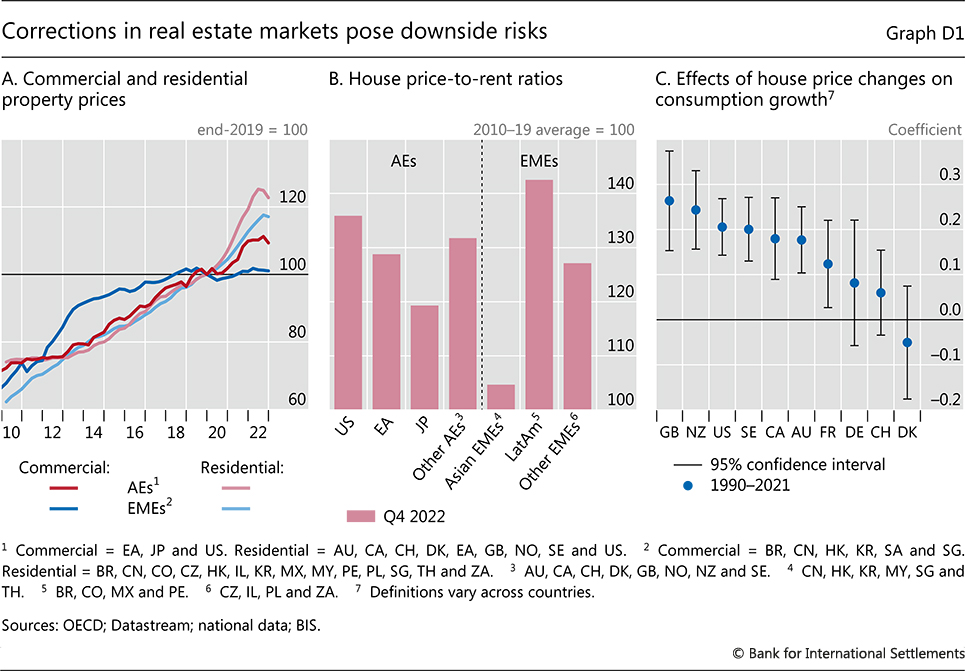

Commercial property markets weakened in emerging market economies (EMEs) during the review period (Graph D1.A). Following a brief period of robust gains, CRE prices in advanced economies (AEs) reached a plateau and dipped slightly. EMEs generally saw the trend of weak CRE prices continue, with sharp price declines in some cases (eg Singapore).

The weakness in commercial property markets reflects a combination of cyclical and structural factors. Higher interest rates played an important role. In addition, office real estate saw sustained pressure as pandemic-era work-from-home activity evolved into permanent remote and hybrid work practices (eg office vacancy rates in the United States stood at almost 20% in the first quarter of 2023, about 6 percentage points higher than in the last quarter of 2019). Retail real estate continued to face headwinds due to greater e-commerce activity.

RRE dynamics

Residential property prices in many economies softened considerably as interest rates climbed. During 2022, many AEs saw house price growth stall or even reverse direction. This weakness persisted into 2023 with only a few exceptions. Markets that had seen particularly strong price increases during the pandemic experienced some of the steepest drops (eg Australia and Canada). House prices also softened in many EMEs, although usually by less than in AEs (Graph D1.A). The gentler softening among EMEs mirrored the generally slower pace of price gains seen during the pandemic.

Valuations are still expensive by historical standards. Price-to-rent ratios have remained at very high levels in most AEs and EMEs (Graph D1.B). This points to further potential price drops.

Risks

The combination of falling house prices, high debt and rapidly rising debt service ratios is likely to increase the number of borrowers facing repayment difficulties for residential mortgages. While delinquency rates on residential mortgages are still low, they are expected to rise in some jurisdictions. For example, in January 2023, the UK Financial Conduct Authority warned that about 9% of UK mortgages are at risk of defaulting in 2023–24.

The downturn in RRE markets has already weighed on activity and a further, disorderly fall in house prices poses a major risk to economic growth. A fall in house prices could weigh on consumption growth due to negative household wealth effects, a reduction of pledgeable collateral and reduced consumer confidence. By some estimates, a 10% decline in house prices reduces (median) consumption growth in the following year by about 1.8% (Graph D1.C). The effect is strongest in countries with high home ownership rates, such as the United Kingdom and New Zealand, and is most pronounced where high home ownership is combined with a heavy reliance on adjustable rate mortgages.

Although smaller than RRE markets, CRE markets also raise a prominent risk to financial stability. Spreads on US commercial mortgage-backed securities (CMBS) rose substantially throughout much of 2022, reflecting a growing difficulty in refinancing maturing debt. In Sweden, where CRE firms rely heavily on bank funding and floating rate loans, a number of large property groups suffered from rating downgrades and stock sell-offs. CRE delinquencies started to pick up in some markets and global distressed CRE debt was close to $175 billion in early 2023, vastly more than in other sectors. CRE prices tend to be more sensitive to the business cycle than RRE prices and to react more strongly to a downturn. Moreover, the performance of banks has historically been sensitive to CRE price developments, raising the risk of a credit crunch. In addition to direct exposures to CRE, particularly in regional banks, some banks have large indirect exposures through other channels, eg via construction lending. Troubles with CRE lending can thus have an outsize impact on overall bank lending. Non-bank financial institutions and foreign investors are also important and growing providers of credit to the CRE sector. Their retrenchment could lead to sizeable asset fire sales, which could in turn destabilise financial markets, as seen during the recent episode of regional bank failures.

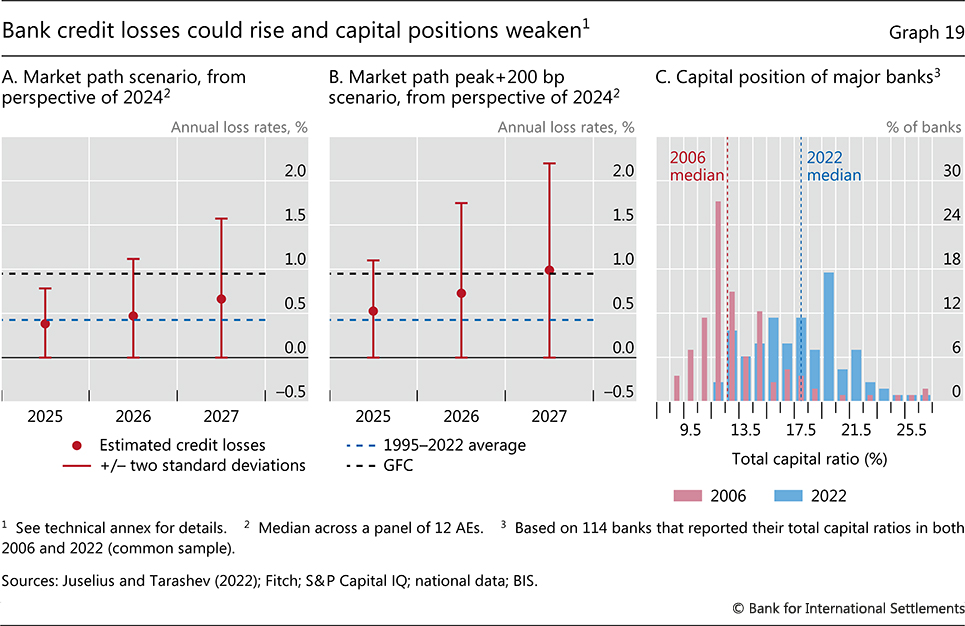

Bank vulnerabilities