Αθήνα 26 Φεβρουαρίου 2024.

Το 1900, περισσότερες από 20.000 τράπεζες λειτουργούσαν στις Ηνωμένες Πολιτείες (σε σύγκριση με λιγότερες από 8.000 σήμερα). Όταν οι άνθρωποι κατέθεταν χρήματα στην τράπεζα, δεν αποθήκευαν απλώς τα μετρητά σε θησαυροφυλάκιο. Η τράπεζα έκανε τα κέρδη της δανείζοντας τα περισσότερα από αυτά τα κεφάλαια σε επιχειρήσεις και ιδιώτες και χρεώνοντας τόκους για αυτά τα δάνεια.

By Pendulum

Οι τραπεζικοί κανονισμοί απαιτούσαν από τις περισσότερες τράπεζες να διατηρούν ένα ορισμένο ποσοστό των καταθέσεών τους, που ονομάζονται re-serves, σε έτοιμα μετρητά ή εύκολα διαθέσιμα.

Οι τράπεζες των μικρών πόλεων κατέθεταν συχνά μερικά από τα αποθεματικά στις μεγαλύτερες τράπεζες για να κερδίσουν τόκους εκεί, αλλά μπορούσαν γρήγορα να ανακαλέσουν τα αποθεματικά τους όπως χρειαζόταν. Οι τράπεζες των πόλεων με τη σειρά τους συνήθως κατέθεταν μέρος των απαιτούμενων αποθεματικών στις μεγαλύτερες τράπεζες της πόλης. Μεγάλο ποσοστό των αποθεματικών που διέρρευσαν σε αυτήν την αλυσίδα τραπεζών κατέληξε στα χρηματοπιστωτικά ιδρύματα της Wall Street της Νέας Υόρκης, στις μεγαλύτερες τράπεζες και σε ομόλογα.

Με αυτόν τον τρόπο, η Wall Street χρηματοδότησε μεγάλο μέρος των αναπτυσσόμενων βιομηχανιών της Αμερικής.

Όταν τα πράγματα κύλησαν ομαλά, τα χρήματα από τα αποθεματικά των τραπεζών διέρρευσαν από την αλυσίδα των τραπεζών στη Wall Street και στη συνέχεια κατέβηκαν στην αλυσίδα με τη μορφή κερδοφόρων τόκων. Τα πράγματα δεν πήγαιναν πάντα ομαλά.

Τραπεζικοί πανικοί

Ένα πρόβλημα ήταν η συχνή έλλειψη χρημάτων σε κυκλοφορία. Για να καλύψουν την αύξηση της ζήτησης για δάνεια, οι τοπικές τράπεζες έπρεπε μερικές φορές να ανακαλούν τα αποθεματικά που είχαν καταθέσει στις τράπεζες των πόλεων. Με τη σειρά τους, αυτές οι τράπεζες έπρεπε συχνά να ανακαλούν τα αποθεματικά τους από την αλυσίδα των τραπεζών. Οι Ηνωμένες Πολιτείες δεν είχαν κεντρική τράπεζα.

Το 1836, ο Πρόεδρος An-Drew Jackson είχε αρνηθεί να εκ νέου την Τράπεζα των Ηνωμένων Πολιτειών. Έτσι, καμία εθνική κεντρική τράπεζα δεν διαχειρίστηκε την προσφορά χρήματος ή λειτούργησε ως «δανειστής έσχατης ανάγκης» για να διατηρήσει τις τράπεζες σε λειτουργία όταν προσωρινά δεν είχαν μετρητά. Επανειλημμένοι τραπεζικοί πανικοί ξέσπασαν μετά τον 19ο αιώνα. Τέτοια γεγονότα συνέβησαν ξαφνικά όταν οι καταθέτες, ενεργώντας με πραγματικούς ή φανταστικούς φόβους, έτρεξαν στις τράπεζές τους για να ζητήσουν πίσω τις καταθέσεις μετρητών τους.

Οι άνθρωποι πανικοβάλονταν εύκολα γιατί, αν η τράπεζά τους αποτύγχανε, θα έχαναν όλα τα χρήματα που είχαν καταθέσει. Σε αντίθεση με σήμερα, κανένα πρόγραμμα κρατικής ασφάλισης δεν εγγυάτο τις τραπεζικές καταθέσεις.

Ένας πανικός θα μπορούσε να ξεκινήσει ανάμεσα στις μικρές αγροτικές τράπεζες και να εξαπλωθεί στην αλυσίδα των τραπεζών. Θα μπορούσε επίσης να υποχωρήσει στην αλυσίδα μετά την αποτυχία των τραπεζών στη Wall Street. Οι χρηματοπιστωτικές αγορές θα μπορούσαν επίσης να προκαλέσουν πανικό στις τράπεζες. Εάν οι τράπεζες κερδοσκοπούσαν απερίσκεπτα τα αποθέματά τους στην ξηρά, όταν η αξία της γης έπεφτε, ακολουούσε πανικός. Εάν η χρηματιστηριακή αγορά καταρρεύσει, θα μπορούσε να προκληθεί τραπεζικός πανικός. Κατά τη διάρκεια του 1800, τουλάχιστον πέντε μεγάλοι τραπεζικοί πανικοί ξέσπασαν ακολουθούμενοι από οικονομική ύφεση ποικίλης διάρκειας και σοβαρότητας. Χωρίς μια κεντρική τράπεζα για να σώσει το τραπεζικό σύστημα κατά τη διάρκεια του πανικού, οι ίδιοι οι τραπεζίτες έπρεπε να προσπαθήσουν να σταματήσουν την οικονομική κατάρρευση.

J.P. Morgan funded the building of the Titanic, and cancelled his long-awaited journey just hours before its proposed departure.

3 of the wealthiest men on earth, whom were against the creation of the Federal Reserve Bank happened to be invited aboard for its maiden voyage. pic.twitter.com/2v2To0PudX

— illuminatibot (@iluminatibot) February 25, 2024

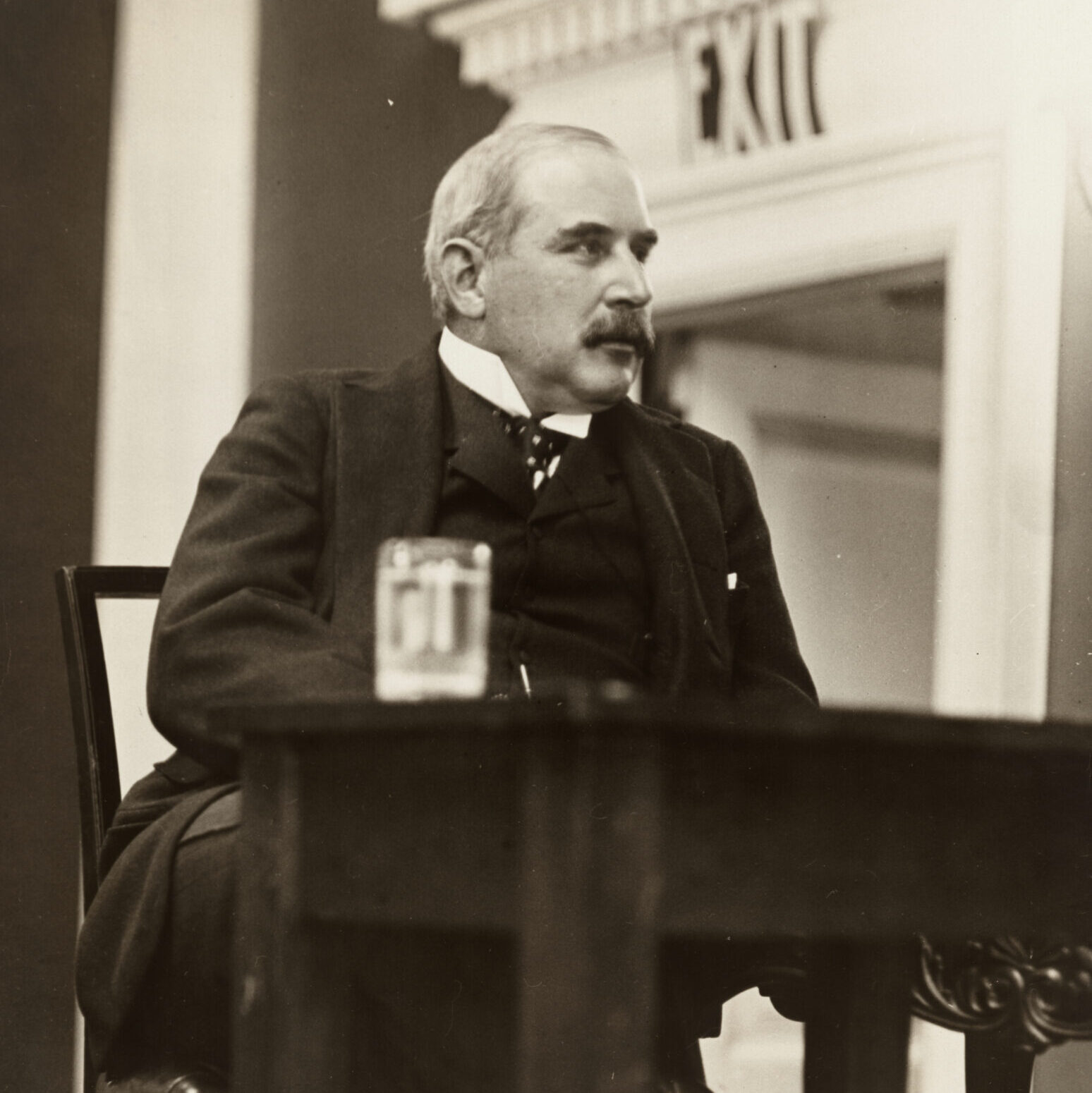

Κανένας τραπεζίτης δεν ήταν καλύτερος από τον J.P. Morgan.

Γεννημένος το 1837, ο John Pierpont Morgan ήταν γιος ενός επιτυχημένου χρηματοδότη τραπεζών. Ο Pierpont, όπως προτιμούσε να τον αποκαλούν, εκπαιδεύτηκε σε ιδιωτικά σχολεία της Νέας Αγγλίας και σπούδασε ιστορία της τέχνης σε ένα γερμανικό πανεπιστήμιο. Αφού πέθανε η πρώτη του γυναίκα, ο Morgan παντρεύτηκε τη Frances Tracy το 1865. Απέκτησαν τέσσερα παιδιά. Σε ηλικία 24 ετών, ο Morgan μπήκε στα χρηματοοικονομικά της Νέας Υόρκης ως πράκτορας της Wall Streetagent για την τραπεζική εταιρεία του πατέρα του. Το 1871, ο πατέρας του Morgan κανόνισε ο γιος του να δημιουργήσει μια εταιρική σχέση με έναν μεγαλύτερο τραπεζίτη.

Οι Drex-ell, Morgan and Co. αναδείχθηκαν σύντομα η κύρια πηγή δανείων προς τη κυβέρνηση των Η.Π.Α. κυβέρνηση.Τις επόμενες δεκαετίες, ο Morgan έγινε η κυρίαρχη φιγούρα στην Wall Library of Congres.

Ήταν πάνω από έξι πόδια ψηλός με μια παραμορφωμένη μοβ μύτη που προκλήθηκε από μια πάθηση του δέρματος. Μισούσε τις φωτογραφίες που τραβήχτηκαν με τη μύτη του στο προφίλ, και κάποτε επιτέθηκε σε φωτογράφους με το μπαστούνι του. Ο Morgan πίστευε ότι ο αμερικανικός καπιταλισμός θα έπρεπε να βρίσκεται υπό τον έλεγχο τραπεζιτών σαν αυτόν.

Οι Wall Streetpeers του τον έβλεπαν ως τον φυσικό τους ηγέτη, ο οποίος ήταν γνωστός ως έντιμος και δίκαιος. Ο Morgan θεώρησε τον άγριο καπιταλισμό στα τέλη του 19ου αιώνα ως σπάταλο και καταστροφικό. Μισούσε τον «καταστροφικό ανταγωνισμό», όπως οι πόλεμοι επιτοκίων που οδήγησαν πολλούς σιδηροδρόμους σε χρεοκοπία.

Ο Morgan πίστευε ότι ο καλύτερος τρόπος για τη δημιουργία επιχειρηματικής σταθερότητας ήταν οι ανταγωνιστές να ρυθμίζουν τον εαυτό τους με ιδιωτικές συμφωνίες που βασίζονται στην εμπιστοσύνη. Στη δεκαετία του 1880, ο Morgan άρχισε να οργανώνει συγχωνεύσεις ανταγωνιστικών σιδηροδρόμων.

Το 1893, ένα κραχ στο χρηματιστήριο προκάλεσε τραπεζικό πανικό και τη χειρότερη ύφεση στην ιστορία των ΗΠΑ μέχρι εκείνη την εποχή. Κατά τη διάρκεια αυτής της ύφεσης, η προσφορά χρήματος συρρικνώθηκε καθώς οι άνθρωποι και οι επιχειρήσεις συσσώρευσαν μετρητά. Το σπάνιο χρήμα προκάλεσε υψηλά επιτόκια δανεισμού, τα οποία οδήγησαν σε πτώση των δαπανών και μαζική ανεργία. Ο κανόνας του χρυσού επιδείνωσε την κρίση. Το Υπουργείο Οικονομικών των ΗΠΑ μπορούσε να τυπώσει μόνο χαρτονομίσματα που υποστηρίζονταν από τα αποθέματά του σε χρυσό.

Η νομισματική κρίση επιδεινώθηκε όταν τα ευρωπαϊκά έθνη ζήτησαν πληρωμή σε χρυσό για να διευθετήσουν τις εμπορικές ανισορροπίες. Αυτό απείλησε να συρρικνώσει περαιτέρω την προσφορά χρήματος.

Τον Φεβρουάριο του 1895, ο Μorgan και άλλοι τραπεζίτες συναντήθηκαν με τον Πρόεδρο Grover Cleveland. Ο Morgan πρότεινε σχέδιο για την οικονομική του εταιρεία να συντονίσει την αγορά χρυσού στις ΗΠΑ από παγκόσμιες πηγές με αντάλλαγμα κρατικά ομόλογα χρυσού πληρωτέα σε 30 χρόνια.

Ο Cleveland ενέκρινε το σχέδιο του Morgan. To σχέδιο λειτούργησε και η προσφορά χρήματος των ΗΠΑ σταθεροποιήθηκε. Ο Morgan και οι άλλοι τραπεζίτες που πραγματοποίησαν το σχέδιο είχαν επίσης καλό κέρδος. Στην πραγματικότητα, ο Morgan έδρασε στη θέση μιας κεντρικής τράπεζας που δεν είχαν οι ΗΠΑ. Η Wall Street του έδωσε το παρατσούκλι «Δίας», από τον κύριο Ρωμαίο θεό. Όταν πέθανε ο τραπεζικός συνεργάτης του, ο Morgan μετονόμασε την εταιρεία J.P. Morgan & Co. Η τράπεζα Morgan χρηματοδότησε τη συγχώνευση πολλών σιδηροδρομικών γραμμών σε έξι τεράστια συστήματα. Αντάλλαξε τη χρηματοδότησή του για την πλειοψηφία των μετοχών στους συγχωνευμένους σιδηροδρόμους και μια θέση στα διοικητικά συμβούλια τους. Η Wall Street αποκάλεσε αυτή τη διαδικασία «morganization». Η Morgan συγχώνευσε επίσης ανταγωνιστικές βιομηχανικές εταιρείες σε γιγαντιαίες εταιρείες.

Το 1901, συγχώνευσε εταιρείες χάλυβα που κατείχε με άλλες εταιρείες Carnegie Steelplusnine για να σχηματίσουν την U.S. Steel. Αυτή έγινε η πρώτη εταιρεία δισεκατομμυρίων δολαρίων στον κόσμο, η οποία ήλεγχε περίπου τη μισή αμερικανική επιχείρηση χάλυβα. Ο Morgan δώρισε εκατομμύρια δολάρια σε μουσεία, την όπερα, τα νοσοκομεία, τα σχολεία και την Επισκοπική Εκκλησία του. Το πάθος του ήταν να συλλέγει έργα τέχνης, χειρόγραφα και άλλα σπάνια αντικείμενα. Για να συγκρατήσει την τεράστια συλλογή του, έχτισε τη βιβλιοθήκη Morgan δίπλα στο σπίτι του.

Ο πανικός του 1907

Το 1901, ο αντιπρόεδρος Theodore Roosevelt έγινε πρόεδρος μετά τη δολοφονία του Προέδρου William McKinley. Ο Roosevelt έδειξε γρήγορα ότι συμπάσχει με τους μεταρρυθμιστές, που ονομάζονταν προοδευτικοί, που απαιτούσαν σθεναρή επιβολή των αντιμονοπωλιακών νόμων. Αλλά το σχέδιο κατέρρευσε και η αξία των αποθεμάτων της εταιρείας έπεσε. Ήταν τότε που ένα νέος είδος “τράπεζας” που ελέγχονταν ελάχιστα έκανε την εμφάνισή του. Οι εταιρείες καταπιστεύματος έκαναν κανονικές τραπεζικές συναλλαγές, αλλά επίσης έδιναν επικίνδυνα δάνεια και κερδοσκοπούσαν στο χρηματιστήριο.

Αναλαμβάνοντας κινδύνους, αποκόμισαν μεγαλύτερα κέρδη και μπορούσαν να προσφέρουν υψηλότερα επιτόκια στους καταθέτες από ό,τι οι πιο κοινές εμπορικές τράπεζες. Επίσης, οι εταιρείες καταπιστεύματος δεν έπρεπε να διατηρούν τόσο αποθεματικό όσο οι εμπορικές τράπεζες. Στις αρχές Οκτωβρίου, οι καταθέτες της Knicker bocker έμαθαν ότι ο πρόεδρος της τράπεζάς τους είχε επενδύσει σε μετοχές United Copper. Αυτό προκάλεσε την καταστροφή της εταιρείας καταπιστεύματος από καταθέτες που φοβήθηκαν ότι είχε χάσει χρήματα και ότι θα αποτύγχανε. Στην πραγματικότητα, η ίδια η Knickerbocker δεν είχε επενδύσει στο πρόγραμμα και ήταν σταθερή. Αλλά η Knickerbocker εξακολουθούσε να μένει χωρίς μετρητά για να εξοφλήσει τους πανικόβλητους καταθέτες της και έκλεισε. Ξεκίνησε ένας πανικός.

Οι καταθέτες σε άλλες τράπεζες εταιρειών εμπιστοσύνης της Νέας Υόρκης άρχισαν να αποσύρουν τα χρήματά τους. Η τραπεζική αλυσίδα Banksdown ανακαλούσαν τα αποθεματικά τους από τη WallStreet για να προφυλαχθούν από το διαρροή των καταθέσεών τους. Οι τραπεζίτες της Wall Street στράφηκαν στον 70χρονο J.P. Morgan, αυτόν που εμπιστεύονταν.

Όταν έλαβε χώρα μια νέα κίνηση στην τράπεζα Τhe Trust Co. of America, ο Morgan και δύο από τους φίλους του τραπεζίτες συγκέντρωσαν 3 εκατομμύρια δολάρια για να το σώσουν. Αλλά οι τραπεζικές εργασίες συνεχίστηκαν, ειδικά στις εταιρείες καταπιστεύματος.

Στη συνέχεια, ο δήμαρχος της Νέας Υόρκης ανέφερε στον Morgan ότι η οικονομικά πιεσμένη πόλη χρειαζόταν ένα δάνειο για να καλύψει τη μισθοδοσία της και να πληρώσει τους εργολάβους.

Φοβούμενοι ότι η οικονομική κατάρρευση της πόλης θα επιδεινώσει τον πανικό, ο Morgan και οι φίλοι του τραπεζίτες αγόρασαν 30 εκατομμύρια δολάρια σε ομόλογα της πόλης. Οι χρηματιστηριακές εταιρείες, που διαχειρίζονταν χρηματιστηριακές συναλλαγές, κινδύνευαν επίσης να αποτύχουν στις υποχρεώσεις τους. Η Morgan συγκέντρωσε μια «δεξαμενή χρημάτων» 25 εκατομμυρίων δολαρίων, σχηματίζοντας δάνεια χαμηλότερου επιτοκίου, αποφεύγοντας σχεδόν βέβαιο κραχ της αγοράς. Αλλά η μεγαλύτερη χρηματιστηριακή εταιρεία στη Wall Street, η Moore & Schley, είχε χρέος 25 εκατομμυρίων δολαρίων. Η χρεοκοπία αυτής της βασικής εταιρείας θα μπορούσε ακόμα να προκαλέσει το κραχ της χρηματιστηριακής αγοράς. Ο Morgan κάλεσε μια συνάντηση στη Βιβλιοθήκη Morgan. Συγκέντρωσε τους τραπεζίτες των εμπορικών εταιρειών και των εταιρειών εμπιστοσύνης της πόλης, τους έβαλε σε χωριστά δωμάτια, κλείδωσε την εξώπορτα και κράτησε το κλειδί στην τσέπη του μέχρι να μπορέσει να διαπραγματευτεί μια συμφωνία.

Η συνάντηση κράτησε μέχρι το βράδυ. Οι τραπεζίτες των εταιρειών καταπιστεύματος αντιστάθηκαν στη συγκέντρωση των αποθεματικών τους για να σταματήσουν τον πανικό, αλλά οι διαπραγματεύσεις συνεχίστηκαν. Στις 4:30 π.μ., ο Morgan τελικά τους παρενόχλησε να υπογράψουν μια συμφωνία. Ζητούσε από τους trust company bankers να διασώσουν τους αδερφούς τους τραπεζίτες που δυσκολευόντουσαν με τρεξίματα στις καταθέσεις τους. Από την πλευρά του, ο Morgan υποσχέθηκε να σώσει τη χρηματιστηριακή εταιρεία Moore & Schley. Στη συνέχεια, ο Morgan επινόησε ένα σχέδιο για τη μείωση του χρέους της Moore & Schley. Θα πουλούσε μια εταιρεία χάλυβα που ανήκε στην U.S. Steel, μια εταιρεία στην οποία μετέχει η Morganheld και ήταν μέλος του διοικητικού συμβουλίου της. Το μόνο πρόβλημα με αυτή τη συμφωνία ήταν ότι αγοράζοντας ανταγωνιστή, η U.S. Steel θα μονοπωλούσε ακόμη περισσότερο τη βιομηχανία χάλυβα.

Αυτό θα μπορούσε να προκαλέσει μια αντιμονοπωλιακή δίωξη από την κυβέρνηση Ρούσβελτ. Ο Μόργκαν έστειλε αμέσως έμπιστους συμβούλους στην Ουάσιγκτον για να πείσουν τον Πρόεδρο Roosevelt να εγκρίνει τη συμφωνία. Ο Roosevelt συμφώνησε ότι οι συνθήκες του πανικού της Wall Street δικαιολογούσαν την αγορά ενός ανταγωνιστή από την US Steel. Η σύναψη συμφωνίας του FalloutMorgan σταμάτησε τελικά τον πανικό της Wall Street. Ωστόσο, η πολυοικονομική ζημιά είχε ήδη εξαπλωθεί σε ολόκληρη τη χώρα.

Η προκύπτουσα ύφεση του 1907-08 ήταν σοβαρή, αλλά πιθανότατα θα ήταν μεγαλύτερη αν συνεχιζόταν ο πανικός στις τράπεζες. Η Wall Street επευφημούσε τον Morgan ως ήρωα. Αλλά οι προοδευτικοί επιτέθηκαν στον Morgan και στη Wall Street για όλα τα κέρδη που αποκόμισαν από τις συμφωνίες τους. Μερικοί μάλιστα τους κατηγόρησαν ότι προκάλεσαν τον πανικό για να μπορέσουν να βγάλουν χρήματα από αυτό, αλλά αυτό δεν αποδείχθηκε ποτέ. Αποδείχθηκε επίσης ότι η χαλυβουργική εταιρεία που αγόρασε η U.S. Steel είχε υποτιμηθεί. Αυτό έκανε την αγορά ακόμη πιο κερδοφόρα για την US Steel (και τoν Morgan). Οι προοδευτικοί επέκριναν τον πρόεδρο βαριά γιατί τον κουκούλωσε ο Morgan για να υπονομεύσει την εκστρατεία κατάρριψης της εμπιστοσύνης του. Επιπλέον, οι προοδευτικοί ισχυρίστηκαν ότι μια «χρηματοπιστία» τραπεζιτών της Wall Street, με επικεφαλής τον Morgan, συνωμότησαν να μονοπωλήσουν τη χρηματοοικονομική επένδυση του έθνους.

Τον Δεκέμβριο του 1912, ο Morgan κατέθεσε ενώπιον μιας ακρόασης της τραπεζικής επιτροπής του Κογκρέσου υπό την προεδρία του αντιπροσώπου Arsene Pujo. Σε ηλικία 75 ετών, ο Μorgan ήταν ημι-συνταξιούχος με τον γιο του, John Jr, στη διαδικασία ανάληψης της οικογενειακής τράπεζας. Όταν ο επικεφαλής σύμβουλος της επιτροπής ρώτησε τον Morgan εάν ασκούσε κάποια εξουσία στην οικονομία, εκείνος απάντησε: «Όχι το παραμικρό».

Αρνήθηκε ότι υπήρχαν χρήματα. Διαφώνησε επίσης ότι οι συγχωνεύσεις του σιδηροδρόμων και βιομηχανιών είχαν δημιουργήσει μια ανθυγιεινή συγκέντρωση οικονομικής δύναμης. Η επιτροπή Pujo, ωστόσο, κατέληξε στο συμπέρασμα ότι υπήρχε μια «κοινότητα συμφερόντων» στη Wall Street που συγκέντρωνε «τον έλεγχο των χρημάτων και της πίστης στα χέρια σχετικά λίγων ανδρών».

Η έκθεση της επιτροπής εντόπισε έξι Wall Streetbanks, συμπεριλαμβανομένης της Morgan’s, γεγονός που καθιστούσε σχεδόν αδύνατο για τις μεγάλες εταιρείες να πουλήσουν τα εταιρικά τους ομόλογα χωρίς τη συνεργασία του ομίλου. Οι έξι τράπεζες είχαν συμφωνήσει να μην ανταγωνίζονται η μία την άλλη για τη διαχείριση νέων εκδόσεων ομολόγων. Η έκθεση Pujo αποκάλυψε επίσης ότι η τράπεζα του Morgan κατείχε δύο ακόμη θέσεις ψήφου στα διοικητικά συμβούλια εταιρειών αξίας 25 δισεκατομμυρίων δολαρίων (μεταξύ 2 και 9 τρισεκατομμυρίων σε σημερινά δολάρια). Ο Morgan ταξίδεψε στην Ευρώπη στις αρχές του 1913. Πέθανε στον ύπνο του στη Ρώμη στις 31 Μαρτίου 1913.

Οι συνεργάτες του Morgan

Το κοινό απέδωσε δημοσίως τον θάνατό του στην πίεση των ακροάσεων του Pujo. Η περιουσία του Morgan αποτιμήθηκε σε περισσότερα από 100 εκατομμύρια δολάρια. Αυτός ο αριθμός ήταν πολύ μικρότερος από τις περιουσίες των βιομηχανικών βαρώνων όπως ο Carnegie και ο Rockefeller. Ο Carnegie σχολίασε: «Και για να σκεφτείς, δεν ήταν πλούσιος».

Ο μοναχογιός του Morgan, John Jr, κληρονόμησε τον έλεγχο της οικονομικής αυτοκρατορίας του πατέρα του.

Μετά τον Πανικό του 1907, υπήρξε ευρέως διαδεδομένη συμφωνία ότι η Κεντρική Τράπεζα ήταν απαραίτητη για τη διαχείριση της προσφοράς χρήματος και ως «δανειστής της τελευταίας ανάγκης».

Έντονη ήταν ωστόσο η διαφωνία, σχετικά με το ποιος θα έπρεπε να διοικεί αυτήν την τράπεζα. Οι περισσότεροι από τους τραπεζίτες της εποχής, συμπεριλαμβανομένης της Morgan, ήθελαν μια ιδιωτική κεντρική τράπεζα ελεγχόμενη εξ ολοκλήρου από τραπεζίτες. Οι προοδευτικοί ήθελαν την κεντρική τράπεζα υπό τον έλεγχο της ομοσπονδιακής κυβέρνησης. Αφού ο Δημοκρατικός Woodrow Wilson κέρδισε τις εκλογές ως πρόεδρος το 1912, τάχθηκε στο πλευρό των προοδευτικών.

Ο Wilson επέμεινε ότι η κεντρική τράπεζα είναι μια δημόσια υπηρεσία που διευθύνεται από κυβερνητικούς αξιωματούχους διορισμένους από τον πρόεδρο. Οι τραπεζίτες και οι Ρεπουμπλικάνοι αντιτάχθηκαν στο αίτημα του Wilson για ομοσπονδιακό έλεγχο της Κεντρικής τράπεζας. Υποστήριξαν ότι η τράπεζα θα ελεγχόταν από πολιτικούς που θα ακολουθούσε τις πολιτικές οποιουδήποτε κόμματος ήταν στην εξουσία. Κατήγγειλαν επίσης ότι ένα τέτοιο συμβούλιο θα σήμαινε σημαντική κρατική παρέμβαση στην ιδιωτική τραπεζική και στο δωρεάν σύστημα επιχειρήσεων.

Οι προοδευτικοί χρησιμοποίησαν τα ευρήματα των ακροάσεων του Pujo για να δικαιολογήσουν την ανάγκη για μια κεντρική τράπεζα που ελέγχεται από την κυβέρνηση για να αντιμετωπίσει την επικίνδυνη συγκέντρωση οικονομικής ισχύος της WallStreet. Για πολλά χρόνια, αγρότες και λαϊκιστές πολιτικοί είχαν παραπονεθεί ότι οι New York banks είχαν υπερβολικό έλεγχο στο κόστος δανεισμού.

Ήταν καιρός, υποστήριξαν οι προοδευτικοί, να σταματήσουν να βασίζονται στους τραπεζίτες της Wall Street, όπως ο J.P. Morgan, για να σταματήσουν οι ίδιοι οι τραπεζικοί πανικοί που αποφέρουν μεγάλα κέρδη στη διαδικασία. Με τους Δημοκρατικούς να ελέγχουν το Κογκρέσο, ο νόμος για την Federal Reserve ψηφίστηκε από ισχυρές πλειοψηφίες στη Βουλή και τη Γερουσία. Ο Πρόεδρος Wilson τον υπέγραψε ως νόμο στις 23 Δεκεμβρίου 1913.

Αυτά ήταν τα βασικά χαρακτηριστικά της πράξης:

• Ένα επταμελές Συμβούλιο Ομοσπονδιακών Αποθεμάτων, που διορίστηκε από τον Πρόεδρο με τη συγκατάθεση της Γερουσίας, επρόκειτο να συντονίσει την πολιτική προσφοράς χρήματος με 12 τράπεζες -αναφέρεται ως Federal Reserve Banks.

Κάθε μία από τις τράπεζες θα βρίσκεται σε διαφορετική περιοχή της χώρας.

• Η Federal Reserve Banks θα ήταν «δανειστές έσχατης ανάγκης» για τις τράπεζες των Η.Π.Α.

• Η Federal Reserve Banks μπορούσε να εκδώσει Federal Reserve Notes, χάρτινο νόμισμα με δυνατότητα επανεξόφλησης σε χρυσό, για να κάνει την προσφορά χρήματος πιο «ελαστική» ή επεκτάσιμη, εάν χρειάζεται.

12 περιφερειακές τράπεζες στους υπεύθυνους χάραξης πολιτικής του Ομοσπονδιακού Αποθεματικού Συστήματος στην Ουάσιγκτον

Ένα σημαντικό ελάττωμα στην προσπάθεια τραπεζικής μεταρρύθμισης του 1913 ήταν η έλλειψη ενός συστήματος ασφάλισης καταθέσεων από τις κυβερνητικές τράπεζες που θα προστατεύει τα χρήματα των ανθρώπων όταν οι τράπεζες πέφτουν.

Το Κογκρέσο ενέκρινε τελικά αυτή τη μεταρρύθμιση το 1933, δημιουργώντας την Federal Deposit Insurance Corporation. Σήμερα, η FDIC ασφαλίζει κάθε καταθέτη έως και τουλάχιστον 250.000 $ σε ασφαλισμένη τράπεζα.

Το 2000, η J.P. Morgan & Co. συγχωνεύθηκε με την Chase Manhattan Corp. για να σχηματίσουν την JPMorgan Chase Bank. Αυτή η τράπεζα συμμετείχε στη διάσωση των τραπεζών των ΗΠΑ το 2008. Δανείστηκε 25 δισεκατομμύρια δολάρια, τα οποία έκτοτε έχει αποπληρώσει στο Υπουργείο Οικονομικών των ΗΠΑ.

Tης Ίδρυσης της FED είχε προηγηθεί μία ενδιαφέρουσα λεπτομέρεια. Η βύθιση του Τιτανικού.

Το υπερωκεάνιο Τιτανικός βυθίστηκε το 1912, η Ομοσπονδιακή Τράπεζα της Αμερικής, η ξακουστή Federal Reserve Bank (FED), άνοιξε τις πύλες της το 1913. Δύο γεγονότα δηλαδή που δεν θα συνδέονταν κατά κανέναν τρόπο μεταξύ τους αν δεν λάχαινε στον Τιτανικό να πάρει στον υγρό του τάφο τρεις προβεβλημένους αμερικανούς επιβάτες με σοβαρή εμπλοκή στη δημιουργία της Κεντρικής Τράπεζας. Αρνητική εμπλοκή, καθώς όλοι τους δεν έβλεπαν με καλό μάτι τη δημιουργία ενός χρηματοπιστωτικού κολοσσού που θα μπορούσε πράγματι να δώσει υπόσταση στη Νέα Τάξη Πραγμάτων και τις σκοτεινές διεργασίες της οικονομικής ελίτ για την υποδούλωση της ανθρωπότητας. Οι τρεις εκατομμυριούχοι που έχασαν τη ζωή τους στο μοιραίο ναυάγιο του Τιτανικού ήταν οι Benjamin Guggenheim, Isador Strauss και John Astor, σφοδροί πολέμιοι της ίδρυσης της FED, η οποία άνοιξε τελικά σε πείσμα τους το 1913. Κάτι που δεν ήταν φυσικά καθόλου τυχαίο, σύμφωνα πάντα με το δημοφιλές σενάριο συνωμοσίας, καθώς όλες οι αντίθετες πλευρές στη δημιουργία της Κεντρικής Τράπεζας είχαν εξαφανιστεί μέχρι τότε από προσώπου γης.

Οι 3 ισχυροί επιβάτες ήταν ιδιαίτερα δραστήριοι και χρησιμοποιούσαν ήδη τις διασυνδέσεις τους στο Κογκρέσο για να μπλοκάρουν τη δημιουργία ενός κολοσσού που όμοιό του δεν είχε ξαναδεί ο σύγχρονος κόσμος. Αυτοί οι τρεις δεν ήταν άλλοι φυσικά από τους βαθύπλουτους Benjamin Guggenheim, Isa Strauss και John Astor, που περιλαμβάνονταν στη λίστα με τους πλουσιότερους ιδιώτες του τότε κόσμου. Την ίδια στιγμή, η ναυπήγηση του Τιτανικού είχε ήδη ξεκινήσει από το 1909 σε ένα ναυπηγείο του Μπέλφαστ της Ιρλανδίας, όταν εντελώς αναπάντεχα ο Τζ. Π. Μόργκαν αγόρασε τη ναυτιλιακή White Star Lines, που ήταν η πλοιοκτήτρια του Τιτανικού…

Οι τρεις ζάμπλουτοι της ιστορίας μας (ο John Jacob Astor ήταν μάλιστα αν όχι ο πλουσιότερος τότε άνθρωπος του κόσμου, σίγουρα στην πρώτη τριάδα) δελεάστηκαν να επιβιβαστούν στον Τιτανικό, καθώς μέχρι τότε η εξασφάλιση μιας VIP καμπίνας είχε γίνει το άγιο δισκοπότηρο της οικονομικής ελίτ. Ακόμα και ο Τζ. Π. Μόργκαν ήταν προγραμματισμένο να είναι στο μοιραίο ταξίδι, αλλά ακύρωσε τελικά (και βολικά) την τελευταία στιγμή.

Ο καπετάνιος του πλοίου Edward Smith ήταν στα σίγουρα ένας από τους πιο έμπειρους θαλασσόλυκους της εποχής, έχοντας ήδη 26 χρόνια πείρας στον Ατλαντικό και τις παγωμένες παγίδες του. Ο Smith δούλευε για τον Morgan.

Ο Smith, γνώστης της τεράστιας περιοχής των παγόβουνων του Βόρειου Ατλαντικού, ταξίδευε σε πλήρη ταχύτητα 22 κόμβων μια νύχτα χωρίς φεγγάρι παρά τους λευκούς παγωμένους όγκους που τον περικύκλωναν. Προφανώς εκτελούσε τις εντολές και μόνο ατύχημα δεν ήταν η πρόσκρουση στο παγόβουνο, καταλήγουν οι συνωμοσιολογικές αναλύσεις. Ένα από τα άλυτα μυστήρια του ναυαγίου παραμένουν οι φωτοβολίδες έκτακτης ανάγκης του πλοίου: όπως είναι γνωστό, μόνο οι κόκκινες ήταν και είναι το διεθνές σήμα κινδύνου, καθώς όλα τα υπόλοιπα χρώματα ήταν απλώς αναγνωριστικά (η πλοιοκτήτρια White Star Line είχε για παράδειγμα το λευκό).

Όταν λοιπόν βυθιζόταν το βαπόρι και το πλήρωμα άρχισε να εκτοξεύει τις φωτοβολίδες SOS, διαπίστωσε έντρομο ότι οι φωτοβολίδες δεν ήταν κόκκινες, αλλά λευκές. Διερχόμενα πλοία είδαν τις λευκές φωτοβολίδες και θεώρησαν φυσικότατα πως δεν ήταν σήμα εκτάκτου ανάγκης, αλλά ότι στο κατάστρωμα γινόταν πάρτι.

Ακόμα και οι σωσίβιες λέμβοι δεν ήταν επαρκείς ούτε και εντελώς γεμάτες όταν άφηναν το καράβι τη μοιραία εκείνη νύχτα της 14ης Απριλίου 1912. Η σύζυγος πάντως του John Jacob Astor γλίτωσε, όπως και πολλοί ακόμα άνθρωποι της μεγαλοαστικής και της μεσαίας τάξης, ακόμα και ιρλανδοί μετανάστες για τον Νέο Κόσμο. Όλα ήταν προσχεδιασμένα λοιπόν για το τρομακτικότερο ναυάγιο που γνώρισε ο 20ός αιώνας;

Έναν χρόνο και 8 μήνες αργότερα, τον Δεκέμβριο του 1913, το αμερικανικό Κογκρέσο υπερψήφιζε το νομοσχέδιο για τη δημιουργία της Ομοσπονδιακής Τράπεζας των ΗΠΑ, καθώς μέχρι τότε κάθε αντίσταση είχε καμφθεί.

Ο Α’ Παγκόσμιος Πόλεμος ξέσπασε σε λιγότερο από έναν χρόνο, υποδεικνύουν με νόημα οι υπέρμαχοι της άποψης ότι αμφότερα τα τραγικά περιστατικά ήταν δείγματα της πρωτόγνωρης πια δύναμης της Νέας Τάξης Πραγμάτων.

Η Κεντρική Τράπεζα χρηματοδότησε εξάλλου τόσο τις ΗΠΑ, όσο και τη Γερμανία και τη Ρωσία στον πόλεμο.

Άλλωστε πως θα μπορούσαν να γνωρίζουν οι εμπνευστές του ναυαγίου ότι οι 3 θα ήταν σίγουρα ανάμεσα στους νεκρούς και όχι τους διασωθέντες; Αυτό το ερώτημα επιδέχεται μίας απάντησης. Οι John Jacob Astor IV, Benjamin Guggenheim και Isador Strauss να ήταν νεκροί (δολοφονημένοι;) πριν την σύγκρουση με το παγόβουν την οποία μοιάζει να επεδίωκε ο καπετάνιος Edward Smith.

Ήταν αρχές Σεπτέμβρη όταν κυκλοφόρησε στη αγορά η πληροφορία ότι ο αμερικάνικος τραπεζικός κολοσσός της JP Morgan ενδιαφερόταν να αποκτήσει συμμετοχή στην ανερχόμενη ελληνική εταιρεία ψηφιακών συναλλαγών Viva Wallet.

Μάλιστα οι ίδιες πληροφορίες ανέφεραν πως η JP Morgan αποτιμούσε τη Viva Wallet πάνω από 1,5 δισ. ευρώ!

Την ίδια ώρα ο ιδρυτής και μεγαλύτερος μέτοχος της Viva Χάρης Καρώνης υποστήριζε σε όποιον τον ρωτούσε ότι δεν πουλάει, καθώς οι προοπτικές της εταιρείας του αξίζουν ακόμη μεγαλύτερης αποτίμησης.

Όλα έμοιαζαν σαν σενάρια επιστημονικής φαντασίας: Ο θείος Σαμ από την Αμερική να ανεμίζει τα δολάρια για μια ελληνική start up και ο επιχειρηματίας να έχει κλείσει τα αυτιά του και να μην ακούει τις «σειρήνες» από την άλλη άκρη του Ατλαντικού.

Και όμως έτσι ακριβώς έγινε. Το χρυσοφόρο deal έκλεισε πριν από τρεις ημέρες έχοντας λίγο -πολύ τα παραπάνω χαρακτηριστικά. Η JP Morgan απέκτησε το 49% της Viva Wallet από τρεις μετόχους μειοψηφίας (το Ηedosophia Fund 25%, το Family Office της Μαριάννας Λάτση 14% και την Deca του Δημήτρη Δασκαλόπουλου 10%). Eπίσης, οι ιδρυτικοί μέτοχοι της Viva Xάρης Καρώνης και Μάκης Αντύπας διατηρούν το πλειοψηφικό πακέτο του 51% και συνεχίζουν να «τρέχουν» την εταιρεία.

Επίσημη πληροφόρηση για την αποτίμηση της συναλλαγής δεν υπάρχει, αλλά όλα συγκλίνουν πως η JP Morgan αποτίμησε μετοχές και (τα λιγοστά) δάνεια στα 2 δισ. ευρώ! Aυτό σημαίνει πως τα τρία funds εισέπραξαν αθροιστικά περίπου 1 δισ. ευρώ, αποκομίζοντας τεράστιες υπεραξίες από την ημέρα που αποφάσισαν να χρηματοδοτήσουν την εταιρεία.

Είναι χαρακτηριστικό ότι η επένδυση της Μαριάννας Λάτση στη Viva Wallet δεν ξεπερνούσε τα 6 εκατ ευρώ και της Deca τα 15 εκατ. ευρώ. Αν επαληθευτούν οι παραπάνω αποτιμήσεις το family office της κυρίας Λάτση εισέπραξε για να αποχωρήσει από τη Viva περίπου 260 εκατ ευρώ και η Deca 190 εκατ ευρώ.

Όσο για τους ιδρυτικούς μετόχους, με την παραπάνω συναλλαγή πιστοποίησαν ότι οι μετοχές που κατέχουν αξίζουν περί το 1 δισ. ευρώ, κάτι που θα αξιοποιηθεί ως σημείο αναφοράς για τις μελλοντικές τους κινήσεις.

Θα πρέπει να σημειωθεί πως η JP Morgan υπέγραψε shareholders agreement με τον Χάρη Καρώνη, που κανείς δεν γνωρίζει τι περιλαμβάνει, αλλά ο λογικός συνειρμός που μπορεί να κάνει κάποιος είναι ότι ο τραπεζικός κολοσσός με κεφαλαιοποίηση 420 δισ. δολάρια δύσκολα θα αρκεστεί να παραμείνει με μειοψηφική συμμετοχή τη Viva Wallet. Ήδη σχεδιάζεται αύξηση κεφαλαίου στη Viva ύψους 200 εκατομμυρίων που θα καλυφθεί εξ΄ ολοκλήρου από την JP Morgan.

To φλερτ της JPMorgan με τη Viva ξεκίνησε από το Λονδίνο, όπου η ελληνική εταιρεία διατηρεί γραφεία. H απόκτηση της Viva Wallet εντάσσεται σε ένα ευρύτερο σχέδιο διείσδυσης των Αμερικανών στην αγορά εταιρειών που παρέχουν ψηφιακές υπηρεσίες (Fintech). Δεν είναι τυχαίο πως η JPMorgan εξαγόρασε πρόσφατα το 75% του τμήματος πληρωμών της γερμανικής αυτοκινητοβιομηχανίας Volkswagen, επεκτείνοντας την πλατφόρμα της για πρώτη φορά στον ευρύτερο τομέα της αυτοκινητοβιομηχανίας.

Ομως, χάρη στο μυαλό και τη διορατικότητα του Χάρη Καρώνη, η Viva Wallet έχει ξεπεράσει το στάδιο της ψηφιακής εταιρείας και έχει περάσει στο στάδιο της neobank. Ιδρύθηκε το 2000 ως εταιρεία πληρωμών και σήμερα, 22 χρόνια μετά, έχει παρoυσία σε 23 χώρες και κατέχει τρεις άδειες, μία τραπεζική -τον Αύγουστο του 2020 εξαγόρασε την Praxia Bank- και δύο άδειες ιδρύματος ηλεκτρονικού χρήματος στην Ελλάδα και την Αγγλία.

Σε καμία περίπτωση τα έσοδά της δεν δικαιολογούν την αποτίμηση των 2 δισ. ευρώ, αλλά οι προοπτικές της έπεισαν (!) τον επικεφαλής της JPMorgan Dimon να αποκτήσει το 49%. Περίπου το 90% των εσόδων της προέρχεται από το εξωτερικό και το 2021 είχε τριπλασιασμό εργασιών σε σχέση με το 2020.

Το μοντέλο ανάπτυξης της Viva Wallet προβλέπει ίδρυση τοπικού υποκατάστηματος σε κάθε χώρα και σύνδεση με το σύστημα πληρωμών της χώρας, εκκαθάριση συναλλαγών στο νόμισμα της κάθε χώρας, σύνδεση με το τοπικό σχήμα πληρωμών και την κάρτα που είναι πιο διαδεδομένη εκεί και παροχή τοπικού IBAN, για να κάνει ο πελάτης όλες τις συναλλαγές του με το τοπικό ΙΒΑΝ ή το τοπικό σχήμα πληρωμών.

Η αποδοχή καρτών δίνει μόνο ένα έσοδο, αλλά η Viva Wallet εξασφαλίζει επιπλέον τζίρο από τη χρήση του λογαριασμού ΙΒΑΝ από την έκδοση καρτών και από την έκδοση δανείων για κεφάλαια κίνησης. Στο εξωτερικό η Viva Wallet αναπτύσσεται με πελάτες αποκλειστικά επιχειρήσεις και μόνο στην Ελλάδα απευθύνεται και σε ιδιώτες καταναλωτές. Το μεγάλο πλεονέκτημα της Viva είναι η καινοτόμα υπηρεσία Tap on Phone, που μετατρέπει τα android κινητά σε τερματικά.

Η δήλωση του επικεφαλής της JP Morgan Paymnents Τάκη Γεωργακόπουλου για τη συναλλαγή δεν αφήνει περιθώρια παρερμηνειών: «Είμαστε πολύ ενθουσιασμένοι που κάνουμε μια στρατηγική επένδυση στη Viva Wallet για να υποστηρίξουμε το όραμά τους να αναπτυχθούν προσφέροντας καινοτομία στις πληρωμές, με στόχο τις ευρωπαϊκές μικρές και μεσαίες επιχειρήσεις (ΜμΕ). Το τοπίο στις πληρωμές είναι κατακερματισμένο στην Ευρώπη αλλά είναι μεγάλο σε όρους ευκαιρίας, με περισσότερους από 17 εκατομμύρια εμπόρους έτοιμους να εφαρμόσουν επεκτάσιμες λύσεις πληρωμών. Αυτός είναι ένας τομέας που θα επικεντρωθεί για πρόσθετη ανάπτυξη η JPMorgan Payments στο μέλλον».

Οταν αποφοίτησε από το 11ο Λύκειο στο Περιστέρι, ο 18χρονος τότε Χάρης Καρώνης ήξερε τι ήθελε να κάνει: να μη γίνει ποτέ υπάλληλος αλλά επιχειρηματίας και να ασχοληθεί με την τεχνολογία. Τα πέτυχε και τα δύο και μάλιστα χωρίς να τελειώσει τις σπουδές του στο ΤΕΙ ηλεκτρολόγων του Πειραιά. Το μυαλό του ξεπερνούσε τα στενά όρια της τριτοβάθμιας τεχνικής εκπαίδευσης.

Στην αρχή τον κέρδισε ο κόσμος του διαδικτύου, αλλά τα πρώτα του λεφτά τα έβγαλε με την εταιρεία Viva Sevices που παρείχε τηλεπικοινωνιακές υπηρεσίες.

Είχε ετήσια έσοδα άνω του 1 εκατ. ευρώ για αρκετά χρόνια, τα οποία ο νεαρός Καρώνης δεν τα έκανε βίλες και σκάφη αλλά τα επένδυσε και με κεφάλαια 20 εκατ. έστησε το 2000 τη Viva Wallet.

Αρχικά δημιουργούσε συστήματα software για τράπεζες, αλλά σύντομα επεκτάθηκε σε συμπληρωματικές υπηρεσίες, όπως ταξιδιωτικές πληρωμές και πληρωμές για θεάματα.

Mέχρι και το 2008 ανέπτυσσε συστήματα ηλεκτρονικών συναλλαγών. Τότε έκανε το colpo grosso. Eκμεταλλευόμενος την ευρωπαϊκή νομοθεσία διεκδίκησε και έλαβε άδεια ιδρύματος πληρωμών. Η δυνατή του ομάδα, με τον ίδιο να συντονίζει, προσφέρει διαρκώς καινοτόμες ιδέες και άφησε πίσω του τις συμβατικές τράπεζες. Δεν είναι υπερβολή να υποστηρίξει κάποιος ότι η Viva Wallet άλλαξε τον τρόπο με τον οποίο πληρώνουν και πληρώνονται οι επιχειρήσεις στην Ευρώπη μέσω της τεχνολογίας αιχμής.

Η συμφωνία προβλέπει και την ενεργοποίηση των stock options για περίπου 200 εργαζομένους της Viva Wallet, που θα λάβουν μια συνολική ανταμοιβή της τάξης των 50 εκατ. δολαρίων σε μετοχές και μετρητά.

Ο Michel de Nostredame αγαπά το ελληνικό ελαιόλαδο και τους καρπούς της ελιάς. Αμφότερα αποτελούν αναπόσπαστη συνταγή του ημερήσιου λιτού διαιτολογίου του ειδικά στη διάρκεια της πρωινής ανάγνωσης των επιλεγμένων ειδήσεων οι οποίες φθάνουν καθημερινά στο γραφείο καθώς ο γραμματέας του κτήματος που είναι επιφορτισμένος με αυτή την αποστολή συμπληρώνει τις σελίδες από τους Τόμους του Χρονολογίου πάντα γραπτώς και με επιμονή στη καλλιγραφία.

Μία από τις οικονομικές ειδήσεις εκείνης της μέρας την οποία επέλεξε ο γραμματέας να παραθέσει ήτο το δημοσίευμα των Financial Times για τις νομικές διαδικασίες κατά του Jamie Dimon από τον κάποτε ιδιοκτήτη της Viva Wallet η οποία πλέον θα μπορούσε να έχει ήδη εξατμισθεί ή να ονομάζεται 0- στο μετασύμπαν.

Στη πραγματικότητα ο Χάρης έχασε τη Viva στα πρώτα 10 λεπτά που κάθησε στο ίδιο τραπέζι με τον Jamie Dimon και τους συνεργάτες του.

Ο ενθουσιώδης και τολμητίας Χάρης γοητεύθηκε στην ιδέα ότι ένας ιστορικός τραπεζικός κολοσσός όπως η JP Morgan, η δόξα του οποίου αναδύεται ακόμη και από τα αμπάρια του Τιτανικού, ασχολήθηκε με τη Viva Wallet.

Έτσι στα πρώτα 10′ της συνάντησης ο Χάρης (Καρώνης) και ο Μάκης (Αντύπας) ξέρασαν το μυστικό της coca-cola. Δηλαδή το τρόπο που λειτουργεί το λογισμικό της Viva Wallet!

Έχοντας ήδη αυτό το μπλιμπλίκι στη κατοχή τους τα στελέχη της JP Morgan θα έπρεπε να επιστρατεύσουν τους καλούς τους τρόπους ώστε να ξεφορτωθούν τους ήδη αχρείαστους νέους συνεταίρους. Ήτο άλλωστε κάτι γνώριμο στους διαδρόμους της Wall Street.

Σε αυτό το σημείο οφείλουμε να σημειώσουμε ότι ο Jamie Dimon (το όνομα του οποίου είχε πέσει πρόσφατα στο τραπέζι ως υποψηφίου των Δημοκρατικών στη θέση του Joe Biden) είναι μία από τις ελάχιστες φωνές του κυρίου Michel de Nostredame όταν ο εκλεκτός Michel θέλει να προκαλέσει οικονομικό τρόμο. Ο Jamie διά μέσω του Jerome Powell της FED λαμβάνει τις σχετικές οδηγίες του Michel de Nostredame.

Όπως αντιλαμβάνεστε το γεγονός ότι ο ο Χάρης και ο Μάκης βρίκονται ακόμη εν ζωή (αλήθεια έχουν λάβει τα εμβόλια ευθανασίας COVID-19 για τις ανάγκες των ταξιδίων της συμφωνίας εν μέσω planδημίας;) διατηρώντας τη ψευδαίσθηση ότι τους ανήκει η Viva Wallet ή οι τραπεζικοί τους λογαριασμοί θα μπορούσε να αποτελεί ένα κωμειδύλλιο σε συνέχειες, τους αναγκαίους στίχους του οποίου θα γράφει ο Πάνος Βλάχος ενώ τα νέα για τις παραστάσεις του κωμειδυλλίου “Viva Wallet” θα μεταφέρει γαργαλιστικά στον σημερινό Έλληνα πρωθυπουργό LGTBQH(amas) KM, ο σύμβουλός του, ο οποίος τυγχάνει και φίλος των Børge Brende και Heiko Echter von der Leyen.

Πάμε τώρα να απολαύσουμε σχετικά πρόσφατα επεισόδια του κωμειδυλλίου>

Μήνυση κατά της JP Morgan (!) κατέθεσε ο Χάρης Καρώνης, ισχυριζόμενος ότι η αμερικάνικη τράπεζα προσπάθησε να μειώσει την αποτίμηση της Viva Wallet, σύμφωνα με τους FT.

Ο κ. Καρώνης, ο οποίος είναι ιδρυτής και συνιδιοκτήτης (!) της Viva Wallet έχει κινήσει (!) νομικές διαδικασίες (Κούγιας;) κατά της JP Morgan καθώς, όπως ισχυρίζεται, η τελευταία επιχείρησε να εμποδίσει την ανάπτυξη της εταιρείας του, στην οποία η αμερικάνικη τράπεζα διατηρεί μεγάλο ποσοστό μετοχών.

Σύμφωνα με νομικά έγγραφα που ήλθαν σε γνώση των FT, ο κ. Καρώνης θεωρεί ότι η JP Morgan βάζει εμπόδια στην είσοδο της Viva Wallet της στις αμερικανικές και νέες ευρωπαϊκές αγορές, σύμφωνα με νομικά έγγραφα που είδαν οι Financial Times.

Ο Καρώνης κατηγορεί επίσης την JPMorgan ότι εμπόδισε τη Viva επιτρέποντας στην επιχείρηση πληρωμών της ίδιας της τράπεζας να την ανταγωνιστεί σε ορισμένες ευρωπαϊκές αγορές-χα, χα, χα-το μυστικό της coca-cola.

Με βάση τη συμφωνία επένδυσης της JPMorgan στη Viva, η αμερικάνικη τράπεζα μπορεί να αναλάβει τον πλήρη έλεγχο του fintech εάν η αξία της Viva είναι κάτω από 5 δισ. ευρώ τον Ιούνιο του 2025. Να σημειωθεί ότι η αμερικάνικη τράπεζα κατέχει μερίδιο 48,5% στη Viva.

Όπως αναφέρει το δημοσίευμα των FT, η JPMorgan έχει προχωρήσει σε ανταγωγή εναντίον του Καρώνη και υποστηρίζει ότι ο τελευταίος επιχειρεί «περιορισμό ή παράκαμψη των συμβατικών και νόμιμων δικαιωμάτων της ως επενδυτή». Και οι δύο νομικές αξιώσεις κατατέθηκαν στο Ανώτατο Δικαστήριο του Λονδίνου (!) την Τετάρτη.

(Σε ποιον ανήκει το Λονδίνο;)

Από την ίδρυσή της το 2000, η Viva έχει σε έναν από τους μεγαλύτερους fintech στη νότια Ευρώπη, προσφέροντας υπηρεσίες πληρωμών σε 24 χώρες. Το 2020 απέκτησε τραπεζική άδεια μετά την εξαγορά της εταιρείας Praxia.

Σύμφωνα με τους FT, η δικαστική διαμάχη μεταξύ της JPMorgan και του Χάρη Καρώνη είναι η τελευταία διαμάχη που έχει ανοιχτή η τράπεζα-χα, χα, χα με ιδρυτή κάποιας από τις επιχειρήσεις που έχει επενδύσει.

Να σημειωθεί ότι Η JPMorgan επένδυσε 1 δισ. ευρώ στη Viva το 2021 για να εξασφαλίσει το 48,5% των μετοχών της ως μέρος μιας πολυδιαφημισμένης ώθησης στην ευρωπαϊκή αγορά πληρωμών.

Στη νομική αγωγή που κατατέθηκε στο Ανώτατο Δικαστήριο, η εταιρεία holding του Καρώνη, WRL, αμφισβήτησε τους όρους που δίνουν τη δυνατότητα να αποκτήσει η JP Morgan την Viva, γιατί όπως λέει δημιουργεί κίνητρα για την τράπεζα να περιορίσει την ανάπτυξή της, ώστε να την εξαγοράσει σε χαμηλότερη τιμή τον επόμενο χρόνο.

Στελέχη της JPMorgan πιστεύουν ότι ο Καρώνης αρνείται να αποδεχθεί ότι η αποτίμηση των εταιρειών fintech έχουν υποχωρήσει δραστικά τα τελευταία δύο χρόνια λόγω των υψηλότερων επιτοκίων.

Όταν η JPMorgan συμφώνησε να επενδύσει στη Viva, ο διευθύνων σύμβουλος Jamie Dimon – ο παππούς του οποίου μετανάστευσε στις ΗΠΑ από την Ελλάδα – ταξίδεψε στην Αθήνα για να συναντήσει τον Καρώνη καθώς και τον πρωθυπουργό LGTBQH(amas) KM.

Στην ημέρα επενδυτών της τράπεζας το 2022, ο Dimon επαίνεσε τον παγκόσμιο επικεφαλής πληρωμών της JPMorgan Τάκη Γεωργακόπουλο για την επίτευξη της συμφωνίας Viva.

Έκτοτε, οι σχέσεις μεταξύ της JPMorgan και του Καρώνη, ο οποίος εξακολουθεί να είναι διευθύνων σύμβουλος της Viva, έχουν επιδεινωθεί.

Προς τα τέλη του περασμένου έτους, δύο διευθυντές που διορίστηκαν από την JPMorgan στο διοικητικό συμβούλιο της Viva παραιτήθηκαν μετά από διαφωνίες για την ανεξαρτησία τους, ανέφεραν οι άνθρωποι που ενημερώθηκαν για την κατάσταση.

Οι δύο πλευρές έχουν επίσης διαφωνήσει σχετικά με τον τρόπο με τον οποίο αποτιμάται η Viva. Η JPMorgan προσέλαβει την Houlihan Lokey, η οποία πρόσφατα έδωσε στο fintech αποτίμηση 1 δισ. ευρώ. Ο εκτιμητής της Viva, η EY, την αποτίμησε στα 3 δισ. ευρώ.

Η JPMorgan και η WRL έχουν φτάσει σε αδιέξοδο σχετικά με τον τρόπο αποτίμησης της Viva και ζητούν από το Ανώτατο Δικαστήριο να επιλύσει τη διαφορά.

«Αυτή η αγωγή υποβλήθηκε αφού εξαντλήθηκαν όλες οι άλλες επιλογές», δήλωσε η JPMorgan σε μια δήλωση σχετικά με την αξίωσή της κατά της WRL.

«Παρά αυτή τη διαμάχη, πιστεύουμε στη Viva Wallet, στους ανθρώπους της, στη στρατηγική μας επένδυση στην εταιρεία και στην ευρύτερη επιχείρησή μας στην Ελλάδα».

Τι είχε προηγηθεί>

Oι ανατροπές διαδέχονται η μία την άλλη.

Με αυτή την εισαγωγή ας δούμε κάτι ενδιαφέρον.

To Koυρδιστό Πορτοκάλι έχοντας πρωταγωνιστικό ρόλο στις εξελίξεις (Leading in a disruptive world) επεσήμανε πολύ έγκαιρα ότι σε ένα κόσμο χωρίς σταθερά και με διαρκείς ανατροπές κανείς δεν μπορεί να θεωρείται με ασφάλεια “μεγάλος”.

Μάλιστα με αφορμή την εξαγορά της Viva Wallet από την JP Morgan είχαμε εντοπίσει κάποιες ενδιαφέρουσες “λεπτομέρειες” οι οποίες προφανώς και δεν πέρασαν απαρατήρητες από τον επικεφαλής της Viva Wallet Χάρη Καρώνη με αποτέλεσμα οι άνθρωποι να έχουν δεύτερες σκέψεις για τη περίφημη συμφωνία με την JP Morgan.

Για να δούμε τι έγραφε στις 11 Νοεμβρίου 2022 στο Capital.gr η Βάσω Αγγελέτου υπό τον τίτλο Μαύρα σύννεφα στο mega deal Viva – JP Morgan.

Με “ναυάγιο” απειλείται η πολύκροτη συμφωνία εκτιμώμενου ύψους 1 δισ. δολαρίων μεταξύ της Viva Wallet και της JP Morgan που είχε προκαλέσει κυριολεκτικά “φρενίτιδα” όταν ανακοινώθηκε στις αρχές του έτους.

Πηγές με γνώση των διαδικασιών αναφέρουν στο Capital.gr ότι το ιδρυτικό δίδυμο Χάρης Καρώνης – Μάκης Αντύπας που ελέγχει το 51,5% της Viva έχει αλλάξει στάση απέναντι στον τραπεζικό κολοσσό, προβάλλοντας πρόσθετες οικονομικές αξιώσεις για την ολοκλήρωση της συμφωνίας.

Επιδίωξη του πλειοψηφικού μετόχου είναι, σύμφωνα με τις ίδιες πληροφορίες, να επαναδιαπραγματευτεί το τίμημα της συναλλαγής, κρίνοντας ότι η αξία του “πρώτου μονόκερου” της χώρας έχει αυξηθεί τους μήνες που μεσολάβησαν.

Σύμφωνα με ασφαλείς πληροφορίες του Capital.gr, υπάρχει σε εξέλιξη μια συζήτηση για τα μελλοντικά δικαιώματα εξαγοράς που έχουν συμπεριληφθεί στο Shareholders Agreement κατ΄ επιθυμία της JP Morgan. Η εν λόγω συζήτηση διεξάγεται μεταξύ του πλειοψηφικού μετόχου και του αγοραστή και δεν περιλαμβάνει τους υπόλοιπους μετόχους.

Σύμφωνα με ασφαλείς πληροφορίες, πάντως, το κλίμα που έχει διαμορφωθεί εντός της neobank σε τίποτα δεν θυμίζει τους πανηγυρισμούς που είχαν διαδεχθεί τη δημοσιοποίηση της συμφωνίας μεταξύ των δύο εταιρειών. Θυμίζεται ότι το deal έλαβε τεράστιες διαστάσεις δημοσιότητας και επικροτήθηκε από αξιωματούχους της κυβέρνησης ως ένα από τα μεγαλύτερα επενδυτικά “success story” των τελευταίων ετών.

Πηγές με γνώση της κατάστασης κάνουν λόγο για “πολεμικό κλίμα” που έχει δημιουργηθεί στο εσωτερικό της Viva, με στόχο τον διευθύνοντα σύμβουλο Χάρη Καρώνη και τις νέες αξιώσεις που προβάλλει στον ενδιαφερόμενο αγοραστή.

Μεγάλη μερίδα του διοικητικού πυρήνα φαίνεται να κατηγορεί τον CEO ότι ρισκάρει να “τινάξει τη συμφωνία στον αέρα”. Θυμίζεται ότι η συμφωνία προβλέπει την επιβράβευση 200 στελεχών της Viva με stock options αξίας από 50.000 έως 4 εκατ. ευρώ – γεγονός που συνεπάγεται ότι μια ενδεχόμενη ματαίωσή της θα προκαλούσε μεγάλη απογοήτευση στα ωφελούμενα στελέχη.

Ανάλογα συναισθήματα θα βιώσουν, σε ένα τέτοιο ενδεχόμενο, και οι μειοψηφικοί μέτοχοι -το LATSCO family office με ποσοστό 13%, η DECA με 10% και το fund Hedosophia με 24%-, οι οποίοι έχουν προεξοφλήσει ένα cash out της επένδυσής τους έναντι δεκάδων εκατομμυρίων ευρώ, καταγράφοντας αποδόσεις που πολλοί επενδυτές θα ζήλευαν διεθνώς.

Πάντως, για την ολοκλήρωση του mega deal, το οποίο έχει λάβει εδώ και εβδομάδες το “πράσινο φως” της Τράπεζας της Ελλάδος και του SSM, υπάρχει προκαθορισμένη προθεσμία η οποία εκπνέει στα τέλη Νοεμβρίου. Αυτό σημαίνει ότι είναι ζήτημα λίγων εβδομάδων για να ενημερώσει η Viva Wallet την Τράπεζα της Ελλάδος σχετικά με την επιτυχή ή μη ολοκλήρωση της συμφωνίας εξαγοράς – ό,τι αυτό συνεπάγεται για τη φήμη της εταιρείας εντός και εκτός συνόρων.

Αυτά γράφει λοιπόν το Capital.

Ο Μάκης και ο Χάρης έχοντας ανάμεσά τους τον Jamie Dimon. Tώρα αναζητούν το πορτοφόλι τους (είναι πορτοφολάς ο Jamie;) με την αίσθηση ότι δεν τους ανήκει τίποτε και είναι δυστυχείς. Λάθος. Κατέχουν πλέον τη γνώση.

Πάμε να δούμε ένα ρεπορτάζ του Κουρδιστού Πορτοκαλιού όταν είχε ανακοινωθεί η περίφημη συμφωνία>

“Αν έχετε μια λαμπρή ιδέα, πάρτε με ένα τηλέφωνο. Ακόμη και μια ανταγωνιστική επενδυτική τράπεζα μπορεί να μας φέρει μια καλή ιδέα και θα πάρει την προμήθεια της”

Ο ίδιος είχε κάνει ξεκάθαρη εδώ και χρόνια την στρατηγική του: Ο μόνος τρόπος για να καταφέρει ο αμερικανικός τραπεζικός κολοσσός να αντιμετωπίσει τον αυξανόμενο ανταγωνισμό από τις fintech εταιρείες που γιγαντώνονται συνεχώς είναι οι επενδύσεις σε εταιρείες που αναπτύσσουν καινοτόμες τεχνολογίες ειδικά στο χώρο των ηλεκτρονικών πληρωμών και των επενδυτικών υπηρεσιών.

Εδώ λοιπόν θα μπορούσε να υπάρχει και μία άλλη ανάγνωση. Οι κάποτε Γολιάθ σπεύδουν να εξαγοράσουν τους απειλητικούς ψηφιακούς Δαυίδ πριν την διαφαινόμενη ήττα, η οποία θα μπορούσε να εξελιχθεί σε ήττα του “παλαιού κόσμου” από έναν “νέο” και “ανεξέλεγκτο” ψηφιακό κόσμο που έρχεται με φόρα και χωρίς τανκς να αμφισβητήσει τις δομές αιώνων της παγκόσμιας οικονομίας.

Ζούμε τον ερχομό του νέου και τις οδύνες του παλαιού;

Όλο και πιο συχνά οι κεντρικοί τραπεζίτες που βρίσκονται κάτω από τη σκέπη της Basel Committee-Bank for International Settlements επισημαίνουν την “ανάγκη να δείξουμε τη δέσμευσή μας στην παγκόσμια συνεργασία και στην ενίσχυση της ανθεκτικότητας των τραπεζών μας…”

Ο δε Πρόεδρος της Επιτροπής της Βασιλείας Pablo Hernández de Cos υπογράμμισε πρόσφατα τη σημασία να εφαρμοστεί με συνέπεια και χωρίς καθυστερήσεις Το πλαίσιο της Βασιλείας III που οριστικοποιήθηκε το 2017 και εγκρίθηκε από τους ηγέτες της G20. Σε κάθε του γραμμή της πρόσφατης ομιλίας του με θέμα την τραπεζική μεταρρύθμιση της ΕΕ μπορεί κανείς να διακρίνει το επίπεδο συναγερμού να κλιμακώνεται.

Implementing Basel III

Remarks by Pablo Hernández de Cos, Chair of the Basel Committee on Banking Supervision and Governor of the Bank of Spain, at the European Economic and Social Committee public hearing on “The EU banking reform package”, 8 February 2022.

Καλησπέρα και σας ευχαριστώ που με προσκαλέσατε να συμμετάσχω σε αυτή τη δημόσια ακρόαση σχετικά με τη δέσμη μέτρων για την τραπεζική μεταρρύθμιση της ΕΕ.

Θα εστιάσω τις παρατηρήσεις μου σήμερα στην εφαρμογή των εκκρεμών μεταρρυθμίσεων της Βασιλείας ΙΙΙ.

Θα κάνω πρώτα κάποιες σκέψεις με την ιδιότητά μου ως Chair of the Basel Committee και στη συνέχεια θα κάνω ορισμένες συγκεκριμένες παρατηρήσεις σχετικά με την κατάσταση στην Ευρώπη υπό την ιδιότητά μου ως Διοικητής της Τράπεζας της Ισπανίας.

Ως σύντομη επισκόπηση, η Basel Committee είναι ο κύριος παγκόσμιος ρυθμιστής προτύπων για την προληπτική ρύθμιση των τραπεζών και παρέχει ένα forum συνεργασίας σε θέματα τραπεζικής εποπτείας. Η εντολή της είναι να ενισχύσει τη ρύθμιση, την εποπτεία και τις πρακτικές των τραπεζών παγκοσμίως με σκοπό την ενίσχυση της παγκόσμιας χρηματοπιστωτικής σταθερότητας. Κατά τη συνέχιση των εργασιών της, η Επιτροπή βασίζεται σε αυστηρή εμπειρική ανάλυση, συμπεριλαμβανομένου ενός ολοκληρωμένου προγράμματος εργασίας αξιολόγησης. Μια τέτοια προσέγγιση βοηθά να διασφαλιστεί ότι η προσέγγιση της επιτροπής στηρίζεται όσο το δυνατόν περισσότερο σε αμερόληπτα στοιχεία.

Η χρηματοπιστωτική σταθερότητα είναι παγκόσμιο δημόσιο αγαθό. Οι διασυνοριακές διαρροές χρηματοπιστωτικών δυσχερειών μπορεί να οδηγήσουν σε ανεπαρκείς επενδύσεις στη χρηματοπιστωτική σταθερότητα από μεμονωμένες δικαιοδοσίες και περιφέρειες.

Δεδομένης της παγκόσμιας φύσης του χρηματοπιστωτικού συστήματος, η αγωνία σε μια δικαιοδοσία ή περιοχή μπορεί εύκολα να μεταδοθεί σε άλλα μέρη του πλανήτη.

Έχουμε δει πολλά παραδείγματα τέτοιων διασυνοριακών επιπτώσεων σε προηγούμενες χρηματοπιστωτικές κρίσεις. Επομένως, ένα ανοιχτό παγκόσμιο χρηματοπιστωτικό σύστημα απαιτεί ένα σύνολο παγκόσμιων ελάχιστων και συνεπών προτύπων προληπτικής εποπτείας. Στον διασυνδεδεμένο κόσμο μας, μια αποτυχία να το επιτύχουμε αυτό θα μπορούσε να οδηγήσει σε κατακερματισμό των ρυθμιστικών αρχών, ρυθμιστικό αρμπιτράζ, άνισους όρους ανταγωνισμού για τις διεθνώς ενεργές τράπεζες και αυξημένους κινδύνους για την παγκόσμια χρηματοπιστωτική σταθερότητα.

Από την ίδρυσή της το 1974, τα μέλη της Επιτροπής της Βασιλείας έχουν επιδείξει την ισχυρή τους δέσμευση για συνεργασία σε θέματα παγκόσμιας χρηματοπιστωτικής σταθερότητας, μεταξύ άλλων μέσω της ανάπτυξης ενός παγκόσμιου ρυθμιστικού πλαισίου για τράπεζες που δραστηριοποιούνται διεθνώς. Η τελευταία έκδοση αυτού του πλαισίου, γνωστή ως Βασιλεία ΙΙΙ, επιδιώκει να αντιμετωπίσει τις ελλείψεις στο τραπεζικό σύστημα που εκτέθηκαν από τη Μεγάλη Χρηματοπιστωτική Κρίση (GFC). Το πλαίσιο της Βασιλείας III οριστικοποιήθηκε το 2017 και εγκρίθηκε από τους ηγέτες της G20.

Ξεκινώντας από την άποψή μου ως Προέδρου της Επιτροπής, θα ήθελα να σταθώ σε τρία σημεία.

Πρώτον, νομίζω ότι είναι χρήσιμο να υπενθυμίσουμε το σκεπτικό αυτών των μεταρρυθμίσεων και γιατί παραμένουν τόσο σημαντικές σήμερα όσο ήταν όταν οριστικοποιήθηκαν το 2017.

Ενώ πολλά έχουν αλλάξει από το 2017, η πανδημία του Covid-19 και άλλες διαρθρωτικές τάσεις υπογράμμισαν ακόμη περισσότερο τη σημασία ενός ανθεκτικού τραπεζικού συστήματος. Οι μεταρρυθμίσεις της Βασιλείας ΙΙΙ έπαιξαν κεντρικό ρόλο στο να διασφαλιστεί ότι το τραπεζικό σύστημα παρέμεινε λειτουργικά και οικονομικά ανθεκτικό κατά τη διάρκεια της πανδημίας.

Σε αντίθεση με την εμπειρία του GFC, οι τράπεζες μπόρεσαν να συνεχίσουν να υποστηρίζουν την πραγματική οικονομία. Οι πελάτες των τραπεζών, είτε είναι καταθέτες, δανειολήπτες ή χρήστες άλλων τραπεζικών υπηρεσιών, έχουν ωφεληθεί πολύ από την ανθεκτικότητα του τραπεζικού συστήματος και θα συνεχίσουν να το κάνουν. Θα πρέπει επίσης να αναγνωρίσουμε ότι τα μέτρα δημόσιας στήριξης έχουν υποστηρίξει σε μεγάλο βαθμό τις τράπεζες από τις ζημίες μέχρι σήμερα. Επομένως, δεν πρέπει να εφησυχάζουμε για την ανάγκη εφαρμογής των εκκρεμών μεταρρυθμίσεων της Βασιλείας ΙΙΙ.

Ενώ το αρχικό σύνολο μεταρρυθμίσεων της Βασιλείας ΙΙΙ διόρθωσε έναν αριθμό σφαλμάτων στο ρυθμιστικό πλαίσιο πριν από την GFC, ο τρόπος με τον οποίο οι τράπεζες υπολόγιζαν τα σταθμισμένα περιουσιακά στοιχεία (RWA) – τον παρονομαστή των σταθμισμένων αναλογιών κεφαλαίου των τραπεζών – παρέμεινε σε μεγάλο βαθμό αμετάβλητος . Ωστόσο, ο GFC κατέδειξε οδυνηρά τον υπερβολικό βαθμό μεταβλητότητας στις κεφαλαιακές απαιτήσεις των τραπεζών που έχουν διαμορφωθεί ως μοντέλο. Για παράδειγμα, όταν ζητήθηκε από τις τράπεζες να διαμορφώσουν τις κεφαλαιακές απαιτήσεις πιστωτικού κινδύνου για το ίδιο υποθετικό χαρτοφυλάκιο, οι αναφερόμενοι δείκτες κεφαλαίου κυμαίνονταν έως και 400 μονάδες βάσης.

Παρόμοια ανησυχητικά επίπεδα μεταβλητότητας θα μπορούσαν επίσης να παρατηρηθούν σε άλλες κατηγορίες κινδύνων μοντελοποιημένων, συμπεριλαμβανομένου του πιστωτικού κινδύνου αγοράς και του πιστωτικού κινδύνου αντισυμβαλλομένου.

Και η GFC τόνισε τις ελλείψεις στο πλαίσιο λειτουργικού κινδύνου, όπου οι κεφαλαιακές απαιτήσεις των τραπεζών που διαμορφώθηκαν σε μοντέλα δεν ήταν επαρκώς εύρωστες για να καλύψουν ζημίες που προέρχονται από κακή συμπεριφορά και ανεπαρκή συστήματα και ελέγχους.

Αυτός ο υπερβολικός βαθμός μεταβλητότητας RWA απείλησε την αξιοπιστία των αναφερόμενων δεικτών κεφαλαίου των τραπεζών. Στην κορύφωση του GFC, οι επενδυτές έχασαν την πίστη τους στους δημοσιευμένους δείκτες των τραπεζών και έδωσαν μεγαλύτερη βαρύτητα σε άλλους δείκτες φερεγγυότητας των τραπεζών.

Οι εκκρεμείς μεταρρυθμίσεις της Βασιλείας ΙΙΙ επιδιώκουν να βοηθήσουν στην αποκατάσταση της αξιοπιστίας στον υπολογισμό του RWA των τραπεζών με τέσσερις τρόπους:

Πρώτον, θα ενισχύσουν την ευρωστία και την ευαισθησία κινδύνου των τυποποιημένων προσεγγίσεων για τον πιστωτικό κίνδυνο, τον κίνδυνο αγοράς και τον λειτουργικό κίνδυνο, γεγονός που θα διευκολύνει τη συγκρισιμότητα των δεικτών κεφαλαίου των τραπεζών.

Δεύτερον, θα περιορίσουν τη χρήση εσωτερικά μοντελοποιημένων προσεγγίσεων διασφαλίζοντας ότι οι μοντελοποιημένες παράμετροι υπόκεινται σε μεγαλύτερες διασφαλίσεις και ότι οι προηγμένες προσεγγίσεις μοντελοποίησης δεν χρησιμοποιούνται για χαρτοφυλάκια με περιορισμένα ιστορικά δεδομένα.

Τρίτον, οι μεταρρυθμίσεις της Βασιλείας ΙΙΙ θα εισαγάγουν ένα ισχυρό επίπεδο παραγωγής ευαίσθητο στον κίνδυνο. Το κατώτατο όριο παραγωγής παρέχει ένα backstop με βάση τον κίνδυνο που περιορίζει τον βαθμό στον οποίο οι τράπεζες μπορούν να μειώσουν τις κεφαλαιακές απαιτήσεις τους σε σχέση με τις τυποποιημένες προσεγγίσεις.

Αυτό βοηθά στη διατήρηση ίσων όρων ανταγωνισμού μεταξύ των τραπεζών που χρησιμοποιούν εσωτερικά μοντέλα και εκείνων των τυποποιημένων προσεγγίσεων. Υποστηρίζει επίσης την αξιοπιστία και τη συγκρισιμότητα των σταθμισμένων υπολογισμών των τραπεζών χάρη στις συνοδευτικές απαιτήσεις δημόσιας γνωστοποίησης, καθώς οι τράπεζες θα πρέπει να δημοσιεύουν το συνολικό RWA τους που αποτελεί τον παρονομαστή των σταθμισμένων κεφαλαιακών απαιτήσεών τους, συμπεριλαμβανομένης της προσαρμογής κατώτατου ορίου παραγωγής .

Και τέταρτον, οι μεταρρυθμίσεις θα συμπληρώσουν το σταθμισμένο ως προς τον κίνδυνο πλαίσιο με έναν οριστικό δείκτη μόχλευσης. Ο δείκτης μόχλευσης παρέχει προστασία έναντι μη βιώσιμων επιπέδων μόχλευσης και μετριάζει τον κίνδυνο παιχνιδιών και μοντέλων τόσο σε εσωτερικά μοντέλα όσο και σε τυποποιημένες προσεγγίσεις μέτρησης κινδύνου.

Η βαρύτητα των ρυθμιστικών σφαλμάτων που επιδιώκει να αντιμετωπίσει η Βασιλεία III παραμένει τόσο σημαντική σήμερα όσο και πριν από την πανδημία. Για παράδειγμα, μια πρόσφατη έκθεση της Ευρωπαϊκής Αρχής Τραπεζών σχετικά με τις κεφαλαιακές απαιτήσεις των τραπεζών που έχουν διαμορφωθεί με μοντέλα υποδεικνύει ένα «σημαντικό» επίπεδο διασποράς κεφαλαίων «που πρέπει να παρακολουθείται». Επομένως, είναι σημαντικό όλες οι δικαιοδοσίες της Επιτροπής της Βασιλείας να εφαρμόσουν τις μεταρρυθμίσεις της Βασιλείας ΙΙΙ με πλήρη και συνεπή τρόπο.

Το δεύτερο σημείο που θα ήθελα να θίξω είναι ο ισχυρισμός ότι οι μεταρρυθμίσεις της Βασιλείας ΙΙΙ δεν έχουν σχεδιαστεί επαρκώς για να αντικατοπτρίζουν τα ειδικά χαρακτηριστικά της δικαιοδοσίας ή της περιοχής και ότι η εφαρμογή τους θα εμποδίσει την οικονομική ανάπτυξη και την ικανότητα των τραπεζών να αντιμετωπίσουν τις διαρθρωτικές τάσεις και προκλήσεις. όπως η ψηφιοποίηση των οικονομικών ή οι οικονομικοί κίνδυνοι που σχετίζονται με το κλίμα. Τέτοιες δηλώσεις δεν αντικατοπτρίζουν επακριβώς την αυστηρή διαδικασία που ακολούθησε η επιτροπή και δεν εξυπηρετούν τα συμφέροντα μιας βιώσιμης και χωρίς αποκλεισμούς οικονομική ανάκαμψη.

Οι μεταρρυθμίσεις της Βασιλείας ΙΙΙ επωφελήθηκαν από μια εκτεταμένη διαδικασία διαβούλευσης με ένα ευρύ φάσμα ενδιαφερομένων. Η Επιτροπή εξέδωσε τουλάχιστον 10 έγγραφα διαβούλευσης ως μέρος αυτών των μεταρρυθμίσεων, με μια συνοδευτική περίοδο διαβούλευσης που διήρκεσε σχεδόν τρία χρόνια. Τα οριστικά πρότυπα έλαβαν υπόψη πολλά από τα σχόλια που ελήφθησαν από τα ενδιαφερόμενα μέρη και αντικατοπτρίζουν τις διαφορές στις απόψεις μεταξύ των μελών μας. Περιλαμβάνουν μια σειρά εθνικών διακριτικών ευχέρειας για την παροχή ενός βαθμού ευελιξίας. Αποτελούν συμβιβασμό από τη φύση τους.

Μια εκτίμηση στο πίσω μέρος του φακέλου υποδηλώνει ότι έγιναν περισσότερες από 35 βασικές προσαρμογές στις μεταρρυθμίσεις καθώς οριστικοποιήθηκαν σε σχέση με τις αρχικές προτάσεις. Δεδομένου ότι μιλάω σε ένα κυρίως ευρωπαϊκό κοινό σήμερα, θα πρέπει να σημειώσω ότι η πλειονότητα αυτών των προσαρμογών έγιναν για να αντικατοπτρίζουν τις απόψεις διαφορετικών ευρωπαϊκών ενδιαφερομένων.

Οι μεταρρυθμίσεις της Βασιλείας ΙΙΙ καθοδηγήθηκαν επίσης από αυστηρές ποσοτικές αναλύσεις. Αυτές οι μελέτες δείχνουν ξεκάθαρα ότι η Επιτροπή πέτυχε τον στόχο που έθεσε η Ομάδα Διοικητών και Επικεφαλής Εποπτείας, και στη συνέχεια επικυρώθηκε από τους ηγέτες της G20, να μην αυξήσει σημαντικά τις συνολικές κεφαλαιακές απαιτήσεις σε παγκόσμιο επίπεδο.

Υπό πολύ συντηρητικές παραδοχές, αυτές οι μεταρρυθμίσεις εκτιμάται ότι θα αυξήσουν τις κεφαλαιακές απαιτήσεις των τραπεζών Tier 1 μόνο κατά 2% εάν εφαρμοστούν άμεσα.

Φυσικά, ορισμένες τράπεζες «απομακρυσμένες» ενδέχεται να αντιμετωπίσουν υψηλότερες απαιτήσεις, για παράδειγμα ως αποτέλεσμα επιθετικών πρακτικών μοντελοποίησης. Αυτό είναι ένα επιδιωκόμενο αποτέλεσμα των προτύπων μας, τα οποία στοχεύουν ακριβώς στη μείωση της υπερβολικής μεταβλητότητας RWA. Ακόμη και σε αυτές τις περιπτώσεις, ο πραγματικός αντίκτυπος κεφαλαίου είναι πιθανό να είναι πολύ χαμηλότερος από ό,τι υποστηρίζουν ορισμένοι ενδιαφερόμενοι, κυρίως λόγω των αρκετά μακρών μεταβατικών ρυθμίσεων: από το 2023, τα τελικά στοιχεία αυτών των μεταρρυθμίσεων θα εφαρμοστούν έως το 2028, περίπου 20 χρόνια από το GFC.

Είναι επίσης ολοένα και πιο σαφές ότι οι εκκρεμείς μεταρρυθμίσεις της Βασιλείας ΙΙΙ θα συμπληρώσουν τις προηγούμενες μεταρρυθμίσεις έχοντας θετικό καθαρό αντίκτυπο στην οικονομία. Για παράδειγμα, μια πρόσφατη ανάλυση της ΕΚΤ υποδηλώνει ότι το κόστος του ΑΕΠ για την εφαρμογή αυτών των μεταρρυθμίσεων στην Ευρώπη είναι μέτριο και προσωρινό, ενώ τα οφέλη τους θα συμβάλουν μόνιμα στην ενίσχυση της ανθεκτικότητας της οικονομίας σε δυσμενείς κρίσεις.

Διαπιστώνει επίσης ότι πιθανές αποκλίσεις από τις μεταρρυθμίσεις της Βασιλείας ΙΙΙ που έχουν συμφωνηθεί παγκοσμίως –για παράδειγμα, όσον αφορά το κατώτατο όριο παραγωγής– θα μείωναν σημαντικά τα οφέλη για την πραγματική οικονομία. Η ιστορία έχει δείξει επανειλημμένα ότι οι υγιείς και ανθεκτικές τράπεζες είναι αυτές που μπορούν να δανείσουν καλύτερα την πραγματική οικονομία και να συμβάλουν στην ανάπτυξη και τις θέσεις εργασίας. Το να υποδηλώνει κανείς ότι η εφαρμογή της Βασιλείας III θα εμποδίσει κατά κάποιο τρόπο την ικανότητα των τραπεζών να επιτύχουν αυτούς τους στόχους και να προσαρμοστούν στις διαρθρωτικές τάσεις, συμπεριλαμβανομένης της ψηφιοποίησης των οικονομικών και της κλιματικής αλλαγής, δεν υποστηρίζεται από εμπειρικά στοιχεία.

Τρίτον, και αυτό θα είναι το τελευταίο μου σημείο ως Πρόεδρος της Επιτροπής της Βασιλείας, η πλήρης και συνεπής εφαρμογή της Βασιλείας ΙΙΙ είναι ένα ισχυρό σύμβολο της συνεχούς δέσμευσης των δικαιοδοσιών στην πολυμέρεια. Τα μέλη της Επιτροπής της Βασιλείας έχουν επανειλημμένα επαναλάβει την προσδοκία τους για αυτή τη δέσμευση όλα αυτά τα χρόνια. Είναι πλέον κρίσιμο όλες οι δικαιοδοσίες των μελών της Επιτροπής της Βασιλείας να μετατρέψουν αυτή τη δέσμευση σε συγκεκριμένη δράση εφαρμόζοντας τα πρότυπα πλήρως και με συνέπεια.

Θα κάνω τώρα μερικές παρατηρήσεις σχετικά με τις συγκεκριμένες προτάσεις που συζητούνται επί του παρόντος στην Ευρώπη υπό την ιδιότητά μου ως Διοικητής της Τράπεζας της Ισπανίας. Όπως ίσως γνωρίζετε, η Επιτροπή της Βασιλείας διαθέτει ένα ολοκληρωμένο πρόγραμμα –το Πρόγραμμα Αξιολόγησης Ρυθμιστικής Συνέπειας (RCAP) – για την αξιολόγηση της συνέπειας της εφαρμογής της Βασιλείας III από τα μέλη μας μετά την έγκρισή της στο εσωτερικό. Καθώς και όταν εφαρμοστεί η Βασιλεία ΙΙΙ στην Ευρώπη, η Επιτροπή θα έχει την ευκαιρία να διενεργήσει αξιολόγηση της συνοχής του RCAP από ομοτίμους. Μέχρι τότε, θα σχολιάσω την τρέχουσα κατάσταση ως Διοικητής μιας ευρωπαϊκής εθνικής κεντρικής τράπεζας.

Το σημείο εκκίνησης μου είναι να επαναλάβω τη σημασία για την πλήρη και συνεπή εφαρμογή όλων των πτυχών του πλαισίου της Βασιλείας ΙΙΙ, όπως ορίζεται σε κοινή επιστολή 24 κεντρικών τραπεζών και εποπτικών αρχών προς την Ευρωπαϊκή Επιτροπή τον περασμένο Σεπτέμβριο.

Θα ήθελα να επωφεληθώ αυτής της ευκαιρίας για να αναλογιστώ τι σημαίνει αυτό στην πράξη τώρα που η Ευρωπαϊκή Επιτροπή δημοσίευσε την πρότασή της.

Πρώτον, είναι κρίσιμο να εφαρμοστεί το πλήρες πακέτο της Βασιλείας ΙΙΙ στην Ευρώπη, καθώς τα στοιχεία του είναι συμπληρωματικά και είναι απαραίτητα για τη διασφάλιση της ανθεκτικότητας του ευρωπαϊκού τραπεζικού συστήματος. Από αυτή την άποψη, εκτιμώ ότι η πρόταση της Επιτροπής καλύπτει όλα τα στοιχεία που περιλαμβάνονται στη Βασιλεία III.

Δεύτερον, η διατήρηση της χρηματοπιστωτικής σταθερότητας απαιτεί έγκαιρη εφαρμογή των μεταρρυθμίσεων στην Ευρώπη. Η πρόταση της Ευρωπαϊκής Επιτροπής προβλέπει ήδη καθυστέρηση δύο ετών σε σύγκριση με το χρονοδιάγραμμα που έχει συμφωνηθεί παγκοσμίως. Ως εκ τούτου, θα προέτρεπα όλα τα ενδιαφερόμενα μέρη να επιταχύνουν τις εργασίες για την εφαρμογή της Βασιλείας III στην Ευρώπη, λαμβάνοντας δεόντως υπόψη την ανάγκη σεβασμού της ευρωπαϊκής νομοθετικής μας διαδικασίας. Οποιεσδήποτε περαιτέρω καθυστερήσεις θα μπορούσαν να έχουν ως αποτέλεσμα το ευρωπαϊκό τραπεζικό σύστημα να είναι ανεπαρκώς προετοιμασμένο για να αντιμετωπίσει μελλοντικούς κλυδωνισμούς και θα μπορούσε ακόμη και να έχει ανεπιθύμητες αρνητικές επιπτώσεις στη διαδικασία εφαρμογής σε άλλες δικαιοδοσίες.

Τέλος, η συνέπεια πρέπει να είναι βασικός πυλώνας της διαδικασίας εφαρμογής στην Ευρώπη. Όπως ανέφερα προηγουμένως, η Βασιλεία ΙΙΙ ενσωματώνει αρκετή ευελιξία μέσω της χρήσης εθνικών διακριτικών ευχέρειας. Για παράδειγμα, η Ευρωπαϊκή Επιτροπή προτείνει την άσκηση της διακριτικής ευχέρειας για τον αποκλεισμό των ιστορικών ζημιών των τραπεζών κατά τον υπολογισμό των απαιτήσεων κεφαλαίου λειτουργικού κινδύνου, μια επιλογή που έχει ήδη υιοθετηθεί από άλλες δικαιοδοσίες και συμμορφώνεται με τη Βασιλεία III.

Αντίθετα, η επιδίωξη προσεγγίσεων που υπερβαίνουν την ευελιξία που έχει ενσωματωθεί στη Βασιλεία III θα πρέπει να ελαχιστοποιηθεί. Υπάρχουν ήδη ορισμένες αποκλίσεις από τα αρχικά πρότυπα της Βασιλείας ΙΙΙ στη νομοθεσία μας και η πρόταση της Ευρωπαϊκής Επιτροπής περιλαμβάνει πρόσθετες, συμπεριλαμβανομένων αρκετών στο πλαίσιο πιστωτικού κινδύνου. Τέτοιες αποκλίσεις δεν θα ήταν προς το συμφέρον της Ευρώπης, καθώς θα μπορούσαν να υπονομεύσουν την αξιοπιστία και την ευρωστία του πλαισίου των τραπεζικών κεφαλαίων μας και θα μπορούσαν να αφήσουν υποκεφαλαιοποιημένα τα ειδικά ανοίγματα σε κίνδυνο. Ένα παράδειγμα σε αυτή τη συγκυρία ενός τέτοιου σεναρίου είναι η αποτίμηση εξασφαλίσεων, καθώς εντοπίζουμε ήδη συσσώρευση συστημικού κινδύνου σε αγορές ακινήτων σε διαφορετικές δικαιοδοσίες.

Ένας άλλος τομέας που με απασχολεί σχετίζεται με το κατώτατο όριο παραγωγής, το οποίο αποτελεί βασικό στοιχείο της Βασιλείας ΙΙΙ που βοηθά στη μείωση της υπερβολικής μεταβλητότητας στα σταθμισμένα στοιχεία ενεργητικού και στην αποκατάσταση της αξιοπιστίας των δεικτών κεφαλαίου των τραπεζών. Αν και χαιρετίζω το σχέδιο “single stack” στην πρόταση της Ευρωπαϊκής Επιτροπής, σημειώνω ότι η πρόταση εισάγει επίσης μια σειρά μεταβατικών προσαρμογών όσον αφορά τα ακίνητα κατοικιών, τις μη αξιολογημένες εταιρείες και τα ανοίγματα παραγώγων. Αυτές οι προσαρμογές θα πρέπει να αποφευχθούν, καθώς, κατά την άποψή μου, παρουσιάζουν απόκλιση από τη Βασιλεία ΙΙΙ, είναι αβάσιμες από λόγους προληπτικής εποπτείας ή χρηματοπιστωτικής σταθερότητας και θα μπορούσαν να προκαλέσουν μια “κούρσα προς τα κάτω”. Θα τονίσω ότι, ακόμη και όταν εξετάζονται επιχειρήματα που απαιτούν αυτές τις προσαρμογές για τη διευκόλυνση της εφαρμογής, οποιεσδήποτε τέτοιες αποκλίσεις θα πρέπει να είναι αυστηρά προσωρινές και δεν θα πρέπει να επεκταθούν περαιτέρω.

Συμπερασματικά, η Ευρώπη έχει μια μοναδική ευκαιρία να επιδείξει τη δέσμευσή της στην πολυμέρεια και στις αποφάσεις που έχουν συμφωνηθεί παγκοσμίως. Είναι προς το συλλογικό και παγκόσμιο συμφέρον μας να προχωρήσουμε προς την εφαρμογή της Βασιλείας ΙΙΙ και να διασφαλίσουμε ότι θα εστιάσουμε την προσοχή και τους πόρους μας σε ορισμένους από τους αναδυόμενους κινδύνους και τις διαρθρωτικές τάσεις που επηρεάζουν το τραπεζικό σύστημα, συμπεριλαμβανομένης της συνεχιζόμενης ψηφιοποίησης των οικονομικών και των χρηματοοικονομικών που σχετίζονται με το κλίμα. Πάνω από μια δεκαετία μετά τον GFC, οφείλουμε στους πολίτες της Ευρώπης να δείξουμε τη δέσμευσή μας στην παγκόσμια συνεργασία και στην ενίσχυση της ανθεκτικότητας των τραπεζών μας.

Το Κουρδιστό Πορτοκάλι κλείνοντας το σημερινό αφιέρωμα στον Χάρη και τον Μάκη οι οποίοι συνειδητοποιούν πλέον ότι δεν τους ανήκει τίποτε και είναι δυστυχισμένοι, τους καλεί να αγοράσουν από την Amazon από ένα αντίτυπο του βιβλίου του William Greider, Secrets of the Temple: How the Federal Reserve Runs the Country και να εντρυφήσουν στην ανάγνωσή του.

(Προς διευκόλυνσή τούς πρoσφέρουμε στο πιάτο την περίληψη)

Για παρηγορία μπορούμε να τους πούμε πως το γεγονός ότι πλησίασαν στο μονοπάτι που οδηγεί στο Ναό είναι σπουδαία εμπειρία γνώσης. Η γνώση είναι το απόκτημά μας σε αυτό το κόσμο.

Καλή τύχη!

PART ONE: SECRETS OF THE TEMPLE

Chapter 1: The Choice of Wall Street

In the summer of 1979, President Carter found himself stuck in the mud.

His popularity was dwindling by the day, and many in the nation viewed his

administration as a model of inconsistency and confusion. The next presidential

election was not far off, and a recent Gallup poll had shown that Democrats

preferred Ted Kennedy to Carter by a more than two-to-one margin (66 to 30

percent).

Carter and his inner circle decided it was time to turn his fortunes around.

For 10 days, he secluded himself at Camp David, and invited leaders from all

spheres of American life to tell him where he went wrong, and what he should

do about it. On Sunday, July 15, Carter famously delivered what would soon be

termed his “malaise speech” (Carter in fact never used the word). Carter told the

nation that they were suffering from a sort of spiritual crisis, that America was

losing its sense of unity and moral purpose. He criticized the nation as

materialist, saying “too many of us now tend to worship self-indulgence and

consumption. Human identity is no longer defined by what one does, but by

what one owns.”

Despite derisive coverage by the press, the speech resonated with the

American people. Carter’s popularity increased by 10 percent virtually

overnight. But Carter wasn’t finished yet. Determined to make a bold statement,

on the Tuesday after his speech Carter asked for the resignations of his entire

Cabinet. Carter would review each of them, and make the changes he found

necessary. Over the following few days, the heads began to roll. The Secretary of

the Treasury, W. Michael Blumenthal, would be replaced. So would the Secretary

of Health, Education, and Welfare, the Energy Secretary, the Transportation

Secretary, and the Attorney General.

Immediately, the actions Carter took to shore up public confidence began

to backfire in that other center of American power—Wall Street. After his speech

and the announcement of wholesale changes to his administration, the markets

turned downward. Short-term interest rates spiked. What worried Wall Street

were not abstract concepts like America’s moral center or sense of purpose, what

worried Wall Street was inflation. Throughout the Carter presidency and before,

inflation raged at unusually high levels—11% around the time of Carter’s speech.

High core inflation, only compounded by surging oil prices in the wake of the

1979 Iranian Revolution, meant that every dollar an American earned today

would only buy 89 cents worth of goods in a year. As a result, Americans were

borrowing money to buy goods today that they would pay off tomorrow.

The change that worried Wall Street the most, covered little by the press,

was the resignation of the chairman of the Federal Reserve, G. William Miller.

Miller was to replace Blumenthal as Treasury Secretary, but who would replace

SomeBookBlog

2

Miller? Markets began to get jittery fearing that the vice chairman, little known

Florida banker Frederick H. Schultz, might take over. Schultz was viewed by

many as a political crony, rewarded by Carter with the vice chairmanship for

raising campaign funds. Carter soon realized he had to calm the markets by

choosing a Fed chairman that Wall Street could trust to tamp down inflation.

Vice President Walter Mondale’s chief of staff, Richard Moe, was given

the task of vetting potential candidates. Moe sought the advice of many—leaders

in business, government officials, lawyers, labor leaders, and academic

economists. One name popped up over and over: Paul Volcker. Volcker was the

President of the New York Fed and an economist who had worked in

government and the private sector. In fact, his very first job was as a junior

employee at the New York Fed. What Moe heard from everyone was that

Volcker was eminently qualified, but what he heard from some disturbed him.

Volcker was described as rigidly conservative, independent, not a team player.

Moe urged Carter to look at other options. Carter did so, but when the president

of Bank of America Tom Clausen turned down the offer, Carter made his

decision. After Volcker’s nomination was announced, the stock and bond

markets shot up, as did the value of the dollar after a months long slide. Wall

Street had their man.

Chapter 2: In the Temple

Since its conception, the Federal Reserve Bank of the United States has

been cloaked in mystery, and subject to conspiracy theories. It was alleged that

the Fed was run by a select set of individuals—Zionists, Illuminati, Satanists—

who decided the fate of the nation and, indeed, the entire world through their

control of money. Though many such outlandish accusations came from the

fringes of society, even the average person had little understanding of how the

Fed worked, or what it did.

Who owned the Fed? In fact, the Fed occupied a unique position in the

American system, positioned in-between public and private management. At the

top of the Fed’s hierarchy were its seven governors, appointed by the President

and confirmed by the Senate for 14-year terms. These governors shared power

with the presidents of the twelve Reserve Banks, spread out all across the nation

from New York to San Francisco. These twelve presidents were elected by the

board of directors in their respective districts. The boards were made up of nine

directors, six of whom were elected by member banks of the Federal Reserve

System—private commercial banks. These private banks held stock shares in the

Federal Reserve Banks.

Monetary policy was decided by the Federal Open Market Committee, or

FOMC. In FOMC meetings, the governors had seven votes and the Reserve

Banks presidents had five, which rotated among the twelve presidents, with the

notable exception of the president of the New York Fed, who always had a vote.

That private interests played a role in the decision making process and owned

stock in the Reserve banks led many to accuse the Fed of representing a private

SomeBookBlog

3

club of bankers. In fact, these stock shares were practically meaningless, and the

greater weight of power on the FOMC committee was held by appointed

officials.

These stock shares did however once give rise to an illuminating incident,

in 1939. Representative Wright Patman, a populist from Texas, announced in a

House hearing that the newly constructed Federal Reserve building was owned

not by the US government, but by the twelve Reserve banks, who were in turn

owned by private commercial banks. Thus, said Patman, the Federal Reserve

building was not owned by the federal government and not tax exempt. This

remark gave rise to several years of legal wrangling, after the D.C. tax authorities

presented a bill that the Federal Reserve refused to pay, insisting it was a

government entity. In the end, after an auction of the building had been set and

postponed several times, the twelve Reserve Banks issued quitclaim deeds,

asserting that the Federal Reserve building was indeed owned by the Federal

Government.

What did the Fed do? To the average American, this was a more

complicated question still. The Fed controlled the money supply. It set interests

rates. This was all that was understood by the average American, but these

assertions were too simplistic. For instance, what is money? The Federal Reserve

did not use the word as the average American did. The Federal Reserve in fact

had multiple definitions of money. M-1, their most basic measure of money,

included all the hard cash Americans held in their wallets and their checking

accounts. M-2 included M-1, plus what money that was stored in less liquid

forms, such as savings accounts and money market mutual funds. M-3 included

all that was in M-2 and even less liquid instruments like certificates of deposit

held by banks or corporations. Finally, the measure of total liquidity, or L,

included all financial assets that could potentially be converted to cash, such as

treasuries, commercial paper, savings bonds, and more. The money of the

American people would slosh around the economy over and over, each dollar

being earned and spent many times in a year, and often moving between the M-

1, M-2, and M-3 aggregates.

Not only did the Fed define what money was, it created money, seemingly

out of thin air. In fact, the creation money was done not only by the Fed but by

every commercial bank in the normal course of business, and was as simple as

making an entry in a ledger. A bank made a loan to an individual or a

corporation, assessing that the borrowing entity would be able to make

repayments. The bank simply credited the money to their account. Money was

created based on a banker’s assessment of the future. If the bankers were wrong,

if the future did not turn out as expected, and enough loans went bad and

depositors lost enough confidence in their bank, the depositors would bang on

the bank’s doors and demand their money back. And they would find that the

bank did not have their money. This is where the Federal Reserve stepped in, as

the lender of last resort for the American economy.

SomeBookBlog

4

If a member bank did not have enough money in reserve, it would go to

the Fed’s discount window and borrow funds, or go to another bank that had

excess reserves and borrow from them. The price of this borrowing between

banks was known as the Fed Funds rate, and it was the interest rate the Fed had

the most control over and the rate that served as the foundation for all other

interest rates in the economy. The price of membership in the Federal Reserve

system was that the reserve rate for member banks was set by the Federal

Reserve. It was through its control over reserves and the Fed Funds rate that the

Fed influenced the economy.

To expand the money supply or contract it, the Fed sold or bought bonds

at the Open Market Desk at the New York Fed. When the Fed bought bonds, it

injected cash (reserves) into the banking system. These reserve deposits could

immediately be lent out, creating a multiplication process. If the Fed bought $100

worth of bonds, $16 may be kept in reserves and $84 lent out. Then 16% of this

amount would be kept in reserves and the rest lent out, and on and on. The

original $100 purchase would create around $500 in new deposits. The Fed

influenced the supply and demand for loanable funds, and therefore set shortterm

interest rates. The Fed had less control over long term interest rates—the

bond market often had its own ideas about the distant future. The price of money

influenced the amount of credit available to finance real economic activity. The

Fed controlled reserves, which influence bank lending, which influenced the

productive capacity of the United States of America and the lives of its citizens.

The governors, Reserve Bank presidents, and employees of the Fed saw

Volcker’s appointment as a long needed return to normalcy for the institution.

The Fed had previously been led by Arthur Burns, who was abusive toward and

manipulative of his fellow governors and others. After Burns came Bill Miller,

Volcker’s predecessor. Miller was considered to be unappreciative of the Fed’s

sense of protocol and his own position, and too close to the Carter

Administration. Volcker was a company man, so to speak, a veteran of the

system with decades of experience in banking and finance.

Chapter 3: A Pact with the Devil

Paul Volcker took the oath of office on August 6, 1979. The Fed had set a

growth target of 1.5-4.5% for the M-1 measure in 1979. When Volcker took office,

M-1 was growing at an annualized rate of 10%. Volcker quickly began sending

signals in his private and public remarks that he would make an effort to tighten

up the money supply. In their August 1979 meeting, the seven governors

decided to raise the discount rate from 10 to 10.5%. This move was relatively

small (though one must remember that that 0.5% gets multiplied by hundreds of

billions of dollars in loans), but Volcker still had to contend with some governors

who thought it too drastic. In their September meeting, however, Volcker

signaled that he felt more action was needed. He proposed increasing the

discount rate once more, but backed off when he saw his fellow governors might

not be with him.

SomeBookBlog

5

At the September meeting of the FOMC, the majority voted to increase the

Fed Funds rate from 11.5 to 11.75%. (It is important to note at this point that the

full FOMC decided the Fed Funds rate, but the seven governors alone decided

the Discount rate). Again, Volcker had wanted to take a more drastic step, but

moderated his position in order to ensure a majority. Slowly, Volcker was

preparing himself and his fellow governors to take such action.

In the late summer and fall of 1979, inflation was raging into the low

double digits. Inflation was fueling a speculative boom that worried many at the

Fed and elsewhere. Individuals, farmers, corporations, and other entities rushed

to spend now before prices rose again. Of course, their buying only led to a selffulfilling

prophecy—they drove the price up, encouraging still others to do the

same thing. The boom was across nearly all markets—real estate, precious

metals, paintings, and on and on. People were rushing out of dollars and into

tangibles, considered a more reliable store of value in inflationary times.. Though

some worried that more aggressive action could stop the economy in its tracks

and cause a recession, outside critics and members of the Fed began to worry

that the Fed’s moves were too gradual to make a difference.

One symptom of this was the growing popularity and influence of an

economist from the University of Chicago, Milton Friedman. Friedman had won

the Nobel prize in 1976 for what came to be called monetarist theory, or

monetarism. Friedman argued in his seminal work, A Monetary History of the

United States, 1867-1960, that the Federal Reserve was directly responsible for

exacerbating if not causing the crash of 1929 and the Depression that followed. In

his view, the Federal Reserve should follow a simple policy of expanding the M-

1 by 3% a year, the historical growth rate of the US economy. Many within the

Fed disagreed, arguing they had to make adjustments as necessary for

developments in the global economy. Despite strong opposition, monetarism

was growing in popularity inside the Fed and out, especially within the Reserve

Banks. Though Volcker was no monetarist, he would soon find reasons to

advocate a monetarist approach to Fed policy.

Traditionally, when the Fed wanted to increase interests rates, it did so by

announcing a target interest rate (the Fed Funds rate), and then authorizing the

traders at the open market desk in New York to buy or sell treasury bonds until

the target was reached. This approach had the advantage of keeping interest

rates steady and financial markets calm. Critics alleged that the Fed was paying

too much attention to the interests of traders on Wall Street. Monetarists argued

that a much more direct approach would be to control the money supply directly

through the reserve rates. Instead of targeting a price of money and hoping that

price would produce the desired results for bank lending and inflation, the Fed

would simply control the amount of dollars flowing through the economy. The

Fed had never taken this approach before. Though this method would contain

the growth of the money supply, many at the Fed believed that it would create

interest rate volatility as bankers adjusted to the change, and the Fed abhorred

instability.

SomeBookBlog

6

Still, though, Volcker saw several reasons to try exactly such an approach.

Volcker was convinced that drastic action—an increase of 2-3, possibly 4-5% in

the Fed Funds rate—was needed to curb inflation. But he doubted he could

cobble together a sustainable majority to vote for such action. Setting the reserve

rate higher would likely produce the desired shift in interest rates, while

distancing the FOMC from the move. Interest rate increases could be blamed on

“market pressures” (which of course was true but neglected the fact that those

market pressures had been set in motion by the Fed). With this approach,

Volcker believed he could get both the hawks and doves to go along.

Volcker also thought such a move would inject a note of uncertainty into

the system. By upsetting the Fed’s traditional mode of business, Volcker would

upset the psychological momentum of inflation; it was a warning to bankers that

interest rates may not increase steadily, that they could move quickly against

them. The bankers, thus warned, would become more cautious in their lending.

It was important that the Fed send a strong signal that it intended to curb

inflation.

Volcker proposed a reserve increase of 8% on the funds banks borrowed

to finance loan expansion. This point demands some explaining. Traditionally,

banks were constrained in their lending by the growth of their interest free